Вам также может понравиться

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Bush 1992 Executive Order 12803 - Infrastructure Privatization PDFДокумент2 страницыBush 1992 Executive Order 12803 - Infrastructure Privatization PDFmichaelonlineОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- How To Amend Articles of Incorporation and byДокумент3 страницыHow To Amend Articles of Incorporation and byHARLEY TANОценок пока нет

- Outline of RA 9646 (RESA)Документ3 страницыOutline of RA 9646 (RESA)MichelleOgatisОценок пока нет

- Banking Law SyllabusДокумент8 страницBanking Law SyllabusAnonymous wdCD7FeW9XОценок пока нет

- Subido V SandiganbayanДокумент3 страницыSubido V SandiganbayanBlake Sy100% (1)

- SEC vs. Universal RightfieldДокумент3 страницыSEC vs. Universal RightfieldCaitlin KintanarОценок пока нет

- Nirc (Codal)Документ247 страницNirc (Codal)Jierah Manahan0% (1)

- Imperial vs. ArmesДокумент17 страницImperial vs. ArmesWorstWitch Tala0% (1)

- 2014-2018 Bar Examinations Questions in MERCANTILE LAWДокумент30 страниц2014-2018 Bar Examinations Questions in MERCANTILE LAWdetteheartsОценок пока нет

- General Information Sheet (Gis) : Non-Stock Corporation FOR THE YEAR - 2020Документ6 страницGeneral Information Sheet (Gis) : Non-Stock Corporation FOR THE YEAR - 2020Rafael ObusanОценок пока нет

- Tiger TeamДокумент14 страницTiger TeammlefcowitzОценок пока нет

- 753 Ground SupplyДокумент53 страницы753 Ground SupplyFernando RosalesОценок пока нет

- Gabionsa v. CAДокумент11 страницGabionsa v. CADennis VelasquezОценок пока нет

- 19padilla v. Dizon, 158 SCRA 127 (1988)Документ2 страницы19padilla v. Dizon, 158 SCRA 127 (1988)Princess Marie FragoОценок пока нет

- Tzero LawsuitДокумент61 страницаTzero LawsuitAnonymous RXEhFb50% (2)

- $) Upreme: 31/epublic of Tbe, LbbtlipptnesДокумент13 страниц$) Upreme: 31/epublic of Tbe, LbbtlipptnesJesryl 8point8 TeamОценок пока нет

- Code of NursingДокумент9 страницCode of NursingRowena TorricoОценок пока нет

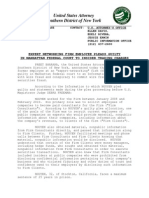

- U.S. Attorney's Statement On Bob Nguyen's Guilty PleaДокумент2 страницыU.S. Attorney's Statement On Bob Nguyen's Guilty PleaDealBookОценок пока нет

- Tabuzo V GomozДокумент8 страницTabuzo V GomozViner Hernan SantosОценок пока нет

- JR, Whereby The Court Therein Ordered Respondent To Be Dismissed From The JudiciaryДокумент36 страницJR, Whereby The Court Therein Ordered Respondent To Be Dismissed From The JudiciaryJimi SolomonОценок пока нет

- Guidance On The 2010 ADA Standards For Accessible Design Volume 2Документ93 страницыGuidance On The 2010 ADA Standards For Accessible Design Volume 2Eproy 3DОценок пока нет

- Remedies of The TaxpayerДокумент16 страницRemedies of The TaxpayerCristelle Elaine Collera100% (1)

- Motion To Dismiss SEC Civil Action Against Texas AG Ken PaxtonДокумент32 страницыMotion To Dismiss SEC Civil Action Against Texas AG Ken Paxtonlanashadwick0% (1)

- Online Gambling Company Fights Iroquois' War of Words - Growth Capitalist 6.11.2014Документ4 страницыOnline Gambling Company Fights Iroquois' War of Words - Growth Capitalist 6.11.2014Teri BuhlОценок пока нет

- Admin Law Cases No. 3Документ11 страницAdmin Law Cases No. 3abbyhwaitingОценок пока нет

- Labor Standards Course Outline Complete)Документ29 страницLabor Standards Course Outline Complete)Rodel del MundoОценок пока нет

- Firm 116797Документ177 страницFirm 116797Federico GennariОценок пока нет

- LOPO - AppointmentДокумент61 страницаLOPO - AppointmentCGОценок пока нет

- Republic of The Philippines - Energy Regulatory CommissionДокумент11 страницRepublic of The Philippines - Energy Regulatory CommissionKhenan James NarismaОценок пока нет

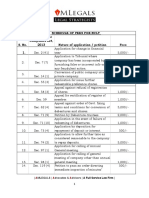

- Schedule of Fees in NCLT 1Документ4 страницыSchedule of Fees in NCLT 1Lavkesh BhambhaniОценок пока нет