Вам также может понравиться

- The Biometric Industry Report - Forecasts and Analysis to 2006От EverandThe Biometric Industry Report - Forecasts and Analysis to 2006M LockieОценок пока нет

- Development of FDA-Regulated Medical Products: A Translational ApproachОт EverandDevelopment of FDA-Regulated Medical Products: A Translational ApproachОценок пока нет

- Top Ten List (IVDT Archive, Jul 05)Документ6 страницTop Ten List (IVDT Archive, Jul 05)Calvin KleinОценок пока нет

- Top Electronic Medical Device Manufacturers in The WorldДокумент13 страницTop Electronic Medical Device Manufacturers in The WorldjackОценок пока нет

- I-Scan Project: Alberta'S: Medical Device SectorДокумент18 страницI-Scan Project: Alberta'S: Medical Device SectortimothytroyОценок пока нет

- Healthcare Analytical Testing ServicesДокумент34 страницыHealthcare Analytical Testing ServicesAaryan AgrahariОценок пока нет

- Excellence in Diagnostic CareДокумент20 страницExcellence in Diagnostic CareDominic LiangОценок пока нет

- Value Chain in Health Care IndustryДокумент20 страницValue Chain in Health Care IndustrydddddeeeeeОценок пока нет

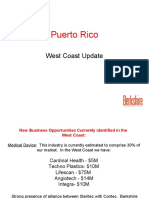

- West Coast UpdateДокумент14 страницWest Coast Updatedreder22Оценок пока нет

- Emerging Medical FINAL PDFДокумент41 страницаEmerging Medical FINAL PDFsriprasanthiОценок пока нет

- Nside: Former Deputy Commissioner Alleges Bias at Gene Test Panel Large Firm Mantra Growth Comes by Any M&A PossibleДокумент12 страницNside: Former Deputy Commissioner Alleges Bias at Gene Test Panel Large Firm Mantra Growth Comes by Any M&A PossibleeparsonsОценок пока нет

- Medical Science PlanДокумент22 страницыMedical Science PlanAdeline OngОценок пока нет

- Research Paper FinalДокумент13 страницResearch Paper FinalUrooj AnsariОценок пока нет

- The Rise of Global Medical TechnologyДокумент28 страницThe Rise of Global Medical Technologyranga.ramanОценок пока нет

- Pharmaceutical Supply ChainsДокумент13 страницPharmaceutical Supply Chainsixion11Оценок пока нет

- 2015 Innovation AgendaДокумент1 страница2015 Innovation AgendaAdvaMedLCIОценок пока нет

- Biobanking - Equipments, 2009-2015 - BroucherДокумент4 страницыBiobanking - Equipments, 2009-2015 - BroucherAxis ResearchMindОценок пока нет

- 4 Supply Chain PharmaДокумент13 страниц4 Supply Chain PharmaMirena Boycheva100% (1)

- Individual Assignment Example - Mindray Medical PDFДокумент10 страницIndividual Assignment Example - Mindray Medical PDFCheryl ShongОценок пока нет

- Global Cro ReportДокумент9 страницGlobal Cro ReportJoseph KamaleshОценок пока нет

- Medical Device IndustryДокумент53 страницыMedical Device Industrydr_gauravsaxena100% (1)

- Electromedical Ray XДокумент13 страницElectromedical Ray XLuis MuñozОценок пока нет

- Case 1 - GE Globalizes Its Medical System BusinessДокумент2 страницыCase 1 - GE Globalizes Its Medical System Businessdinar50% (2)

- Medical Equipment & Supply MFG ProfileДокумент18 страницMedical Equipment & Supply MFG ProfileChad Thayer VОценок пока нет

- Pulse Redefining Medical Technology InnovationДокумент64 страницыPulse Redefining Medical Technology InnovationAdvaMedLCIОценок пока нет

- 2013 Medical Equipment Supplies FinalДокумент28 страниц2013 Medical Equipment Supplies Finaldevalj100% (1)

- Leering University Healthcare StrategyДокумент18 страницLeering University Healthcare Strategychuff6675Оценок пока нет

- The Global Pharmaceutical Industry Case Study Scenario PlanningДокумент4 страницыThe Global Pharmaceutical Industry Case Study Scenario PlanningIke Ten100% (1)

- GE Heathcare BOP ArticleДокумент7 страницGE Heathcare BOP ArticleMustafa HussainОценок пока нет

- Innovation Agenda: February 2015Документ4 страницыInnovation Agenda: February 2015AdvaMedLCIОценок пока нет

- Ozalp Et Al 2022 Digital Colonization of Highly Regulated Industries An Analysis of Big Tech Platforms Entry IntoДокумент30 страницOzalp Et Al 2022 Digital Colonization of Highly Regulated Industries An Analysis of Big Tech Platforms Entry IntotijncohendelaraОценок пока нет

