Вам также может понравиться

- Plastic IndustryДокумент9 страницPlastic IndustryYepuru ChaithanyaОценок пока нет

- Global Trends For Polypropylene: Basell Polyolefins USA, Inc., Lansing, Michigan, U.S.AДокумент9 страницGlobal Trends For Polypropylene: Basell Polyolefins USA, Inc., Lansing, Michigan, U.S.AAvinash Upmanyu BhardwajОценок пока нет

- Plastics Market: Global Industry Trends and Forecast 2019-2025Документ4 страницыPlastics Market: Global Industry Trends and Forecast 2019-2025RishabhОценок пока нет

- Plastic Packaging Market ReportДокумент21 страницаPlastic Packaging Market ReportAdham SalahОценок пока нет

- HTTP WWW PlastemartДокумент7 страницHTTP WWW PlastemartrishikeshmandawadОценок пока нет

- Khushboo Plastics Project 2Документ42 страницыKhushboo Plastics Project 2vishalОценок пока нет

- Final The Global Paper Industry Today 2018Документ15 страницFinal The Global Paper Industry Today 2018Arthur HutabaratОценок пока нет

- Cutting plastics pollution: Financial measures for a more circular value chainОт EverandCutting plastics pollution: Financial measures for a more circular value chainОценок пока нет

- BOPPДокумент21 страницаBOPPN khade100% (1)

- Plastics - The Facts 2014/2015 An Analysis of European Plastics Production, Demand and Waste DataДокумент34 страницыPlastics - The Facts 2014/2015 An Analysis of European Plastics Production, Demand and Waste DatabaaartazОценок пока нет

- Organization Study (12354Документ39 страницOrganization Study (12354Gobs Mix100% (1)

- Plastics - The Facts 2010: An Analysis of European Plastics Production, Demand and Recovery For 2009Документ32 страницыPlastics - The Facts 2010: An Analysis of European Plastics Production, Demand and Recovery For 2009elylrakОценок пока нет

- Sintex Industries Companyanalysis92384293424Документ16 страницSintex Industries Companyanalysis92384293424Vijay Gohil100% (1)

- 1.1.1 Global Building Materials IndustryДокумент25 страниц1.1.1 Global Building Materials IndustrySiddharth JainОценок пока нет

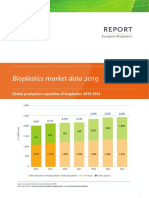

- Report Bioplastics Market Data 2019Документ4 страницыReport Bioplastics Market Data 2019Donato GalloОценок пока нет

- Mining Equipment Industry AnalysisДокумент2 страницыMining Equipment Industry AnalysisMatt SchaveyОценок пока нет

- Hexa Research IncДокумент4 страницыHexa Research Incapi-293819200Оценок пока нет

- Released On 15 July 2014: Email ID-Tel No - 91 2241236650 / +91 - 998 729 5242 Published byДокумент17 страницReleased On 15 July 2014: Email ID-Tel No - 91 2241236650 / +91 - 998 729 5242 Published byapi-258937409Оценок пока нет

- Paint and Coatings Industry OverviewДокумент3 страницыPaint and Coatings Industry OverviewYash VasantaОценок пока нет

- KKKKKKKKДокумент72 страницыKKKKKKKKkirankalkii44Оценок пока нет

- Me News ArticlesДокумент5 страницMe News ArticlesCarla Pianz FampulmeОценок пока нет

- Sahai DistrustGMFoods 2004Документ3 страницыSahai DistrustGMFoods 2004debanshu panwarОценок пока нет

- KKKKKKKKДокумент49 страницKKKKKKKKkirankalkii44Оценок пока нет

- WWF Plastics Consumption Report FinalДокумент15 страницWWF Plastics Consumption Report FinalPooja ShettyОценок пока нет

- Documento Traducido 1Документ6 страницDocumento Traducido 1sergioОценок пока нет

- 0QpUa0LN - Vietnam Plastics BriefingДокумент10 страниц0QpUa0LN - Vietnam Plastics BriefingMiley Minh HuyenОценок пока нет

- BPF Plastics StrategyДокумент66 страницBPF Plastics StrategyPeter EvansОценок пока нет

- Polymer Demand in IndiaДокумент2 страницыPolymer Demand in IndiasarafonlineОценок пока нет

- BP - Strategic Management - The EnvironmentДокумент6 страницBP - Strategic Management - The EnvironmentRoxana OlteanuОценок пока нет

