Вам также может понравиться

- Unit 1Документ72 страницыUnit 1Sumit SoniОценок пока нет

- Unit 1 - Management AccountingДокумент16 страницUnit 1 - Management Accountingdilipkumar.1267Оценок пока нет

- MANAGEMENT ACCOUNTINg Unit-1Документ49 страницMANAGEMENT ACCOUNTINg Unit-1Vishwas AgarwalОценок пока нет

- Management Accounting Definition and FunctionsДокумент16 страницManagement Accounting Definition and FunctionsRahul kumar100% (1)

- Meaning and Definition of Management AccountingДокумент93 страницыMeaning and Definition of Management AccountingJean Fajardo BadilloОценок пока нет

- Bcom 203Документ134 страницыBcom 203Dharmesh GoyalОценок пока нет

- Management Accounting - An OverviewДокумент14 страницManagement Accounting - An OverviewMadhurGuptaОценок пока нет

- Management AccountingДокумент13 страницManagement AccountingEricka BautistaОценок пока нет

- Management AccountingДокумент132 страницыManagement Accountingaanchal singhОценок пока нет

- Management Accounting - SBA1501: Unit - IДокумент9 страницManagement Accounting - SBA1501: Unit - ISubhasri RajaОценок пока нет

- Lesson 1: Introduction To Management Accounting: Learning ObjectivesДокумент5 страницLesson 1: Introduction To Management Accounting: Learning ObjectivesShivani GuptaОценок пока нет

- Management_Accounting-February 2024Документ51 страницаManagement_Accounting-February 2024Somesh AgrawalОценок пока нет

- management accounting notesДокумент80 страницmanagement accounting notesnuk.2021018028Оценок пока нет

- Acct 232 Management and Cost Accounting IiДокумент14 страницAcct 232 Management and Cost Accounting IipfungwaОценок пока нет

- Projects Ma 1Документ16 страницProjects Ma 1nikkiОценок пока нет

- Fa 1Документ18 страницFa 1Rahul KotagiriОценок пока нет

- 2 Zapya StatiscДокумент10 страниц2 Zapya StatiscLOND SONОценок пока нет

- Chapter I: Management and The Nature of Management AccountingДокумент11 страницChapter I: Management and The Nature of Management AccountingMark ManuntagОценок пока нет

- Managerial Accounting Lecture 1stДокумент8 страницManagerial Accounting Lecture 1stkhizarniazОценок пока нет

- Management Accounting NotesДокумент72 страницыManagement Accounting NotesALLU SRISAIОценок пока нет

- Management AccountingДокумент135 страницManagement Accountingdibakardas10017100% (1)

- Management AccountingДокумент18 страницManagement AccountingmayankОценок пока нет

- Hrithik kamble hkДокумент36 страницHrithik kamble hkHRITHIK KambleОценок пока нет

- Copy Cost Accting-1Документ205 страницCopy Cost Accting-1Kassawmar DesalegnОценок пока нет

- Nature and Objectives of Management AccountingДокумент13 страницNature and Objectives of Management AccountingpfungwaОценок пока нет

- Introduction to Management AccountingДокумент12 страницIntroduction to Management Accountingmannat sethiОценок пока нет

- Cost & Mgt. Acct - I, Lecture Note - Chapter 1 & 2Документ35 страницCost & Mgt. Acct - I, Lecture Note - Chapter 1 & 2Yonas BamlakuОценок пока нет

- Introduction To Managerial AccountingДокумент10 страницIntroduction To Managerial AccountingMark Ronnier VedañaОценок пока нет

- Meaning and Definitions of Management AccountingДокумент9 страницMeaning and Definitions of Management AccountingHafizullah Ansari100% (1)

- Intro to Managerial AcctДокумент9 страницIntro to Managerial AcctMark Ronnier VedañaОценок пока нет

- Module 4 Management AccountingДокумент14 страницModule 4 Management AccountingRajimol KPОценок пока нет

- Characteristics/Nature of Management AccountingДокумент7 страницCharacteristics/Nature of Management Accountingritu paudelОценок пока нет

