Вам также может понравиться

- W8 BEN FormДокумент2 страницыW8 BEN FormJay100% (2)

- 609b7c0 1655smartДокумент1 страница609b7c0 1655smartram janeОценок пока нет

- Invoice OD40426072810Документ2 страницыInvoice OD40426072810war10ckjupiОценок пока нет

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Документ1 страницаTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Nitin KumarОценок пока нет

- Mega Sales Sale - Cr1186Документ6 страницMega Sales Sale - Cr1186Spitfire llОценок пока нет

- Customer Name Delhivery GSTДокумент4 страницыCustomer Name Delhivery GSTSai Kruthik ReddyОценок пока нет

- InvoiceДокумент1 страницаInvoiceKuldeep Krishan Trivedi Sr.Оценок пока нет

- Birch Paper Company FinalllllДокумент11 страницBirch Paper Company FinalllllMadhuri Sangare100% (1)

- (Test Bank) Chapter 3Документ41 страница(Test Bank) Chapter 3Kiara Mas100% (2)

- Aspl Invoice 2019-20 Jan'20 To Mar'20Документ20 страницAspl Invoice 2019-20 Jan'20 To Mar'20Gurupada SahooОценок пока нет

- Postpaid Bill 9855810088 927643165Документ7 страницPostpaid Bill 9855810088 927643165Atul SaralachОценок пока нет

- Patra Electronics: ® ga#E®R®#8Документ1 страницаPatra Electronics: ® ga#E®R®#8Vikrant DeshmukhОценок пока нет

- Ugvcl Godrej AUG 2017Документ1 страницаUgvcl Godrej AUG 2017jha.sofcon5941Оценок пока нет

- Iltil - Il Il - Rillil LL Illflll Llil Il Ffil LTR Il LilДокумент1 страницаIltil - Il Il - Rillil LL Illflll Llil Il Ffil LTR Il LilJay SriramОценок пока нет

- MCD OperationsДокумент16 страницMCD OperationsAnkit DubeyОценок пока нет

- Introduction To Project ManagementДокумент41 страницаIntroduction To Project ManagementSheikh Muneeb Ul HaqОценок пока нет

- HSBCДокумент91 страницаHSBCSufyan Safwan SulaimanОценок пока нет

- Hytorc Gas 25533 8-28-18Документ1 страницаHytorc Gas 25533 8-28-18Jenny RobertsonОценок пока нет

- BillДокумент2 страницыBillBilal SalimОценок пока нет

- Retail Invoice: Other Details of SupplierДокумент1 страницаRetail Invoice: Other Details of SupplierPubali Deb BurmanОценок пока нет

- Postpaid Bill 7710074295 DECДокумент3 страницыPostpaid Bill 7710074295 DEConkarОценок пока нет

- Complete Mobile Protection 1 Year by Flipkart Protect: Grand Total 299.00Документ1 страницаComplete Mobile Protection 1 Year by Flipkart Protect: Grand Total 299.00mahisoft225Оценок пока нет

- PassbookДокумент1 страницаPassbookAnonymous OodVBivОценок пока нет

- InvoiceДокумент1 страницаInvoiceSUNIL PATELОценок пока нет

- Water Bill June 2019Документ1 страницаWater Bill June 2019Sathish A AvnОценок пока нет

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Документ1 страницаTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Sumit VyasОценок пока нет

- Invoice PDFДокумент1 страницаInvoice PDFAYUSH VERMAОценок пока нет

- AMAN BILL & Invoice FormatДокумент27 страницAMAN BILL & Invoice FormatManpreet SachdevaОценок пока нет

- Gani Dental Lab: Qty DescriptionДокумент1 страницаGani Dental Lab: Qty DescriptionSridharanGuruSenthОценок пока нет

- CSC Online Registration Process - CompressedДокумент9 страницCSC Online Registration Process - CompressedMedagam VenkateswarareddyОценок пока нет

- Invoice 3Документ1 страницаInvoice 3Ranveer Singh SajwanОценок пока нет

- Water Bill June19 MidcДокумент1 страницаWater Bill June19 MidcManoj SahuОценок пока нет

- 10%approval Hospital Claims-March2013Документ52 страницы10%approval Hospital Claims-March2013abdulkhaderjeelani14Оценок пока нет

- Policy ScheduleДокумент4 страницыPolicy ScheduleacrajeshОценок пока нет

- Delivery Summary: Order DateДокумент4 страницыDelivery Summary: Order Datemahi vaniОценок пока нет

- PI - Urbanscape PDFДокумент1 страницаPI - Urbanscape PDFSanrachna ConsultantsОценок пока нет

- Sub Order LabelsДокумент163 страницыSub Order LabelsHitzz LalwaniОценок пока нет

- SIPB Stage-1 Check List For Incentives Under Bihar Industrial Investment Promotion Policy, 2016Документ1 страницаSIPB Stage-1 Check List For Incentives Under Bihar Industrial Investment Promotion Policy, 2016SAMRAT SILОценок пока нет