- GoodFellas-Healthcare & Life Sciences in US-Final ReportДокумент10 страницGoodFellas-Healthcare & Life Sciences in US-Final ReportAnkit SuriОценок пока нет

- TWB Position Paper Pharmaceutical IndustryДокумент9 страницTWB Position Paper Pharmaceutical IndustryThe Writers BlockОценок пока нет

- Between A Political Rock and Industry Hard Place:: THE FDA's 510 (K) InitiativeДокумент11 страницBetween A Political Rock and Industry Hard Place:: THE FDA's 510 (K) InitiativemaikagmОценок пока нет

- Biomedical Engineering and Medical Device DesignДокумент1 страницаBiomedical Engineering and Medical Device Designmesic9029Оценок пока нет

- Handhelds in Healthcare The World Market For PDAs, Smartphones, Tablet PCS, Handheld Monitors & ScannersДокумент9 страницHandhelds in Healthcare The World Market For PDAs, Smartphones, Tablet PCS, Handheld Monitors & ScannersVero FrancoОценок пока нет

- Medical Devices Sector: Key Challenges and MethodologiesДокумент2 страницыMedical Devices Sector: Key Challenges and MethodologiesGyan PrakashОценок пока нет

- Pca Ijiset V7 I7 13Документ6 страницPca Ijiset V7 I7 13PeaceОценок пока нет

- 6544f60884188 Health Blues Case Study Sandee C For IIM Ranchi 2023Документ4 страницы6544f60884188 Health Blues Case Study Sandee C For IIM Ranchi 2023Divyansh SaxenaОценок пока нет

- Medical Devices and Equipment Sector ProfileДокумент3 страницыMedical Devices and Equipment Sector ProfileArvind MehtaОценок пока нет

- Pharmaceutical & Healthcare SectorДокумент14 страницPharmaceutical & Healthcare SectorSayujya ChaurasiaОценок пока нет

- Biotech TT DevcountriesДокумент11 страницBiotech TT Devcountriesydss19Оценок пока нет

- Assignent 2 - SDMMДокумент16 страницAssignent 2 - SDMMwipbanuaОценок пока нет

- IQ4I Research & Consultancy Published A New Report On "Cell Expansion Global Market - Forecast To 2022"Документ4 страницыIQ4I Research & Consultancy Published A New Report On "Cell Expansion Global Market - Forecast To 2022"VinayОценок пока нет

- Cepton Strategic Outsourcing Across The Pharmaceuticals Value ChainДокумент9 страницCepton Strategic Outsourcing Across The Pharmaceuticals Value ChainFrenzy FrenesisОценок пока нет

- China Medical Device MarketДокумент20 страницChina Medical Device Marketkrrishshrish14Оценок пока нет

- Global Trends Bio Pharma IndustryДокумент26 страницGlobal Trends Bio Pharma Industryhamza123456789Оценок пока нет

- Lab Manager May 2010Документ89 страницLab Manager May 2010DavidОценок пока нет

- IH InstrumentationДокумент5 страницIH InstrumentationBharatiyaNaariОценок пока нет

- Massachusetts' Medical Device EcosystemДокумент22 страницыMassachusetts' Medical Device EcosystemSteven TelloОценок пока нет

- Small Business Developed Innovative Tests: A Proposed Regulatory Exemption ForДокумент4 страницыSmall Business Developed Innovative Tests: A Proposed Regulatory Exemption ForfdablogОценок пока нет

- Bio WorldДокумент198 страницBio Worldmc_goaОценок пока нет

- Clinical Engineering in Canada: by AaaДокумент16 страницClinical Engineering in Canada: by AaaAne moОценок пока нет

- Regulatory BrainboxДокумент14 страницRegulatory BrainboxRenuОценок пока нет

- Tijuana Medical MFGДокумент5 страницTijuana Medical MFGHarold A Sequeira RojasОценок пока нет

- 3D Technology in Healthcare Mar Ket Forecast 2014 - 2020: Occams Business Research & ConsultingДокумент20 страниц3D Technology in Healthcare Mar Ket Forecast 2014 - 2020: Occams Business Research & ConsultingTrai HNОценок пока нет

- IQ4I Research & Consultancy Published A New Report On "Catheters Global Market - Forecast To 2022"Документ4 страницыIQ4I Research & Consultancy Published A New Report On "Catheters Global Market - Forecast To 2022"VinayОценок пока нет

- Industry's Involvement in R&D For Neglected Diseases in Developing CountriesДокумент11 страницIndustry's Involvement in R&D For Neglected Diseases in Developing CountriesphilomenebouchonОценок пока нет

