Вам также может понравиться

- A-level Physics Revision: Cheeky Revision ShortcutsОт EverandA-level Physics Revision: Cheeky Revision ShortcutsРейтинг: 3 из 5 звезд3/5 (10)

- Mechanical Vibration Lab ReportДокумент7 страницMechanical Vibration Lab ReportChris NichollsОценок пока нет

- Jeremy Silman - The Reassess Your Chess WorkbookДокумент220 страницJeremy Silman - The Reassess Your Chess Workbookalan_du2264590% (29)

- Linear Algebra Cheat SheetДокумент2 страницыLinear Algebra Cheat SheetBrian WilliamsonОценок пока нет

- SSA Beginners Guide v9Документ22 страницыSSA Beginners Guide v9김진석Оценок пока нет

- Multivariate Data Analysis: Universiteit Van AmsterdamДокумент28 страницMultivariate Data Analysis: Universiteit Van AmsterdamcfisicasterОценок пока нет

- Higham Siam Sde ReviewДокумент22 страницыHigham Siam Sde ReviewAlex ChenОценок пока нет

- 6415 Ijdps 01Документ13 страниц6415 Ijdps 01ijdpsОценок пока нет

- Heat Equation in Partial DimensionsДокумент27 страницHeat Equation in Partial DimensionsRameezz WaajidОценок пока нет

- Taylor's Theorem and Its ApplicationsДокумент20 страницTaylor's Theorem and Its ApplicationseracksОценок пока нет

- Markov Processes, Lab 2Документ6 страницMarkov Processes, Lab 2Duc-Duy Pham NguyenОценок пока нет

- Planar Trusses Solution Via Numerical MethodДокумент42 страницыPlanar Trusses Solution Via Numerical MethodIzzaty RoslanОценок пока нет

- INTLAB TutorialДокумент50 страницINTLAB TutorialHeitor JuniorОценок пока нет

- CS1114: Study Guide 1: 1 Finding The Center of Things: Bounding Boxes, Cen-Troids, Trimmed Means, and MediansДокумент9 страницCS1114: Study Guide 1: 1 Finding The Center of Things: Bounding Boxes, Cen-Troids, Trimmed Means, and Medianslightsaber5Оценок пока нет

- ApplicationsДокумент12 страницApplicationskkkprotОценок пока нет

- Some Efficient Heuristic Methods For The Flow Shop Sequencing ProblemДокумент21 страницаSome Efficient Heuristic Methods For The Flow Shop Sequencing ProblemDeba SahooОценок пока нет

- Modeling and Simulation of Dynamic Systems: Lecture Notes of ME 862Документ9 страницModeling and Simulation of Dynamic Systems: Lecture Notes of ME 862RajrdbОценок пока нет

- MWN 780 Assignment1 Block 1Документ5 страницMWN 780 Assignment1 Block 1DenielОценок пока нет

- 7 Variance Reduction Techniques: 7.1 Common Random NumbersДокумент5 страниц7 Variance Reduction Techniques: 7.1 Common Random NumbersjarameliОценок пока нет

- Observer Hybrid Systems 4Документ12 страницObserver Hybrid Systems 4Paulina MarquezОценок пока нет

- Computer Algorithms For Solving The SCHR Odinger and Poisson EquationsДокумент9 страницComputer Algorithms For Solving The SCHR Odinger and Poisson EquationsJoyee BasuОценок пока нет

- Assimilation AlgorithmsДокумент30 страницAssimilation AlgorithmsaminaОценок пока нет

- Error Analysis For IPhO ContestantsДокумент11 страницError Analysis For IPhO ContestantsnurlubekОценок пока нет

- Triangles Train AlgorithmДокумент12 страницTriangles Train Algorithmputih_138242459Оценок пока нет

- MTamis ConstraintBasedPhysicsSolverДокумент31 страницаMTamis ConstraintBasedPhysicsSolverlucianobuglioniОценок пока нет

- A General Approach To Multiple Precesion Point Motion Generation by 4-Bar LinkageДокумент25 страницA General Approach To Multiple Precesion Point Motion Generation by 4-Bar LinkageAbhinaba MaitraОценок пока нет

- Implementasi Program Software Matlab Dalam Memecahkan Kasus Fisika: Dinamika Sistem Massa Dan Pegas (Prinsip Nilai Dan Vektor Eigen)Документ8 страницImplementasi Program Software Matlab Dalam Memecahkan Kasus Fisika: Dinamika Sistem Massa Dan Pegas (Prinsip Nilai Dan Vektor Eigen)Azka FathiaОценок пока нет

- Hasbun PosterДокумент21 страницаHasbun PosterSuhailUmarОценок пока нет

- Mathematical Association of AmericaДокумент17 страницMathematical Association of AmericaAlim SultangazinОценок пока нет

- Lab Report - OscilloscopeДокумент3 страницыLab Report - Oscilloscopehyeon님Оценок пока нет

- Signals and Systems Using MatlabДокумент68 страницSignals and Systems Using MatlabSavio S100% (6)

- Time Series Similarity MeasureДокумент9 страницTime Series Similarity MeasureDiego Fustes VilladónigaОценок пока нет

