Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Reviewer Personal Property Security ActДокумент34 страницыReviewer Personal Property Security ActSbl Irv100% (15)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Due Diligence Checklist: For Use On Commercial Real EstateДокумент2 страницыDue Diligence Checklist: For Use On Commercial Real EstateTejas Patil100% (1)

- Schedule of Stay Itinerary Template Free WordДокумент2 страницыSchedule of Stay Itinerary Template Free WordheyoooОценок пока нет

- 2023 Greeneville Farmers Market RulesДокумент6 страниц2023 Greeneville Farmers Market RulesGFM BoardОценок пока нет

- Office Fit Out ManualДокумент17 страницOffice Fit Out ManualClarence Lim0% (1)

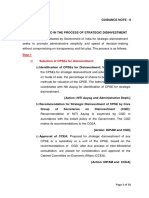

- Guidance Notes Dipam Valuation II To V - 1Документ35 страницGuidance Notes Dipam Valuation II To V - 1tomsraoОценок пока нет

- Election Law Case Digest (Final)Документ57 страницElection Law Case Digest (Final)Evitha Bernabe-Rodriguez100% (3)

- Marine Insurance CasesДокумент13 страницMarine Insurance CasesEvitha Bernabe-RodriguezОценок пока нет

- Office of The Solicitor General For Appellant. Rustics F. de Los Reyes, Jr. For AppelleesДокумент9 страницOffice of The Solicitor General For Appellant. Rustics F. de Los Reyes, Jr. For AppelleesEvitha Bernabe-RodriguezОценок пока нет

- People V Maceren: Ratio The Rule-Making Power Must Be Confined To Details For Regulating The Mode orДокумент2 страницыPeople V Maceren: Ratio The Rule-Making Power Must Be Confined To Details For Regulating The Mode orEvitha Bernabe-RodriguezОценок пока нет

- Sec 14. Puyat V de GuzmanДокумент7 страницSec 14. Puyat V de GuzmanEvitha Bernabe-RodriguezОценок пока нет

- San Beda College of Law Mendiola, ManilaДокумент19 страницSan Beda College of Law Mendiola, ManilaEvitha Bernabe-RodriguezОценок пока нет

- Solid Homes V CAДокумент2 страницыSolid Homes V CAEvitha Bernabe-RodriguezОценок пока нет

- Fisher & QuijanoДокумент69 страницFisher & QuijanoEvitha Bernabe-RodriguezОценок пока нет

- SSS BenefitsДокумент7 страницSSS BenefitsEvitha Bernabe-RodriguezОценок пока нет

- ARCHITECTДокумент3 страницыARCHITECTEvitha Bernabe-RodriguezОценок пока нет

- Transpo Case Digests 2Документ12 страницTranspo Case Digests 2Evitha Bernabe-RodriguezОценок пока нет

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledДокумент7 страницBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledEvitha Bernabe-RodriguezОценок пока нет

- TAX.2811 Deductions From Gross IncomeДокумент10 страницTAX.2811 Deductions From Gross IncomeMary Ann Del PradoОценок пока нет

- Singapore Industrial Asking Rental Guide (2018.07)Документ8 страницSingapore Industrial Asking Rental Guide (2018.07)Derek OngОценок пока нет

- Franchisee AgreementДокумент17 страницFranchisee AgreementKathyayani KhandavilliОценок пока нет

- Candice SunДокумент1 страницаCandice SunsiegelgallagherОценок пока нет

- Interactive Title and Registration ManualДокумент137 страницInteractive Title and Registration Manualchihuahua8383Оценок пока нет

- Contract of Lease 2019-2020 - Abdukahal, Arbi (Tigbongabong, Tungawan, Zamboanga Sibugay)Документ3 страницыContract of Lease 2019-2020 - Abdukahal, Arbi (Tigbongabong, Tungawan, Zamboanga Sibugay)Enrryson SebastianОценок пока нет

- 7 2020 UP BOC Remedial Law Reviewer Evid OnlyДокумент72 страницы7 2020 UP BOC Remedial Law Reviewer Evid OnlyAnj JosonОценок пока нет

- Deed of Guarantee Mulberry CottageДокумент2 страницыDeed of Guarantee Mulberry CottageJaktronОценок пока нет

- Zudio LOIДокумент11 страницZudio LOIYash ChhabraОценок пока нет

- Far Volume 1, 2 and 3 TheoryДокумент17 страницFar Volume 1, 2 and 3 TheoryKimberly Etulle CelonaОценок пока нет

- University College London - StarRez Portal - Licence AgreementДокумент3 страницыUniversity College London - StarRez Portal - Licence AgreementBenjamin WoodierОценок пока нет

- Quize 14Документ15 страницQuize 14Daniella Mae ElipОценок пока нет

- BBM 442 AssignmentДокумент11 страницBBM 442 AssignmentHashi MohamedОценок пока нет

- Sriram Uppuluri - Apartment Lease AgreementДокумент3 страницыSriram Uppuluri - Apartment Lease AgreementRohit SharmaОценок пока нет

- Ethiopia - Proclomation No. 592-2008 - Banking BusinessДокумент17 страницEthiopia - Proclomation No. 592-2008 - Banking BusinessShewangizaw TasachewОценок пока нет

- 01 Handout FINAC2 Lease Accounting Debt Restructuring PDFДокумент4 страницы01 Handout FINAC2 Lease Accounting Debt Restructuring PDFNil Allen Dizon FajardoОценок пока нет

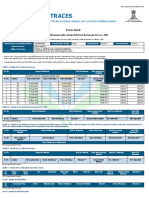

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Документ4 страницыForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Madhukar GuptaОценок пока нет

- 3 - Syed Ahmad Jamal Alganoff (2017) 3 SLR 0386Документ28 страниц3 - Syed Ahmad Jamal Alganoff (2017) 3 SLR 0386LОценок пока нет

- (26.04.2017) Lease Agreement - Lanchang Edible GardenДокумент11 страниц(26.04.2017) Lease Agreement - Lanchang Edible GardensheniОценок пока нет

- Macasiano vs. Diokno, G.R. No. 97764, August 10, 1992 - Full TextДокумент8 страницMacasiano vs. Diokno, G.R. No. 97764, August 10, 1992 - Full TextMarianne Hope VillasОценок пока нет

- Revised TelecommunicationsДокумент27 страницRevised TelecommunicationsPa Rian Rho DoraОценок пока нет

- Initial Draft (CONTRACT OF LEASE)Документ3 страницыInitial Draft (CONTRACT OF LEASE)Jireh Dela Vega AgustinОценок пока нет

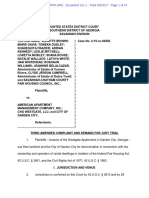

- Westgate & Garden City Third Amended Complaint (Filed)Документ47 страницWestgate & Garden City Third Amended Complaint (Filed)David DawsonОценок пока нет

- DIGEST Llantino v. Co Liong ChongДокумент1 страницаDIGEST Llantino v. Co Liong ChongAyo Lapid100% (1)

- TPA - Important SectionsДокумент2 страницыTPA - Important SectionsRitesh AroraОценок пока нет