Вам также может понравиться

- AfterLife ServicesДокумент21 страницаAfterLife ServicesJoydeep SilОценок пока нет

- De La Salle University Medical Center (Dlsumc) : Hospital AdministrationДокумент1 страницаDe La Salle University Medical Center (Dlsumc) : Hospital AdministrationFerl ElardoОценок пока нет

- Microsoft Word - Health Literacy AbstractДокумент1 страницаMicrosoft Word - Health Literacy AbstractPhilip GirvanОценок пока нет

- Marketing Plan DraftДокумент18 страницMarketing Plan DraftTreachy Rose GeneblazaОценок пока нет

- Swot AnalysisДокумент7 страницSwot AnalysisAlianna Irish ContrerasОценок пока нет

- Funeral Plans Case StudyДокумент5 страницFuneral Plans Case StudyAna Pintac0% (1)

- What Are The Challenges Faced by Small Business Owners in This Era of GlobalizationДокумент53 страницыWhat Are The Challenges Faced by Small Business Owners in This Era of GlobalizationGabreyille Nuya100% (1)

- PRECIS 6 - The Consumer Decision JourneyДокумент2 страницыPRECIS 6 - The Consumer Decision JourneyjeffscribdОценок пока нет

- GROUP 3 - Europe BookДокумент8 страницGROUP 3 - Europe BookIrish June TayagОценок пока нет

- Entrepreneurial Marketing (Aes 51003) : Prepared For: Prof Madya Noor Hasmini Binti Abd GhaniДокумент8 страницEntrepreneurial Marketing (Aes 51003) : Prepared For: Prof Madya Noor Hasmini Binti Abd GhaniMuhammad Qasim A20D047FОценок пока нет

- Chinese Numbers To One BillionДокумент10 страницChinese Numbers To One Billionkoray sairОценок пока нет

- 4 PsДокумент4 страницы4 PsYoga ChanОценок пока нет

- Thesis Proposal PDFДокумент13 страницThesis Proposal PDFHimale AhammedОценок пока нет

- Essay On The Parable of The SadhuДокумент3 страницыEssay On The Parable of The SadhumattОценок пока нет

- Impact of Small and Medium Enterprises On Economic Growth and DevelopmentДокумент5 страницImpact of Small and Medium Enterprises On Economic Growth and DevelopmentBabak HedayatiОценок пока нет

- Ethics Challenge 1 - 47Документ58 страницEthics Challenge 1 - 47Sam SelinОценок пока нет

- II. Brief History of The CompanyДокумент5 страницII. Brief History of The CompanyJohn Patrick ReynosОценок пока нет

- Nike Internal External Assessment 1218783971527971 8Документ26 страницNike Internal External Assessment 1218783971527971 8Shahaen Baloch100% (1)

- International Business Strategy NotesДокумент68 страницInternational Business Strategy NotesAlexandra LífОценок пока нет

- A Conceptual Model of Corporate Moral DevelopmentДокумент12 страницA Conceptual Model of Corporate Moral DevelopmentmirianalbertpiresОценок пока нет

- Case Study - PNOC EDC (Critique) (Group 5)Документ6 страницCase Study - PNOC EDC (Critique) (Group 5)Anonymous bV4OSIОценок пока нет

- UCP AssignmentДокумент16 страницUCP AssignmentSaniya SaddiqiОценок пока нет

- Managerial 1Документ88 страницManagerial 1Mary Kris CaparosoОценок пока нет

- Solved Forecasting The Success of New Product Introductions Is Notoriously DifficultДокумент1 страницаSolved Forecasting The Success of New Product Introductions Is Notoriously DifficultM Bilal SaleemОценок пока нет

- NHSL Mortuary ServicesДокумент7 страницNHSL Mortuary ServicesPamila AdikariОценок пока нет

- Youth Employment and Employability in MalaysiaДокумент15 страницYouth Employment and Employability in MalaysiaAbe Alias Syed HamidОценок пока нет

- Essay ActivitiesДокумент17 страницEssay ActivitiesAngelyn LingatongОценок пока нет