- Improving Middle Square Method RNG Using. 2011Документ5 страницImproving Middle Square Method RNG Using. 2011MustikaSariОценок пока нет

- Intro To Dynamic ProgrammingДокумент7 страницIntro To Dynamic ProgrammingUtkarsh PatelОценок пока нет

- Introduction To MATLAB 3rd Ed Etter ProblemsДокумент11 страницIntroduction To MATLAB 3rd Ed Etter ProblemsAndy OcegueraОценок пока нет

- Dimensional Analysis and Scaling: 1.1 Mathematical ModelsДокумент29 страницDimensional Analysis and Scaling: 1.1 Mathematical ModelslynnetanОценок пока нет

- Dynamics and Control Design Via LQR and Sdre Methods For A Maglev SystemДокумент13 страницDynamics and Control Design Via LQR and Sdre Methods For A Maglev SystemVinay KashyapОценок пока нет

- MCMC Final EditionДокумент17 страницMCMC Final EditionYou ZhaoОценок пока нет

- Implementing The RSA Cryptosystem With Maxima CASДокумент20 страницImplementing The RSA Cryptosystem With Maxima CASjoaquin murgadeОценок пока нет

- H2 Measurement 2012Документ21 страницаH2 Measurement 2012Ronnie QuekОценок пока нет

- Numerical Solution of Third Order Time-Invariant Linear Differential Equations by Adomian Decomposition MethodДокумент5 страницNumerical Solution of Third Order Time-Invariant Linear Differential Equations by Adomian Decomposition MethodtheijesОценок пока нет

- Algo Trading Assignment 1 ColumbiaДокумент1 страницаAlgo Trading Assignment 1 ColumbiaAditya JainОценок пока нет

- Lecture Notes On Finite Element Methods For Partial Differential EquationsДокумент106 страницLecture Notes On Finite Element Methods For Partial Differential EquationsEndless LoveОценок пока нет

- 2015WimoTriangleTrianglePublished PDFДокумент9 страниц2015WimoTriangleTrianglePublished PDFAlexgh1993Оценок пока нет

- Proper Orthogonal DecompositionДокумент10 страницProper Orthogonal DecompositionKenry Xu ChiОценок пока нет

- Algorithm Report PDFДокумент6 страницAlgorithm Report PDFWaleed KhanОценок пока нет

- Presentation Advanced Structural Dynamics FinДокумент57 страницPresentation Advanced Structural Dynamics FinandyronaldoОценок пока нет

- Algorithm Report PDFДокумент6 страницAlgorithm Report PDFWaleed KhanОценок пока нет

- Math 243M, Numerical Linear Algebra Lecture NotesДокумент71 страницаMath 243M, Numerical Linear Algebra Lecture NotesRonaldОценок пока нет

- Statistics 1 - NotesДокумент22 страницыStatistics 1 - Notesryanb97Оценок пока нет

- Numerical Solution of Initial Value ProblemsДокумент17 страницNumerical Solution of Initial Value ProblemslambdaStudent_eplОценок пока нет

- Recipe For PHY 107Документ37 страницRecipe For PHY 107Midhun K ThankachanОценок пока нет

- Linear RegressionДокумент4 страницыLinear RegressionHemant GargОценок пока нет

- GreedyДокумент22 страницыGreedylarymarklaryОценок пока нет

- Merge Sort: Divide and ConquerДокумент18 страницMerge Sort: Divide and ConquervinithОценок пока нет

- Averaging Oscillations With Small Fractional Damping and Delayed TermsДокумент20 страницAveraging Oscillations With Small Fractional Damping and Delayed TermsYogesh DanekarОценок пока нет

- EEE350 Control Systems: Assignment 2Документ15 страницEEE350 Control Systems: Assignment 2Nur AfiqahОценок пока нет

- Matrices with MATLAB (Taken from "MATLAB for Beginners: A Gentle Approach")От EverandMatrices with MATLAB (Taken from "MATLAB for Beginners: A Gentle Approach")Рейтинг: 3 из 5 звезд3/5 (4)

- Commercial Real Estate and The Economy v2Документ20 страницCommercial Real Estate and The Economy v2viktor6Оценок пока нет

- Current Priorities of GovernmentДокумент1 страницаCurrent Priorities of Governmentviktor6Оценок пока нет

- Silat Meeting 201112 NotesДокумент3 страницыSilat Meeting 201112 Notesviktor6Оценок пока нет

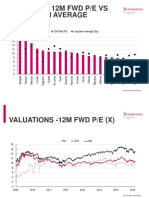

- 18 20 12M FWD P/E Long-Term Average (5yr)Документ10 страниц18 20 12M FWD P/E Long-Term Average (5yr)viktor6Оценок пока нет

- MSCI Nov15 INTSummaryДокумент59 страницMSCI Nov15 INTSummaryviktor6Оценок пока нет

- Fund Flows Geo Focus Table - 05022016Документ1 страницаFund Flows Geo Focus Table - 05022016viktor6Оценок пока нет