- Manage Acctg Provides Info for Decision MakingДокумент24 страницыManage Acctg Provides Info for Decision MakingguptaorchidОценок пока нет

- Manage Acct Ch 1Документ24 страницыManage Acct Ch 1Zaid ZatariОценок пока нет

- The Nature and Purpose of Accounting ExplainedДокумент16 страницThe Nature and Purpose of Accounting ExplainedSubashiиy PяabakaяaиОценок пока нет

- Management Accounting IntroductionДокумент45 страницManagement Accounting IntroductionK DevikaОценок пока нет

- Abdel Razza Khoirie-185020307141016-Assignment 1Документ5 страницAbdel Razza Khoirie-185020307141016-Assignment 1Abdel RazzaОценок пока нет

- MANAGEMENT ACCOUNTINGДокумент35 страницMANAGEMENT ACCOUNTINGshimmuuОценок пока нет

- Organization of Management AccountingДокумент3 страницыOrganization of Management AccountingRidwanullah ramadaniОценок пока нет

- Management Accounting Notes at Mba BKДокумент134 страницыManagement Accounting Notes at Mba BKBabasab Patil (Karrisatte)Оценок пока нет

- Management Accounting (Bba32) Unit - IДокумент42 страницыManagement Accounting (Bba32) Unit - IT S Kumar KumarОценок пока нет

- Management Accounting and The Modern Business EnvironmentДокумент6 страницManagement Accounting and The Modern Business EnvironmentdevajeetbaruahОценок пока нет

- Chapter 1 IntroductionДокумент40 страницChapter 1 IntroductionSoka PokaОценок пока нет

- Management Accounting Mba BKДокумент138 страницManagement Accounting Mba BKBabasab Patil (Karrisatte)100% (1)

- Management Accounting: DefinitionДокумент5 страницManagement Accounting: DefinitionSangram PandaОценок пока нет

- Introduction To Managerial AccountingДокумент6 страницIntroduction To Managerial AccountingMark Ronnier VedañaОценок пока нет

- Management AccountingДокумент5 страницManagement Accountingτυσηαρ ηαβιβОценок пока нет

- CH. 1 Introduction To Management AccountingДокумент15 страницCH. 1 Introduction To Management Accountingdivyakumbhar18Оценок пока нет

- Management AccountingДокумент36 страницManagement AccountingSreepada KameswariОценок пока нет

- Project Mahindra Finance PVT LTDДокумент63 страницыProject Mahindra Finance PVT LTDSpandana Shetty75% (4)

- Strategic Cost Management GuideДокумент27 страницStrategic Cost Management GuideGabrielle Anne MagsanocОценок пока нет

- Intro to Management Accounting FunctionsДокумент12 страницIntro to Management Accounting FunctionskipovoОценок пока нет

- Management AccountingДокумент24 страницыManagement AccountingRajat ChauhanОценок пока нет

- New Microsoft Office Word Document-1Документ73 страницыNew Microsoft Office Word Document-1Toshar JindalОценок пока нет

- Management AccountingДокумент358 страницManagement AccountingAsifHossain100% (8)

- Saya Sedang Berbagi '7. Belkaoui - Behavioral Management Accounting - 2002' Dengan Anda-Halaman-14-54Документ41 страницаSaya Sedang Berbagi '7. Belkaoui - Behavioral Management Accounting - 2002' Dengan Anda-Halaman-14-54ghina adhha hauraОценок пока нет

- Notes - Management AccountingДокумент54 страницыNotes - Management Accountingbenjoel1209Оценок пока нет

- Accounting NotesДокумент11 страницAccounting Noteszabi ullah MohammadiОценок пока нет

- Finance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersОт EverandFinance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersОценок пока нет

- Cable Part CodeДокумент2 страницыCable Part Codesaneesh81Оценок пока нет

- 600 625 Kva DV 12 Powered GensetsДокумент12 страниц600 625 Kva DV 12 Powered Gensetssaneesh81Оценок пока нет

- AMFi Range Training - 01Документ33 страницыAMFi Range Training - 01saneesh81Оценок пока нет

