Вам также может понравиться

- Table 17: Factors Wise Classification From Respondents: (AverageДокумент4 страницыTable 17: Factors Wise Classification From Respondents: (AveragemgajenОценок пока нет

- Product Specification: AUO Confidential For STAR Internal Use Only On 2014/04/15Документ32 страницыProduct Specification: AUO Confidential For STAR Internal Use Only On 2014/04/15Yunianto ObloОценок пока нет

- Detailed Advt CWE Clerks VДокумент33 страницыDetailed Advt CWE Clerks VRahul SoniОценок пока нет

- Abhishek Car LoanДокумент3 страницыAbhishek Car LoanmgajenОценок пока нет

- S VikyДокумент4 страницыS VikymgajenОценок пока нет

- Product Specification: AUO Confidential For STAR Internal Use Only On 2014/04/15Документ32 страницыProduct Specification: AUO Confidential For STAR Internal Use Only On 2014/04/15Yunianto ObloОценок пока нет

- Summary, Findings and ConclusionДокумент10 страницSummary, Findings and ConclusionmgajenОценок пока нет

- 1.3 Company ProfileДокумент10 страниц1.3 Company ProfilemgajenОценок пока нет

- 1.1 Industry ProfileДокумент9 страниц1.1 Industry ProfilemgajenОценок пока нет

- Research MethodologyДокумент14 страницResearch MethodologymgajenОценок пока нет

- 2.5 Review of LiteratureДокумент4 страницы2.5 Review of LiteraturemgajenОценок пока нет

- During The Year 2014 Due To Power Fluctuation The Unit Could Not Supply Goods in Time To TTK Prestige Who Are One of The Major Customers of This UnitДокумент1 страницаDuring The Year 2014 Due To Power Fluctuation The Unit Could Not Supply Goods in Time To TTK Prestige Who Are One of The Major Customers of This UnitmgajenОценок пока нет

- Findings: Age Wise ClassificationДокумент3 страницыFindings: Age Wise ClassificationmgajenОценок пока нет

- Findings of Leverages and Cost SheetДокумент3 страницыFindings of Leverages and Cost SheetmgajenОценок пока нет

- 5.introduction Credit Appraisal 15Документ17 страниц5.introduction Credit Appraisal 15mgajenОценок пока нет

- Full ProjectДокумент92 страницыFull ProjectmgajenОценок пока нет

- 1.01 List of Tables and ChartsДокумент4 страницы1.01 List of Tables and ChartsmgajenОценок пока нет

- Abhinav: International Monthly Refereed Journal of Research in Management & TechnologyДокумент6 страницAbhinav: International Monthly Refereed Journal of Research in Management & TechnologymgajenОценок пока нет

- 2015 2016Документ1 страница2015 2016mgajenОценок пока нет

- Objectives of The Study Primary ObjectiveДокумент1 страницаObjectives of The Study Primary ObjectivemgajenОценок пока нет

- Objectives of The Study Primary ObjectiveДокумент1 страницаObjectives of The Study Primary ObjectivemgajenОценок пока нет

- Credit Appraisal IntroductionДокумент17 страницCredit Appraisal IntroductionmgajenОценок пока нет

- Inventory To Current Asset RatioДокумент6 страницInventory To Current Asset RatiomgajenОценок пока нет

- 2.2 Needs, 2.3 Scope and 2.4 Limitations of The StudyДокумент1 страница2.2 Needs, 2.3 Scope and 2.4 Limitations of The StudymgajenОценок пока нет

- 13.data Analysis & InterpretationДокумент49 страниц13.data Analysis & InterpretationmgajenОценок пока нет

- Ratio Formula RemarksДокумент7 страницRatio Formula RemarksmgajenОценок пока нет

- During The Year 2014 Due To Power Fluctuation The Unit Could Not Supply Goods in Time To TTK Prestige Who Are One of The Major Customers of This UnitДокумент1 страницаDuring The Year 2014 Due To Power Fluctuation The Unit Could Not Supply Goods in Time To TTK Prestige Who Are One of The Major Customers of This UnitmgajenОценок пока нет

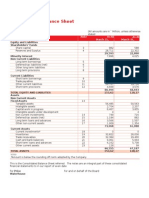

- Consolidated Balance Sheet: Annual Report 2013 - 2014Документ2 страницыConsolidated Balance Sheet: Annual Report 2013 - 2014mgajenОценок пока нет

- Credit Appraisal IntroductionДокумент17 страницCredit Appraisal IntroductionmgajenОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (120)

- Wisdom ReportДокумент58 страницWisdom ReportBRIAN NCUBEОценок пока нет

- Ebb Midterm PaperДокумент14 страницEbb Midterm PaperPutry LedoОценок пока нет

- AES CS Virtual Internship ProjectДокумент22 страницыAES CS Virtual Internship ProjectAjay0% (1)

