Вам также может понравиться

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Process costing methods and calculationsДокумент10 страницProcess costing methods and calculationsTricia Mae Fernandez67% (3)

- Low Cost KB Drip - TERI PDFДокумент102 страницыLow Cost KB Drip - TERI PDFAnkit JainОценок пока нет

- MAS 25 27TH BATCH With AnswersДокумент15 страницMAS 25 27TH BATCH With AnswersSarah Jane GanigaОценок пока нет

- Supply Chain Finance Management Mba ProjectДокумент14 страницSupply Chain Finance Management Mba ProjectPooja BansalОценок пока нет

- Customer Perception Towards Mutual FundsДокумент82 страницыCustomer Perception Towards Mutual FundsMohd Fahad100% (10)

- Analysis of Investment Options MBA ProjectДокумент64 страницыAnalysis of Investment Options MBA ProjectAshish Sood100% (2)

- Income Tax ChartДокумент2 страницыIncome Tax ChartAnkit JainОценок пока нет

- Swami VivekanandaДокумент24 страницыSwami VivekanandaAnkit JainОценок пока нет

- Banking in IndiaДокумент12 страницBanking in IndiaAnkit JainОценок пока нет

- Electronic Communications Equipment: Telecommunication Acquisition Storage InformationДокумент1 страницаElectronic Communications Equipment: Telecommunication Acquisition Storage InformationAnkit JainОценок пока нет

- ManagmentДокумент12 страницManagmentAnkit JainОценок пока нет

- Ectronics Deals WithДокумент6 страницEctronics Deals WithAnkit JainОценок пока нет

- Definitions of Financial ManagementДокумент2 страницыDefinitions of Financial Managementletter_ashish4444Оценок пока нет

- AtomyДокумент21 страницаAtomyAnkit JainОценок пока нет

- IfmДокумент7 страницIfmAnkit JainОценок пока нет

- FinanceДокумент9 страницFinanceAnkit JainОценок пока нет

- Amazing Facts About Big 4 Accounting FirmsДокумент20 страницAmazing Facts About Big 4 Accounting FirmsMoralVolcanoОценок пока нет

- List of BanksДокумент4 страницыList of BanksAnkit JainОценок пока нет

- Capital BudgetingДокумент78 страницCapital BudgetingAnkit Jain100% (1)

- Airtel 120314015809 Phpapp02Документ97 страницAirtel 120314015809 Phpapp02Ankit JainОценок пока нет

- Acclimited 120821052457 Phpapp01Документ67 страницAcclimited 120821052457 Phpapp01Ankit JainОценок пока нет

- Banking in IndiaДокумент7 страницBanking in IndiaAnkit JainОценок пока нет

- Reliance Power & GMR IPO AnalysisДокумент94 страницыReliance Power & GMR IPO AnalysisNagarjun ArjunОценок пока нет

- Banking in IndiaДокумент7 страницBanking in IndiaAnkit JainОценок пока нет

- Acclimited 120821052457 Phpapp01Документ67 страницAcclimited 120821052457 Phpapp01Ankit JainОценок пока нет

- Sales Promotion Schemes Project Report MBAДокумент118 страницSales Promotion Schemes Project Report MBAAnkit JainОценок пока нет

- Sales Promotion Schemes Project Report MBAДокумент118 страницSales Promotion Schemes Project Report MBAAnkit JainОценок пока нет

- Pai International: B.D Road, ChitradurgaДокумент1 страницаPai International: B.D Road, ChitradurgaAnkit JainОценок пока нет

- Sales Promotion Schemes Project Report MBAДокумент118 страницSales Promotion Schemes Project Report MBAAnkit JainОценок пока нет

- Study of Quality of Work LifeДокумент89 страницStudy of Quality of Work LifeAnkit JainОценок пока нет

- Indian Capital MarketДокумент69 страницIndian Capital MarketAnkit JainОценок пока нет

- Chapter 3 Solutions Comm 305Документ77 страницChapter 3 Solutions Comm 305mike100% (1)