- Digital Health: Scaling Healthcare to the WorldОт EverandDigital Health: Scaling Healthcare to the WorldHomero RivasОценок пока нет

- Game Theory 93 2 Slide01Документ44 страницыGame Theory 93 2 Slide01amiref100% (1)

- 9 RepeatedДокумент17 страниц9 RepeatedamirefОценок пока нет

- 1 s2.0 S0377221710003735 MainДокумент8 страниц1 s2.0 S0377221710003735 MainamirefОценок пока нет

- 3.4.bertrand ModelДокумент9 страниц3.4.bertrand ModelamirefОценок пока нет

- 3.4.bertrand ModelДокумент9 страниц3.4.bertrand ModelamirefОценок пока нет

- 4 - Dafny - Do Report Cards Tell Consumers Anything They Don't Already Know - The Case of Medicare Hmos - 2008Документ32 страницы4 - Dafny - Do Report Cards Tell Consumers Anything They Don't Already Know - The Case of Medicare Hmos - 2008amirefОценок пока нет

- Business Process Mining: An Industrial ApplicationДокумент30 страницBusiness Process Mining: An Industrial ApplicationpanketОценок пока нет

- 67Документ14 страниц67amirefОценок пока нет

- Atlantic Computer Case SolutionsДокумент4 страницыAtlantic Computer Case Solutionsamiref100% (1)

- Author IndexДокумент5 страницAuthor IndexamirefОценок пока нет

- Analytic Business Processes: The Third Generation: A Monash Information Services White Paper by Curt A. Monash, PH.DДокумент26 страницAnalytic Business Processes: The Third Generation: A Monash Information Services White Paper by Curt A. Monash, PH.DamirefОценок пока нет

- 2003 Peteraf Unraveling Resource Based TangleДокумент15 страниц2003 Peteraf Unraveling Resource Based TangleamirefОценок пока нет

- Chopra Sunil 090814Документ6 страницChopra Sunil 090814amirefОценок пока нет

- 44 Dec013 0010Документ3 страницы44 Dec013 0010amirefОценок пока нет

- Market Dynamics in The Healthcare IndustryДокумент14 страницMarket Dynamics in The Healthcare IndustryamirefОценок пока нет

- I e Accenture Sap Mission Critical FinalДокумент8 страницI e Accenture Sap Mission Critical FinalamirefОценок пока нет

- Healthcare Delivery - Customers by Market Segment SummaryДокумент6 страницHealthcare Delivery - Customers by Market Segment SummaryamirefОценок пока нет

- Analytic Business Processes: The Third Generation: A Monash Information Services White Paper by Curt A. Monash, PH.DДокумент26 страницAnalytic Business Processes: The Third Generation: A Monash Information Services White Paper by Curt A. Monash, PH.DamirefОценок пока нет

- 6-5 Von NordenflychtДокумент37 страниц6-5 Von NordenflychtamirefОценок пока нет

- Dipanjan Kumar Dey - Docx NewДокумент6 страницDipanjan Kumar Dey - Docx NewMerhan FoudaОценок пока нет

- Causal 6Документ2 страницыCausal 6Ishtiaq IshaqОценок пока нет

- 3 D Charles Fishman - The Insourcing Boom - The AtlanticДокумент11 страниц3 D Charles Fishman - The Insourcing Boom - The AtlanticamirefОценок пока нет

- 1 s2gfcg.0 S0950584914002274 MainДокумент1 страница1 s2gfcg.0 S0950584914002274 MainamirefОценок пока нет

- 125 Klein, Complex ContractsДокумент16 страниц125 Klein, Complex ContractsamirefОценок пока нет

- Medical Device Growth in Emerging Markets InVivo 1206Документ9 страницMedical Device Growth in Emerging Markets InVivo 1206amirefОценок пока нет

- 10.1007 - s10257 013 0221 4 PDFДокумент4 страницы10.1007 - s10257 013 0221 4 PDFamirefОценок пока нет

- Designing Service Systems by Bridging The Front Stage'' and Back Stage''Документ21 страницаDesigning Service Systems by Bridging The Front Stage'' and Back Stage''amirefОценок пока нет

- 1 s2.0 S0020025514008135 Main PDFДокумент22 страницы1 s2.0 S0020025514008135 Main PDFamirefОценок пока нет

- Isulat Lamang Ang Titik NG Tamang Sagot Sa Inyong Papel. (Ilagay Ang Pangalan, Section atДокумент1 страницаIsulat Lamang Ang Titik NG Tamang Sagot Sa Inyong Papel. (Ilagay Ang Pangalan, Section atMysterious StudentОценок пока нет

- GB GW01 14 04 02Документ2 страницыGB GW01 14 04 02Muhammad LukmanОценок пока нет