- Battery AH Cable SizeДокумент1 страницаBattery AH Cable Sizesaneesh81Оценок пока нет

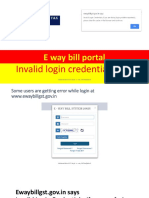

- Fix invalid login error ewaybillgst portalДокумент13 страницFix invalid login error ewaybillgst portalMagdum EngineeringОценок пока нет

- Low Budget Duplex House Design With Modern Exterior - : 19 Lakh For ConstructionДокумент3 страницыLow Budget Duplex House Design With Modern Exterior - : 19 Lakh For Constructionsaneesh81Оценок пока нет

- Kuv100 e Brochure Aug 2019Документ4 страницыKuv100 e Brochure Aug 2019DiditlkgxulrsОценок пока нет

- Cable Size For DG SetДокумент1 страницаCable Size For DG Setsaneesh81Оценок пока нет

- Funnel Presentation For Field TeamДокумент12 страницFunnel Presentation For Field Teamsaneesh81Оценок пока нет

- Untitled PDFДокумент35 страницUntitled PDFSafeer EdaloliОценок пока нет

- Master ECU wiring diagram componentsДокумент1 страницаMaster ECU wiring diagram componentssaneesh81Оценок пока нет

- USD Money Transfer Details Through Top US BanksДокумент2 страницыUSD Money Transfer Details Through Top US Bankssaneesh810% (1)

- ECEL Snap Ring ActivityДокумент5 страницECEL Snap Ring Activitysaneesh81Оценок пока нет

- Funnel Presentation For Field TeamДокумент12 страницFunnel Presentation For Field Teamsaneesh81Оценок пока нет

- Small Double Oor House Plan With 3 Bedroom and Stunning ExteriorДокумент3 страницыSmall Double Oor House Plan With 3 Bedroom and Stunning Exteriorsaneesh81Оценок пока нет

- KMSCL e-Tender for Supply and Installation of Diesel Generator 40KVAДокумент76 страницKMSCL e-Tender for Supply and Installation of Diesel Generator 40KVAsaneesh81Оценок пока нет

- MTU 4R0120 DS125: Diesel Generator SetДокумент4 страницыMTU 4R0120 DS125: Diesel Generator Setsaneesh81Оценок пока нет

- Kseb Payment SlipДокумент1 страницаKseb Payment Slipsaneesh81Оценок пока нет

- 3 - 5 Kva Portable Kirloskar LeafletДокумент2 страницы3 - 5 Kva Portable Kirloskar Leafletsaneesh81Оценок пока нет

- Amf ControllerДокумент14 страницAmf Controllersaneesh81Оценок пока нет

- SEAMLESS LUXURY WITH FENESTA'S SYSTEM ALUMINIUM WINDOWS AND DOORSДокумент21 страницаSEAMLESS LUXURY WITH FENESTA'S SYSTEM ALUMINIUM WINDOWS AND DOORSsaneesh81Оценок пока нет

- SX-HS Series New1Документ19 страницSX-HS Series New1saneesh81Оценок пока нет

- Kg545 II UserДокумент86 страницKg545 II Usersaneesh81100% (1)

- JCB Catalogue AДокумент9 страницJCB Catalogue Asaneesh81100% (2)

- Marks Total MarksДокумент3 страницыMarks Total Markssaneesh81Оценок пока нет

- Volvo - Eicher AdvДокумент3 страницыVolvo - Eicher Advsaneesh81Оценок пока нет

- Bba404 SLM Unit 01Документ21 страницаBba404 SLM Unit 01saneesh81Оценок пока нет

- Diesel Generator SetДокумент1 страницаDiesel Generator Setsaneesh81100% (1)

- BB0015 Quality Management MQPДокумент13 страницBB0015 Quality Management MQPsaneesh81Оценок пока нет

- Oil Money 2015 BrochureДокумент6 страницOil Money 2015 BrochureTwirXОценок пока нет

- Solution WileyPlus COMM 305 / ACCO 240Документ62 страницыSolution WileyPlus COMM 305 / ACCO 240Léo Audibert100% (2)