- EMEA pt2Документ20 страницEMEA pt2viktor6Оценок пока нет

- Fund Flows Geo Focus Table - 10022016Документ1 страницаFund Flows Geo Focus Table - 10022016viktor6Оценок пока нет

- Singapore Institute of Management: University of London Preliminary Exam 2015Документ5 страницSingapore Institute of Management: University of London Preliminary Exam 2015viktor6Оценок пока нет

- Frontier Pt2Документ20 страницFrontier Pt2viktor6Оценок пока нет

- Chapter SixДокумент234 страницыChapter Sixviktor6Оценок пока нет

- P FM Credit Policy BriefДокумент16 страницP FM Credit Policy Briefviktor6Оценок пока нет

- Eigenvalues and Eigenvectors: An: Example. Consider The MatrixДокумент23 страницыEigenvalues and Eigenvectors: An: Example. Consider The MatrixlsvikneshОценок пока нет

- Math 9 PDFДокумент174 страницыMath 9 PDFArslan HaiderОценок пока нет

- 2 - Trigonometry and Advance MathДокумент5 страниц2 - Trigonometry and Advance MathRichelle Calandria VedadОценок пока нет

- Application of AVX (Advanced Vector Extensions) For Improved PDFДокумент8 страницApplication of AVX (Advanced Vector Extensions) For Improved PDFRichieQCОценок пока нет

- 9th Math EnglishДокумент319 страниц9th Math EnglishHAFIZ IMTIAZ ALIОценок пока нет

- Business MathematicsДокумент346 страницBusiness Mathematicssohail bangashОценок пока нет

- PETE-560 Mathematical Methods in Petroleum Engineering Lecture Notes Chapter # 5 6.1 Linear AlgebraДокумент50 страницPETE-560 Mathematical Methods in Petroleum Engineering Lecture Notes Chapter # 5 6.1 Linear AlgebratayyabmujahidОценок пока нет

- Convolution: 8.1. Linear Translation Invariant (LTI or LSI) OperatorsДокумент9 страницConvolution: 8.1. Linear Translation Invariant (LTI or LSI) OperatorsAnonymous OOeTGKMAdDОценок пока нет

- SR Secondary Maths Text BookДокумент578 страницSR Secondary Maths Text BookVamsidhar ReddyОценок пока нет

- Ometry B098MMT32KДокумент472 страницыOmetry B098MMT32KEh PhotographyОценок пока нет

- PVDnotesДокумент160 страницPVDnotessvhanu4010Оценок пока нет

- Untitled 2Документ81 страницаUntitled 2JEAN KATHLEEN SORIANOОценок пока нет

- Applications of Linear AlgebraДокумент45 страницApplications of Linear AlgebraSisitha100% (1)

- MassartHandbook of Qualimetrics Part B PDFДокумент708 страницMassartHandbook of Qualimetrics Part B PDFLiliana ForzaniОценок пока нет

- Bridge Course Meterial OriginalДокумент83 страницыBridge Course Meterial OriginalAswin Thangaraju0% (1)

- MTH603 - Midterm Solved Mcqs and Quizes by MoaazДокумент18 страницMTH603 - Midterm Solved Mcqs and Quizes by MoaazusmanОценок пока нет

- MatrixДокумент9 страницMatrixMonower H SarkerОценок пока нет

- Group Project Team1Документ58 страницGroup Project Team1Aasika AasikaОценок пока нет

- Matrices PDFДокумент13 страницMatrices PDFRJ Baluyot MontallaОценок пока нет

- 703 Whats New in The Accelerate FrameworkДокумент162 страницы703 Whats New in The Accelerate Frameworkclungaho7109Оценок пока нет

- Matrix Algebra For Engineers PDFДокумент108 страницMatrix Algebra For Engineers PDFRosella LunaОценок пока нет

- CHAPTER1LinearEquationsandMatrices - Son (Compatibility Mode)Документ65 страницCHAPTER1LinearEquationsandMatrices - Son (Compatibility Mode)Anonymous wrtUShmQFОценок пока нет

- Factorsynth3 ManualДокумент17 страницFactorsynth3 ManualAnonymous uFZHfqpBОценок пока нет

- Data StructureДокумент393 страницыData Structuresem notesОценок пока нет

- Three Matlab Implementations of The Lowest-Order Raviart-Thomas Mfem With A Posteriori Error ControlДокумент29 страницThree Matlab Implementations of The Lowest-Order Raviart-Thomas Mfem With A Posteriori Error ControlPankaj SahlotОценок пока нет

- Matrix Tutorial 3Документ118 страницMatrix Tutorial 3kaiser tsarОценок пока нет

- Chapter 0 - Miscellaneous Preliminaries: EE 520: Topics - Compressed Sensing Linear Algebra ReviewДокумент18 страницChapter 0 - Miscellaneous Preliminaries: EE 520: Topics - Compressed Sensing Linear Algebra ReviewmohanОценок пока нет

- Mathematics Matrices: Vibrant AcademyДокумент26 страницMathematics Matrices: Vibrant AcademyIndranilОценок пока нет

- Bcom III Semester: Basic Numerical MethodsДокумент21 страницаBcom III Semester: Basic Numerical MethodsJaya Prakash100% (1)