Вам также может понравиться

- K.G.Joshi College of Arts & N.G.Bedekar College of Commerce Certificate of Project WorkДокумент2 страницыK.G.Joshi College of Arts & N.G.Bedekar College of Commerce Certificate of Project Workdarthvader005Оценок пока нет

- SSC CGL 2013 Preliminary Exam Question PaperДокумент16 страницSSC CGL 2013 Preliminary Exam Question PaperSai Bhargav VeerabathiniОценок пока нет

- IM 4th SemДокумент20 страницIM 4th Semdarthvader005Оценок пока нет

- RM 4th SemДокумент26 страницRM 4th Semdarthvader005Оценок пока нет

- Edited MicrofinanceДокумент59 страницEdited Microfinancedarthvader005Оценок пока нет

- Euro Currency MarketДокумент42 страницыEuro Currency Marketdarthvader005Оценок пока нет

- Student - Declaration: Bilin.E.B, East West College of ManagementДокумент4 страницыStudent - Declaration: Bilin.E.B, East West College of Managementdarthvader005Оценок пока нет

- SMДокумент26 страницSMdarthvader005Оценок пока нет

- Brief OverviewДокумент5 страницBrief Overviewdarthvader005Оценок пока нет

- K. G. Joshi Collage of Arts & N.G. Bedekar College of CommerceДокумент18 страницK. G. Joshi Collage of Arts & N.G. Bedekar College of Commercedarthvader005Оценок пока нет

- HRM IndexДокумент1 страницаHRM Indexdarthvader005Оценок пока нет

- Project On AseanДокумент39 страницProject On Aseandarthvader005100% (1)

- Infosys LearningMate Recruitment Selection ProcessДокумент53 страницыInfosys LearningMate Recruitment Selection Processdarthvader005Оценок пока нет

- Management Practices and Organiztional Behavior: 1 Suman Tiwari (A-22)Документ22 страницыManagement Practices and Organiztional Behavior: 1 Suman Tiwari (A-22)darthvader005Оценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Mock Test - 1-1473080346944 PDFДокумент7 страницMock Test - 1-1473080346944 PDFSonali DulwaniОценок пока нет

- ZACKS Screening PDFДокумент53 страницыZACKS Screening PDFraviraviravi1100% (1)

- c3 Capital Allocation of Risky AssetsДокумент39 страницc3 Capital Allocation of Risky AssetsfelipeОценок пока нет

- 2021 FEDVIP Dental RatesДокумент3 страницы2021 FEDVIP Dental RatesFedSmith Inc.100% (3)

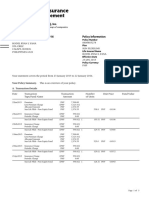

- Anniversary Statement 25 January 2016Документ3 страницыAnniversary Statement 25 January 2016Rodel Ryan YanaОценок пока нет

- A Study of An Derivative Market in IndiaДокумент22 страницыA Study of An Derivative Market in IndiaSuvankar MallickОценок пока нет

- C6T2 - Basel III - Risk Management PDFДокумент10 страницC6T2 - Basel III - Risk Management PDFTanmoy IimcОценок пока нет

- Financial Risk ManagementДокумент4 страницыFinancial Risk ManagementJeraldine Nicole RazonОценок пока нет

- The Relevance of Factors Affecting Real Estate Investment DecisionsДокумент16 страницThe Relevance of Factors Affecting Real Estate Investment DecisionsMariaОценок пока нет

- Insurance BusinessДокумент69 страницInsurance BusinessMittal Kirti MukeshОценок пока нет

- 999dice - BotДокумент30 страниц999dice - BotSMGОценок пока нет

- PPL Brokers Setup and Usage: April 2020Документ24 страницыPPL Brokers Setup and Usage: April 2020saxobobОценок пока нет

- M一级百题段风险管理Alex金程教育Документ56 страницM一级百题段风险管理Alex金程教育JIAWEIОценок пока нет

- List of Insurance Companies With Valid and Existing CA As of 30 June 2022Документ3 страницыList of Insurance Companies With Valid and Existing CA As of 30 June 2022LGU PASAY SAFETY SEAL CERTIFICATIONОценок пока нет

- Overview of Property and Casualty ReinsuranceДокумент29 страницOverview of Property and Casualty ReinsuranceAman AroraОценок пока нет

- CGC - 2.2.1 Study - 8FDLaelerДокумент7 страницCGC - 2.2.1 Study - 8FDLaelerCaleb Gonzalez CruzОценок пока нет

- KIM - Kotak Multi Asset Allocator Fund of Fund - DynamicДокумент17 страницKIM - Kotak Multi Asset Allocator Fund of Fund - DynamicTedtОценок пока нет

- Read This First - High ProbabilityДокумент5 страницRead This First - High ProbabilitySanthosh InigoeОценок пока нет

- User Manual PipGenius v1.25Документ10 страницUser Manual PipGenius v1.25maОценок пока нет

- Final RevisionДокумент25 страницFinal RevisionTrang CaoОценок пока нет

- Accounting For Proportional TreatiesДокумент35 страницAccounting For Proportional TreatiesGashawОценок пока нет

- CH12Документ39 страницCH12Z pristinОценок пока нет

- Zimbabwe 2011 Fourth Quarter - Short Term Insurance ReportДокумент33 страницыZimbabwe 2011 Fourth Quarter - Short Term Insurance ReportKristi DuranОценок пока нет

- FINANCIAL DERIVATIVES Unit - 1Документ18 страницFINANCIAL DERIVATIVES Unit - 1Neehasultana ShaikОценок пока нет

- BAUTISTA BAFIMARX ACT181, Activity 2Документ3 страницыBAUTISTA BAFIMARX ACT181, Activity 2Joshua BautistaОценок пока нет

- Credit Risk Modelling Literature ReviewДокумент5 страницCredit Risk Modelling Literature Reviewea3h1c1p100% (1)

- ABBREVIATIONSДокумент74 страницыABBREVIATIONSElizabeth SharmaОценок пока нет

- 1-Law On Insurance EngДокумент13 страниц1-Law On Insurance EngSao SaraОценок пока нет

- Introduction of InsuranceДокумент11 страницIntroduction of InsuranceNisarg ShahОценок пока нет

- Chapter 4 - Teori AkuntansiДокумент30 страницChapter 4 - Teori AkuntansiCut Riezka SakinahОценок пока нет