- Fin1 Eq2 BsatДокумент1 страницаFin1 Eq2 BsatYu BabylanОценок пока нет

- Standalone Financial Results, Limited Review Report For September 30, 2016 (Result)Документ5 страницStandalone Financial Results, Limited Review Report For September 30, 2016 (Result)Shyam SunderОценок пока нет

- India's Cost of Capital: A Survey: January 2014Документ16 страницIndia's Cost of Capital: A Survey: January 2014Jeanette JenaОценок пока нет

- Mother DairyДокумент16 страницMother DairyMano VikasОценок пока нет

- Professionalpractice 160908192356Документ25 страницProfessionalpractice 160908192356Ar Princy MarthaОценок пока нет

- The Roi CalculationДокумент3 страницыThe Roi CalculationSasaОценок пока нет

- Acctng Reviewer 2Документ21 страницаAcctng Reviewer 2alliahnah33% (3)

- What is Fedwire? Understanding the Federal Reserve Wire NetworkДокумент17 страницWhat is Fedwire? Understanding the Federal Reserve Wire NetworkVijai RaghavanОценок пока нет

- MT Morris: Downtown Revitalization in Rural New York StateДокумент29 страницMT Morris: Downtown Revitalization in Rural New York StateprobrockportОценок пока нет

- C4 GoldenДокумент4 страницыC4 GoldenJonuelin Infante100% (1)

- SanDisk Corporation Equity Valuation AnalysisДокумент6 страницSanDisk Corporation Equity Valuation AnalysisBrant HammerОценок пока нет

- Cost of Capital Components Debt Preferred Common Equity WaccДокумент55 страницCost of Capital Components Debt Preferred Common Equity Waccfaisal_stylishОценок пока нет

- Bond Amortization ScheduleДокумент10 страницBond Amortization ScheduleVidya IntaniОценок пока нет

- The Stochastic Oscillator - A Harmonious System of TradingДокумент9 страницThe Stochastic Oscillator - A Harmonious System of TradingMirabo AndreeaОценок пока нет

- Behavioural Finance: Theory and SurveyДокумент6 страницBehavioural Finance: Theory and SurveymbapritiОценок пока нет

- The Zone Issue 27Документ16 страницThe Zone Issue 27Jeff Clay GarciaОценок пока нет

- Assignment On JournalДокумент4 страницыAssignment On JournalNIKHIL GUPTAОценок пока нет

- JM Financial Mutual FundДокумент2 страницыJM Financial Mutual FundJohn WilliamsОценок пока нет

- Capital Budgeting: Session 3Документ50 страницCapital Budgeting: Session 3Isaack MgeniОценок пока нет

- Adjudication Order in Respect of Mr. Bikramjit Ahluwalia and Others in The Matter of Ahlcon Parenterals India) LTDДокумент9 страницAdjudication Order in Respect of Mr. Bikramjit Ahluwalia and Others in The Matter of Ahlcon Parenterals India) LTDShyam SunderОценок пока нет

- AAIB Fixed Income Fund (Gozoor) : Fact Sheet JuneДокумент2 страницыAAIB Fixed Income Fund (Gozoor) : Fact Sheet Juneapi-237717884Оценок пока нет

- 03FM SM Ch3 1LPДокумент6 страниц03FM SM Ch3 1LPjoebloggs18880% (1)

- Converged Systems Sales PlaybookДокумент12 страницConverged Systems Sales PlaybookPeter Stone100% (3)

- HUL Financial AnalysisДокумент11 страницHUL Financial AnalysisAbhishek Khanna0% (1)

- SSS VacancyДокумент61 страницаSSS VacancyCess AyomaОценок пока нет

- Regional CSHP report for NCR projects in September 2017Документ53 страницыRegional CSHP report for NCR projects in September 2017JohnmoiОценок пока нет

- Maid FormДокумент2 страницыMaid FormhutuguoОценок пока нет

- Distressed Debt Investing - Trade Claims PrimerДокумент7 страницDistressed Debt Investing - Trade Claims Primer10Z2Оценок пока нет