- VavДокумент8 страницVavkprasad_56900Оценок пока нет

- Badminton ReviewerДокумент10 страницBadminton ReviewerHailsey WinterОценок пока нет

- Clocks (New) PDFДокумент5 страницClocks (New) PDFAbhay DabhadeОценок пока нет

- c270 KW NTA855G2 60 HZДокумент31 страницаc270 KW NTA855G2 60 HZAhmad El KhatibОценок пока нет

- 1n5711 RF Detector Diode 70v PIV DatasheetДокумент3 страницы1n5711 RF Detector Diode 70v PIV DatasheetgordslaterОценок пока нет

- Joby Aviation - Analyst Day PresentationДокумент100 страницJoby Aviation - Analyst Day PresentationIan TanОценок пока нет

- Management of DredgedExcavated SedimentДокумент17 страницManagement of DredgedExcavated SedimentMan Ho LamОценок пока нет

- Course Code:TEX3021 Course Title: Wet Processing Technology-IIДокумент20 страницCourse Code:TEX3021 Course Title: Wet Processing Technology-IINakib Ibna BasharОценок пока нет

- Presentation AcetanilideДокумент22 страницыPresentation AcetanilideNovitasarii JufriОценок пока нет

- Crma Unit 1 Crma RolesДокумент34 страницыCrma Unit 1 Crma Rolesumop3plsdn0% (1)

- Solar Charge Controller: Solar Car Solar Home Solar Backpack Solar Boat Solar Street Light Solar Power GeneratorДокумент4 страницыSolar Charge Controller: Solar Car Solar Home Solar Backpack Solar Boat Solar Street Light Solar Power Generatorluis fernandoОценок пока нет

- Danika Cristoal 18aДокумент4 страницыDanika Cristoal 18aapi-462148990Оценок пока нет

- Birla MEEP Op ManualДокумент43 страницыBirla MEEP Op ManualAshok ChettiyarОценок пока нет

- Paper-Czechowski-Slow-strain-rate Stress Corrosion Testing of Welded Joints of Al-Mg AlloysДокумент4 страницыPaper-Czechowski-Slow-strain-rate Stress Corrosion Testing of Welded Joints of Al-Mg Alloysjavo0128Оценок пока нет

- Hevi-Bar II and Safe-Lec 2Документ68 страницHevi-Bar II and Safe-Lec 2elkabongscribdОценок пока нет

- 2nd APJ Abdul Kalam Essay Writing CompetitionДокумент2 страницы2nd APJ Abdul Kalam Essay Writing CompetitionANURAG SINGHОценок пока нет

- Cold Regions Science and TechnologyДокумент8 страницCold Regions Science and TechnologyAbraham SilesОценок пока нет

- Haldex-Barnes 2-Stage Pump For Log SplittersДокумент2 страницыHaldex-Barnes 2-Stage Pump For Log SplittersPer Akkamaan AgessonОценок пока нет

- 988611457NK448908 Vehicle Scan ReportДокумент5 страниц988611457NK448908 Vehicle Scan ReportVictor Daniel Piñeros ZubietaОценок пока нет

- MSDS DowthermДокумент4 страницыMSDS DowthermfebriantabbyОценок пока нет

- 2017 Classification of Periodontal and Peri-Implant Diseases and Conditions. Decision Making Algorithms For Clinical PracticeДокумент40 страниц2017 Classification of Periodontal and Peri-Implant Diseases and Conditions. Decision Making Algorithms For Clinical PracticebbОценок пока нет

- B737-3 ATA 23 CommunicationsДокумент112 страницB737-3 ATA 23 CommunicationsPaul RizlОценок пока нет

- Document List - Eni Progetti - Algeria BRN-MLE - 2019-06-10Документ18 страницDocument List - Eni Progetti - Algeria BRN-MLE - 2019-06-10Naceri Mohamed RedhaОценок пока нет

- T.A.T.U. - Waste Management - Digital BookletДокумент14 страницT.A.T.U. - Waste Management - Digital BookletMarieBLОценок пока нет

- RD Sharma Class8 SolutionsДокумент2 страницыRD Sharma Class8 Solutionsncertsoluitons100% (2)

- Pusheen With Donut: Light Grey, Dark Grey, Brown, RoséДокумент13 страницPusheen With Donut: Light Grey, Dark Grey, Brown, RosémafaldasОценок пока нет

- Bulk Material/Part Ppap Process Checklist / Approval: Required?Документ32 страницыBulk Material/Part Ppap Process Checklist / Approval: Required?krds chidОценок пока нет

- Statics: Vector Mechanics For EngineersДокумент39 страницStatics: Vector Mechanics For EngineersVijay KumarОценок пока нет