- Plastic Products Cluster - Lahore: Diagnostic StudyДокумент32 страницыPlastic Products Cluster - Lahore: Diagnostic StudynaderpourОценок пока нет

- DURVA SHETYE - International Oil Companies Betting On Renewables - A Right StrategyДокумент4 страницыDURVA SHETYE - International Oil Companies Betting On Renewables - A Right StrategyDurva ShetyeОценок пока нет

- Indian Polymer Industry OutlookДокумент9 страницIndian Polymer Industry OutlookHappy RoxОценок пока нет

- Indian Plastic Industry Exports and GrowthДокумент11 страницIndian Plastic Industry Exports and GrowthAAYUSHI VERMA 7AОценок пока нет

- New Microsoft Office Word DocumentДокумент8 страницNew Microsoft Office Word DocumentShyam KrishnanОценок пока нет

- Market Analysis of Propylene, Water, Tungsten and Isopropyl AlcoholДокумент4 страницыMarket Analysis of Propylene, Water, Tungsten and Isopropyl AlcoholhasanulfiqryОценок пока нет

- Potential of Plastics Industry in Northern India ConferenceДокумент185 страницPotential of Plastics Industry in Northern India ConferenceNishant MishraОценок пока нет

- Ramu Final ProjectДокумент75 страницRamu Final ProjectJayanth.75% (4)

- Recycling Survey 2020 Executive Summary 2Документ17 страницRecycling Survey 2020 Executive Summary 2Nicole Campos CastroОценок пока нет

- Vietnam Plastic Industry Report (EN) - VCBS - 2016 PDFДокумент21 страницаVietnam Plastic Industry Report (EN) - VCBS - 2016 PDFKhoi NguyenОценок пока нет

- Green Industry: A Greener Footprint For IndustryДокумент30 страницGreen Industry: A Greener Footprint For Industryvanhung2809Оценок пока нет

- Plastic Products LahoreДокумент32 страницыPlastic Products LahoreAbdul SattarОценок пока нет

- Latest Industry Statistics ReleasedДокумент2 страницыLatest Industry Statistics ReleasedNicole Campos CastroОценок пока нет

- Biomaterials Development in The Polymer IndustryДокумент6 страницBiomaterials Development in The Polymer Industrydrbasit93Оценок пока нет

- EuroChem - Europe - Final PDFДокумент36 страницEuroChem - Europe - Final PDFYuvrajОценок пока нет

- CFA - Group 7Документ9 страницCFA - Group 7James WayneОценок пока нет

- China On Plastic WastesДокумент3 страницыChina On Plastic WastesNica TemajoОценок пока нет

- Report Bioplastics - Market-Data - 2018Документ4 страницыReport Bioplastics - Market-Data - 2018Jorge Alberto Cuellar BolivarОценок пока нет

- How Is The Global Industrial Gas Market?Документ15 страницHow Is The Global Industrial Gas Market?Anil SrinivasОценок пока нет

- Blowmoldingresinsmarket 200914142651 PDFДокумент7 страницBlowmoldingresinsmarket 200914142651 PDFluan_baОценок пока нет

- UN Docs Compile Global AgreementsДокумент1 страницаUN Docs Compile Global AgreementscobalamyanineОценок пока нет

- Organisational Study On Aglass Manufacturing FirmДокумент61 страницаOrganisational Study On Aglass Manufacturing Firmthis_is_noorОценок пока нет

- Effects of Global and Local Markets Evolution in The Biomass Industry As A Green Business ModelДокумент14 страницEffects of Global and Local Markets Evolution in The Biomass Industry As A Green Business ModelManuel Alejandro Romero HungОценок пока нет

- Final ProjectДокумент66 страницFinal ProjectVikram VrmОценок пока нет

- Assignment 4Документ7 страницAssignment 4Yash DОценок пока нет

- 09 Chapter 2Документ62 страницы09 Chapter 2Chirag KothiyaОценок пока нет

- World Plastics Market Outlook 2015 2030Документ3 страницыWorld Plastics Market Outlook 2015 2030akashdalwadi100% (1)

- Plastic Industry in INDIA (2011 15) : IS AdvisorsДокумент6 страницPlastic Industry in INDIA (2011 15) : IS AdvisorsDilip RkОценок пока нет

- Petrochemicals - A SWOT AnalysisДокумент2 страницыPetrochemicals - A SWOT AnalysisShwet KamalОценок пока нет

- Sarofim Energy White Paper 2012Документ14 страницSarofim Energy White Paper 2012hkm_gmat4849Оценок пока нет