- Paper 2newДокумент328 страницPaper 2newAnonymous 1ClGHbiT0JОценок пока нет

- Topic 11 A181 - Variance AnalysisДокумент38 страницTopic 11 A181 - Variance AnalysisEngku FarahОценок пока нет

- Midterm Examination: Cost AccountingДокумент12 страницMidterm Examination: Cost AccountingHardly Dare GonzalesОценок пока нет

- Acctg 402Документ9 страницAcctg 402Marriah Izzabelle Suarez RamadaОценок пока нет

- Chapter 041Документ248 страницChapter 041abeОценок пока нет

- Abs and VarДокумент7 страницAbs and VarChloe Chiong50% (2)

- Cost CurvesДокумент64 страницыCost CurvesChiranjitОценок пока нет

- Strategic Cost Management PDFДокумент20 страницStrategic Cost Management PDFKrizza Sajonia TaboclaonОценок пока нет

- Engineering Economics Breakeven AnalysisДокумент39 страницEngineering Economics Breakeven AnalysisNagesh NОценок пока нет

- Roura ProjMgtExer1Документ1 страницаRoura ProjMgtExer1Irish Nicole RouraОценок пока нет

- SCM TableДокумент5 страницSCM TableRed VelvetОценок пока нет

- Introduction to Cost Management PrinciplesДокумент49 страницIntroduction to Cost Management PrinciplesHARYATI SETYORINI100% (1)

- Demand Driven Answers For AccountantsДокумент13 страницDemand Driven Answers For AccountantsRichard ChiangОценок пока нет

- ACCOUNTING FOR MANAGERS Theoretical QuestionsДокумент5 страницACCOUNTING FOR MANAGERS Theoretical QuestionsAnjana AnilkumarОценок пока нет

- Strategic Costing: Variable vs AbsorptionДокумент9 страницStrategic Costing: Variable vs AbsorptionMargie Garcia LausaОценок пока нет

- ACC123 InventoryCostFlow Problem11-6 LagurinДокумент2 страницыACC123 InventoryCostFlow Problem11-6 Lagurinkhryzellia lagurinОценок пока нет

- Sample Problems On Relevant CostsДокумент9 страницSample Problems On Relevant CostsJames Ryan AlzonaОценок пока нет

- Management Accounting Practices and Performance of Micro, Small and Medium Enterprises in Makassar CityДокумент7 страницManagement Accounting Practices and Performance of Micro, Small and Medium Enterprises in Makassar Cityhiếu trầnОценок пока нет

- Job Order Costing ConceptsДокумент3 страницыJob Order Costing ConceptsMarites ArcenaОценок пока нет

- Solution Manual For Managerial Accounting Decision Making and Motivating Performance 1st Edition Datar Rajan 0132816245Документ36 страницSolution Manual For Managerial Accounting Decision Making and Motivating Performance 1st Edition Datar Rajan 0132816245richardwilsonmgftzpsjxq100% (21)

- Contoh Kasus Job Order CostingДокумент14 страницContoh Kasus Job Order CostingMuhammadIrfanОценок пока нет

- Environmental Management Accounting and Firm Performance: Sayedeh Parastoo Saeidi, Saudah Sofian, Parvaneh SaeidiДокумент10 страницEnvironmental Management Accounting and Firm Performance: Sayedeh Parastoo Saeidi, Saudah Sofian, Parvaneh SaeidiJavier Noel ClaudioОценок пока нет

- Chapter 3 CVPДокумент26 страницChapter 3 CVPshuhadaОценок пока нет

- Cycle InventoryДокумент13 страницCycle InventoryUmang ZehenОценок пока нет

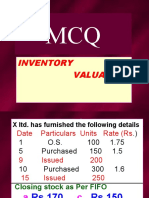

- MCQ Inventory Valuation LBSIMДокумент49 страницMCQ Inventory Valuation LBSIMSumit SharmaОценок пока нет

- Cost & Work Accounting Multiple Choice QuestionsДокумент55 страницCost & Work Accounting Multiple Choice QuestionsYash PardeshiОценок пока нет

- Management Accounting - Course Handout - 3Документ4 страницыManagement Accounting - Course Handout - 3DiptОценок пока нет