- Name of The Company (In Full) :: Contractor / Vendor Registration FormДокумент14 страницName of The Company (In Full) :: Contractor / Vendor Registration FormSantosh ThakurОценок пока нет

- ACT InvoiceДокумент2 страницыACT InvoiceRaghavendra RaoОценок пока нет

- Delivery Acknowledgement NoteДокумент1 страницаDelivery Acknowledgement NoteManvi PareekОценок пока нет

- Broadband Bill JuneДокумент1 страницаBroadband Bill JunekarthikОценок пока нет

- Hul FravДокумент8 страницHul FravAnmol YadavОценок пока нет

- Srinivas InvoiceДокумент1 страницаSrinivas InvoiceKanchanapalli SrinivasОценок пока нет

- Cost Estimate: Datum TechnologiesДокумент1 страницаCost Estimate: Datum Technologiesraj rajОценок пока нет

- Invoice Trolley SnapdealДокумент3 страницыInvoice Trolley SnapdealPrashant AdhikariОценок пока нет

- Sales 32 2023 24Документ1 страницаSales 32 2023 24Bharat AutomobileОценок пока нет

- Mobile Services: Your Account Summary This Month'S ChargesДокумент8 страницMobile Services: Your Account Summary This Month'S ChargesVenkatram PailaОценок пока нет

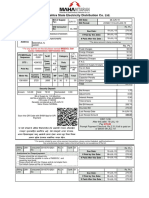

- Maharashtra State Electricity Distribution Co. LTD.: For Any Queries On This Bill Please Contact MSEDCL CallДокумент1 страницаMaharashtra State Electricity Distribution Co. LTD.: For Any Queries On This Bill Please Contact MSEDCL CallAkash PatilОценок пока нет

- Rahul Kumar: Flat No.202, Whit Building, Front of OYO Tower, Bachute Patil Nagar, Marunji, Pune Maharashtra - 27Документ1 страницаRahul Kumar: Flat No.202, Whit Building, Front of OYO Tower, Bachute Patil Nagar, Marunji, Pune Maharashtra - 27RAHULsprlОценок пока нет

- Upes Fee Invoice PDFДокумент1 страницаUpes Fee Invoice PDFJai SingalОценок пока нет

- Mobile Services: Your Account Summary This Month'S ChargesДокумент3 страницыMobile Services: Your Account Summary This Month'S Chargeskumarvaibhav301745Оценок пока нет

- Receipt: GTPL Broadband Pvt. LTDДокумент1 страницаReceipt: GTPL Broadband Pvt. LTDketan patelОценок пока нет

- Beam April 2018 PDFДокумент2 страницыBeam April 2018 PDFShyam BhaskaranОценок пока нет

- Retail Invoice / Bill: Your Total Savings: Rs.23.39Документ1 страницаRetail Invoice / Bill: Your Total Savings: Rs.23.39Praveen KumarОценок пока нет

- GST Invoice FormatДокумент1 страницаGST Invoice FormatMaulin Patel100% (1)

- Ishan Netsol Private Limited: Tax InvoiceДокумент2 страницыIshan Netsol Private Limited: Tax InvoiceSunil Patel100% (1)

- Tax Invoice: Excitel Broadband Pvt. LTDДокумент1 страницаTax Invoice: Excitel Broadband Pvt. LTDMittal Galaxy100% (1)

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Документ2 страницыTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Devan ShahОценок пока нет

- View-Bill Dhaliywas PDFДокумент1 страницаView-Bill Dhaliywas PDFGourav RaoОценок пока нет

- Hospital Invoice TemplateДокумент1 страницаHospital Invoice TemplateAakash HoskotiОценок пока нет

- Bill of Supply For Electricity Due Date: - : BSES Yamuna Power LTDДокумент1 страницаBill of Supply For Electricity Due Date: - : BSES Yamuna Power LTDShrishti NegiОценок пока нет

- 181320250 (2)Документ1 страница181320250 (2)Maharshi DattaОценок пока нет

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Документ1 страницаTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)diruОценок пока нет

- Proforma Invoice - Volvo TrucksДокумент1 страницаProforma Invoice - Volvo TrucksRaviTeja KvsnОценок пока нет

- MFL Q3 FY2015 Financial ResultsДокумент2 страницыMFL Q3 FY2015 Financial ResultsAnkit DubeyОценок пока нет

- BPR Bank FinalДокумент22 страницыBPR Bank FinalAnkit DubeyОценок пока нет

- Behaviour in OrganisationДокумент9 страницBehaviour in OrganisationRasesh ShahОценок пока нет

- Budgeting and PlanningДокумент53 страницыBudgeting and PlanningAnkit DubeyОценок пока нет

- Associate Consultant / Consultant-Performance Improvement - IT Advisory ServicesДокумент2 страницыAssociate Consultant / Consultant-Performance Improvement - IT Advisory ServicesAnkit DubeyОценок пока нет

- 40 Paarul Vora Adlabs ImagicaДокумент10 страниц40 Paarul Vora Adlabs ImagicaAnkit DubeyОценок пока нет