- BSP Circular 425Документ3 страницыBSP Circular 425G Ant Mgd100% (1)

- Entrepreneurship... Chapter 6Документ17 страницEntrepreneurship... Chapter 6Zohaib XaibОценок пока нет

- Beat The Streets Investment Banking Interview Practice Guide PDFДокумент182 страницыBeat The Streets Investment Banking Interview Practice Guide PDFRushil Surapaneni100% (1)

- Impact of Monetary Policy On Interest RateДокумент97 страницImpact of Monetary Policy On Interest Raterajib1chowdhury1mushОценок пока нет

- Business and Competitive Analysis of RMG Industry of BangladeshДокумент41 страницаBusiness and Competitive Analysis of RMG Industry of Bangladeshsoul1971Оценок пока нет

- Civil Accounts Manual: SL No. Points Key PointsДокумент17 страницCivil Accounts Manual: SL No. Points Key PointsMooni Naik Meeravath100% (1)

- Thackwell v. BarclaysДокумент12 страницThackwell v. BarclaysJayant SinghОценок пока нет

- RHB Company ProfileДокумент5 страницRHB Company ProfileKhaleel Khusairi100% (1)

- The Stony Brook Press - Volume 30, Issue 10Документ32 страницыThe Stony Brook Press - Volume 30, Issue 10The Stony Brook PressОценок пока нет

- Axis - Microfinance Industry - Sector Report - Bandhan Bank and CreditAccess Grameen - 04-03-2021Документ40 страницAxis - Microfinance Industry - Sector Report - Bandhan Bank and CreditAccess Grameen - 04-03-2021anil1820Оценок пока нет

- PDFДокумент2 страницыPDFSunil RameshОценок пока нет

- Banking System A Database Project ReportДокумент31 страницаBanking System A Database Project Reportstrmohan85% (34)

- Banking Sector Yes Bank Under A Moratorium. SBI Investing CapitalДокумент5 страницBanking Sector Yes Bank Under A Moratorium. SBI Investing CapitalSingh JagdishОценок пока нет

- Project On Fund Based LoansДокумент18 страницProject On Fund Based LoansABHISHEK DAMОценок пока нет

- Case# Bandhan (A) : Advancing Financial Inclusion in IndiaДокумент3 страницыCase# Bandhan (A) : Advancing Financial Inclusion in IndiaLavanya KashyapОценок пока нет

- Math 11-ABM Business Math-Q2-Week-1Документ16 страницMath 11-ABM Business Math-Q2-Week-1Flordilyn DichonОценок пока нет

- Myanmar's Financial Sector A Challenging Environment For Banks ( (3 RD Edition, 2016)Документ96 страницMyanmar's Financial Sector A Challenging Environment For Banks ( (3 RD Edition, 2016)THAN HANОценок пока нет

- FAQ Cleared DateДокумент9 страницFAQ Cleared DateMadhurima ChatterjeeОценок пока нет

- Project Management of World Bank ProjectsДокумент25 страницProject Management of World Bank ProjectsDenisa PopescuОценок пока нет

- Nmims Mba Distance DetailsДокумент9 страницNmims Mba Distance DetailsGanapathy VigneshОценок пока нет

- MBA IB - International Business Laws Notes & Ebook - Second Year Sem 3 - Free PDF Download PDFДокумент319 страницMBA IB - International Business Laws Notes & Ebook - Second Year Sem 3 - Free PDF Download PDFrohanОценок пока нет

- The Extent To Which The Organization Is Realizing Its Visions and Missions and Performance of The Organization in Relation To Its ObjectivesДокумент3 страницыThe Extent To Which The Organization Is Realizing Its Visions and Missions and Performance of The Organization in Relation To Its ObjectivesZelalem AnimutОценок пока нет

- Auditing Problems TheoryДокумент40 страницAuditing Problems TheoryRod Lester de Guzman100% (2)

- RFBT - Chapter 5 - Philippine Deposit Insurance CorporationДокумент6 страницRFBT - Chapter 5 - Philippine Deposit Insurance Corporationlaythejoylunas21Оценок пока нет

- Accounting and Reporting Practice of Micro and Small Enterprises in West Oromia Region, EthiopiaДокумент8 страницAccounting and Reporting Practice of Micro and Small Enterprises in West Oromia Region, Ethiopiagezahagn EyobОценок пока нет

- SOC Islamic July Dec 2021 1Документ57 страницSOC Islamic July Dec 2021 1ZohaibОценок пока нет

- Reading 1 2223-Kids and MoneyДокумент2 страницыReading 1 2223-Kids and MoneyVíctor Barbosa LosadaОценок пока нет