- Packaging Industry FinalДокумент30 страницPackaging Industry FinalUtkarsh Tyagi100% (1)

- Measuring Product Development VitalityДокумент3 страницыMeasuring Product Development VitalityTrevor J. HutleyОценок пока нет

- International Abbreviations For Polymers and Polymer ProcessingДокумент226 страницInternational Abbreviations For Polymers and Polymer ProcessingTrevor J. HutleyОценок пока нет

- Calcium - Carbonate - An Overview PDFДокумент2 страницыCalcium - Carbonate - An Overview PDFTrevor J. HutleyОценок пока нет

- Overview Polymer ProcessingДокумент9 страницOverview Polymer ProcessingTrevor J. HutleyОценок пока нет

- Origin of Toughness in B-Polypropylene: The Effect of Molecular Mobility in The Amorphous PhaseДокумент8 страницOrigin of Toughness in B-Polypropylene: The Effect of Molecular Mobility in The Amorphous PhaseTrevor J. HutleyОценок пока нет

- Polymer Structure3Документ29 страницPolymer Structure3roscillaОценок пока нет

- ADL Innovation For Economic DiversificationДокумент8 страницADL Innovation For Economic DiversificationTrevor J. HutleyОценок пока нет

- The Imagination GapДокумент5 страницThe Imagination GapTrevor J. HutleyОценок пока нет

- PWC Middle East CEO Survey 2014Документ13 страницPWC Middle East CEO Survey 2014Trevor J. HutleyОценок пока нет

- BPF Industry Directory 2016Документ36 страницBPF Industry Directory 2016Trevor J. HutleyОценок пока нет

- Catching The Asia Petrochemical Boom - A Polyolefin PerspectiveДокумент7 страницCatching The Asia Petrochemical Boom - A Polyolefin PerspectiveTrevor J. HutleyОценок пока нет

- Huawei WS320 - User - Guide PDFДокумент49 страницHuawei WS320 - User - Guide PDFTrevor J. HutleyОценок пока нет

- Appendix B - Trade NamesДокумент29 страницAppendix B - Trade NamesTrevor J. HutleyОценок пока нет

- TRL Definitions PDFДокумент1 страницаTRL Definitions PDFBHARadwajОценок пока нет

- EMET Technical ProgramДокумент8 страницEMET Technical ProgramTrevor J. HutleyОценок пока нет

- Paint & Coatings Industry August 2014Документ56 страницPaint & Coatings Industry August 2014Trevor J. Hutley100% (1)

- USP 3.755,237 W R Grace 1973Документ7 страницUSP 3.755,237 W R Grace 1973Trevor J. HutleyОценок пока нет

- TPXДокумент1 страницаTPXTrevor J. HutleyОценок пока нет

- USP 3112300 Isotactic Polypropylene Giulio NattaДокумент11 страницUSP 3112300 Isotactic Polypropylene Giulio NattaTrevor J. HutleyОценок пока нет

- New Olefin Production Technologies in SINOPECДокумент10 страницNew Olefin Production Technologies in SINOPECTrevor J. HutleyОценок пока нет

- Models and Theory of Polymer RheologyДокумент49 страницModels and Theory of Polymer RheologyTrevor J. HutleyОценок пока нет

- Lectures in Polymer PhysicsДокумент24 страницыLectures in Polymer PhysicsTrevor J. HutleyОценок пока нет

- Introducing and Supporting Speciality Polymer (EVA) Applications GPCA PlastCon 7-9 April 2013 FINAL 8-4-13Документ52 страницыIntroducing and Supporting Speciality Polymer (EVA) Applications GPCA PlastCon 7-9 April 2013 FINAL 8-4-13Trevor J. HutleyОценок пока нет

- Strategic Approaches To Science and Technology in DevelopmentДокумент62 страницыStrategic Approaches To Science and Technology in DevelopmentTrevor J. HutleyОценок пока нет

- When Composites Technology Followed The Serendipitous Path To DiscoveryДокумент7 страницWhen Composites Technology Followed The Serendipitous Path To DiscoveryTrevor J. HutleyОценок пока нет

- Ldpe 4 PDFДокумент13 страницLdpe 4 PDFOkePreciousEmmanuelОценок пока нет

- Mcleish ReviewДокумент149 страницMcleish ReviewTrevor J. HutleyОценок пока нет

- Compounding World 2008-12Документ34 страницыCompounding World 2008-12Trevor J. HutleyОценок пока нет

- Fuel Synthesis From SyngasДокумент9 страницFuel Synthesis From SyngasTrevor J. HutleyОценок пока нет