- EditorialДокумент2 страницыEditorialAnkit DubeyОценок пока нет

- Contingency PathgoaltheoriesДокумент20 страницContingency PathgoaltheorieslengocthangОценок пока нет

- Forex Daily Report: Fundamentals EURUSD Sep'13Документ3 страницыForex Daily Report: Fundamentals EURUSD Sep'13Ankit DubeyОценок пока нет

- TARGET 2015 - All India General Studies Mains Test Series 2015 - 22 Mock Tests - English Medium + Current Affairs Notes - Module 17 JanДокумент14 страницTARGET 2015 - All India General Studies Mains Test Series 2015 - 22 Mock Tests - English Medium + Current Affairs Notes - Module 17 JanAnkit DubeyОценок пока нет

- Concept and Measurement of Human DevelopmentДокумент58 страницConcept and Measurement of Human DevelopmentAnkit DubeyОценок пока нет

- InsightsonIndia Test Series Paper 1Документ27 страницInsightsonIndia Test Series Paper 1fafduplessiОценок пока нет

- Sept Week 11Документ40 страницSept Week 11Ankit DubeyОценок пока нет

- 560265592PC - IT Sector Update - Oct 2014 20141031143535Документ6 страниц560265592PC - IT Sector Update - Oct 2014 20141031143535Ankit DubeyОценок пока нет

- 1796823687PC - State Bank Q2FY15 - Nov 2014 20141114220543Документ8 страниц1796823687PC - State Bank Q2FY15 - Nov 2014 20141114220543Ankit DubeyОценок пока нет

- Banking Reform in IndiaДокумент57 страницBanking Reform in IndiaManushi ShahОценок пока нет

- SIMSR Value Stock DriversДокумент7 страницSIMSR Value Stock DriversAnkit DubeyОценок пока нет

- Sudhir Anand and Amartya SenДокумент34 страницыSudhir Anand and Amartya SenAnkur SinghОценок пока нет

- Class Notes CH21Документ17 страницClass Notes CH21KamauWafulaWanyamaОценок пока нет

- Saunders & Cornnet Solution Chapter 1 Part 1Документ5 страницSaunders & Cornnet Solution Chapter 1 Part 1Mo AlamОценок пока нет

- The Macroeconomic Impact of Remittances in The PhilippinesДокумент46 страницThe Macroeconomic Impact of Remittances in The PhilippinesBrian Jason PonceОценок пока нет

- Getting Funding or Financing: Bruce R. Barringer R. Duane IrelandДокумент47 страницGetting Funding or Financing: Bruce R. Barringer R. Duane IrelandSuplex CityОценок пока нет

- Bombay DyeingДокумент17 страницBombay Dyeingparas_bhatnagar89Оценок пока нет

- Business English WordsДокумент10 страницBusiness English WordsAnna EgriОценок пока нет

- Accounting Framework and ConceptsДокумент30 страницAccounting Framework and Conceptsyow jing peiОценок пока нет

- Presentation On Topic: HDFC Bank AND Models of ManagementДокумент42 страницыPresentation On Topic: HDFC Bank AND Models of Managementsonu238909Оценок пока нет

- 09Документ8 страниц09asnairahОценок пока нет

- Chapte R: Principles of Working Capital ManagementДокумент24 страницыChapte R: Principles of Working Capital Managementmylyf12Оценок пока нет

- New Horizon Business Proposal FinalДокумент20 страницNew Horizon Business Proposal FinalCHARRYSAH TABAOSARESОценок пока нет

- 2018 DP World Annual Report EnglishДокумент77 страниц2018 DP World Annual Report EnglishGabriel CaraveteanuОценок пока нет

- Establishing The Effectiveness of Market Ratios in Predicting Financial Distress of Listed Firms in Nairobi Security Exchange MarketДокумент13 страницEstablishing The Effectiveness of Market Ratios in Predicting Financial Distress of Listed Firms in Nairobi Security Exchange MarketOIRCОценок пока нет

- Ifrs 7 DeloitteДокумент14 страницIfrs 7 DeloitteMystic Male0% (1)

- Issue 95Документ32 страницыIssue 95NZ Tasveer NewsОценок пока нет

- Market Entry strategy-WORDДокумент3 страницыMarket Entry strategy-WORDAparna TiwariОценок пока нет

- IAS#16Документ17 страницIAS#16Shah KamalОценок пока нет

- PDFДокумент19 страницPDFVINOD MEHTAОценок пока нет

- Corporate BankingДокумент100 страницCorporate Bankingvinesh1515100% (3)

- Mplus FormДокумент4 страницыMplus Formmohd fairusОценок пока нет

- Failed Work Needs ResitДокумент15 страницFailed Work Needs ResitrashidaОценок пока нет

- An Empirical Examination of The Amortized Spread: John M.R. Chalmers !, Gregory B. Kadlec"Документ30 страницAn Empirical Examination of The Amortized Spread: John M.R. Chalmers !, Gregory B. Kadlec"tsas9508Оценок пока нет

- Project Content NewДокумент87 страницProject Content NewSintoj Thomas100% (1)