- Andrew Linklater - The Transformation of Political Community - E H Carr, Critical Theory and International RelationsДокумент19 страницAndrew Linklater - The Transformation of Political Community - E H Carr, Critical Theory and International Relationsmaria luizaОценок пока нет

- Sample Interview Questions for Motivation, Communication, TeamsДокумент6 страницSample Interview Questions for Motivation, Communication, TeamsSahibzada Muhammad MubeenОценок пока нет

- Biomérieux 21342 Vitek 2 GP: Intended UseДокумент19 страницBiomérieux 21342 Vitek 2 GP: Intended UserezaОценок пока нет

- Tutorial Backpropagation Neural NetworkДокумент10 страницTutorial Backpropagation Neural NetworkHeru PraОценок пока нет

- Current Developments in Testing Item Response Theory (IRT) : Prepared byДокумент32 страницыCurrent Developments in Testing Item Response Theory (IRT) : Prepared byMalar VengadesОценок пока нет

- So You Want To Be A NeurosugeonДокумент10 страницSo You Want To Be A NeurosugeonColby TimmОценок пока нет

- Primavera Inspire For Sap: Increased Profitability Through Superior TransparencyДокумент4 страницыPrimavera Inspire For Sap: Increased Profitability Through Superior TransparencyAnbu ManoОценок пока нет

- The German eID-Card by Jens BenderДокумент42 страницыThe German eID-Card by Jens BenderPoomjit SirawongprasertОценок пока нет

- Complimentary JournalДокумент58 страницComplimentary JournalMcKey ZoeОценок пока нет

- Business Plan1Документ38 страницBusiness Plan1Gwendolyn PansoyОценок пока нет

- PHILHIS Executive Summary - EditedДокумент7 страницPHILHIS Executive Summary - EditedMaxy Bariacto100% (1)

- ManuscriptДокумент2 страницыManuscriptVanya QuistoОценок пока нет

- Seminar 6 Precision AttachmentsДокумент30 страницSeminar 6 Precision AttachmentsAmit Sadhwani67% (3)

- Amna Hameed: ObjectiveДокумент2 страницыAmna Hameed: ObjectiveSabrina GandapurОценок пока нет

- 50 Ways To Balance MagicДокумент11 страниц50 Ways To Balance MagicRodolfo AlencarОценок пока нет

- 20comm Um003 - en PДокумент270 страниц20comm Um003 - en PRogério BotelhoОценок пока нет

- Sexual & Reproductive Health of AdolocentsДокумент8 страницSexual & Reproductive Health of AdolocentsSourav HossenОценок пока нет

- Sample of Accident Notification & Investigation ProcedureДокумент2 страницыSample of Accident Notification & Investigation Procedurerajendhar100% (1)

- L P 10Документ13 страницL P 10Bình Minh HoàngОценок пока нет

- Ownership and Governance of State Owned Enterprises A Compendium of National Practices 2021Документ104 страницыOwnership and Governance of State Owned Enterprises A Compendium of National Practices 2021Ary Surya PurnamaОценок пока нет

- 02 - Order Quantities When Demand Is Approximately LevelДокумент2 страницы02 - Order Quantities When Demand Is Approximately Levelrahma.samyОценок пока нет

- F&B Data Analyst Portfolio ProjectДокумент12 страницF&B Data Analyst Portfolio ProjectTom HollandОценок пока нет

- Teaching Support Untuk Managemen HRДокумент102 страницыTeaching Support Untuk Managemen HRFernando FmchpОценок пока нет

- Professional Builder - Agosto 2014Документ32 страницыProfessional Builder - Agosto 2014ValОценок пока нет

- Self ReflectivityДокумент7 страницSelf ReflectivityJoseph Jajo100% (1)

- Quality Management - QuestionДокумент4 страницыQuality Management - QuestionLawzy Elsadig SeddigОценок пока нет

- Direction: Read The Questions Carefully. Write The Letters of The Correct AnswerДокумент3 страницыDirection: Read The Questions Carefully. Write The Letters of The Correct AnswerRomyross JavierОценок пока нет

- Asus X553MA Repair Guide Rev2.0Документ7 страницAsus X553MA Repair Guide Rev2.0UMA AKANDU UCHEОценок пока нет

- Strata KT Office OpportunityДокумент41 страницаStrata KT Office OpportunitySanskar SurekaОценок пока нет

- C++ NotesДокумент129 страницC++ NotesNikhil Kant Saxena100% (4)