- Julia Anggraini 17018082 - Thesis ProposalДокумент38 страницJulia Anggraini 17018082 - Thesis ProposalJuliia AnggraiiniiОценок пока нет

- Brooklyn BreweryДокумент11 страницBrooklyn BreweryHammad GillaniОценок пока нет

- Mexico Case StudyДокумент3 страницыMexico Case StudyWalaa Alzoubi100% (1)

- Tariffied Case AnalysisДокумент2 страницыTariffied Case AnalysisParmeetОценок пока нет

- Business Strategy 1st MidTerm UniboДокумент55 страницBusiness Strategy 1st MidTerm Unibogeorge_natОценок пока нет

- Asirius Philippines Inc.Документ96 страницAsirius Philippines Inc.Lee SuarezОценок пока нет

- STRAMAДокумент7 страницSTRAMACheryl Arcega PangdaОценок пока нет

- International Production TheoriesДокумент72 страницыInternational Production TheoriesBrandonMoothooОценок пока нет

- Monetary EconomicsДокумент26 страницMonetary EconomicsNidhi AroraОценок пока нет

- CEMEX Case StudyДокумент2 страницыCEMEX Case Studyshamina kОценок пока нет

- Dairy SolutioNZ English 19-7-10Документ16 страницDairy SolutioNZ English 19-7-10Priyanka SinghОценок пока нет

- Manila Bulletin Publishing Corporation-ManualДокумент13 страницManila Bulletin Publishing Corporation-ManualMoises CalastravoОценок пока нет

- Impact of Globalization On JamaicaДокумент2 страницыImpact of Globalization On JamaicaAaliyah Mohamed100% (1)

- Reducing Employee Turnover in Small BusinessДокумент6 страницReducing Employee Turnover in Small BusinessManpreet Kaur VirkОценок пока нет

- Case Study - Coca Cola and Nike.Документ3 страницыCase Study - Coca Cola and Nike.Jayanth ReddyОценок пока нет

- Pest AnalysisДокумент2 страницыPest AnalysisRupesh LimbaniОценок пока нет

- The Blue Ocean StrategyДокумент8 страницThe Blue Ocean StrategybrendaОценок пока нет

- Evolution, Basics and Importance of Knowledge ManagementДокумент10 страницEvolution, Basics and Importance of Knowledge ManagementDeepti RajОценок пока нет

- Reaction Paper EntrepДокумент1 страницаReaction Paper EntrepClaire MacaraegОценок пока нет

- JIT and LEANДокумент2 страницыJIT and LEANNaCho5 PrettyОценок пока нет

- Strategy AllaincesДокумент40 страницStrategy AllaincesSarin John SkariaОценок пока нет

- Porters Five Forces AnalaysisДокумент2 страницыPorters Five Forces AnalaysisMd. Sabbir Sarker 1611386630Оценок пока нет

- Closing Case: Coca-ColaДокумент2 страницыClosing Case: Coca-ColaLina M. Pajaro EllesОценок пока нет

- Assignment Operations Management Hazel LawnДокумент9 страницAssignment Operations Management Hazel Lawnthắng trần văn100% (1)

- Case Study SWOT PDFДокумент8 страницCase Study SWOT PDFRoy John Sarmiento100% (1)

- 10 Step: Marketing Plan For MISSION Hospital and Ambulatory Surgery CenterДокумент23 страницы10 Step: Marketing Plan For MISSION Hospital and Ambulatory Surgery Centercadbury12345Оценок пока нет

- Case Analysis 1Документ4 страницыCase Analysis 1Angela TolentinoОценок пока нет

- 84 AcДокумент25 страниц84 AcHàQuốcMinhОценок пока нет

- Consumer BehaviorДокумент38 страницConsumer BehaviorAbhay100% (1)

- Thesis Good Final Copy2Документ171 страницаThesis Good Final Copy2Милица Д. СтошићОценок пока нет

- Foundation of Organization DevelopmentДокумент20 страницFoundation of Organization Developmentrohankshah1Оценок пока нет

- Convergent Thinking Vs Divergent by Chuck ClaytonДокумент4 страницыConvergent Thinking Vs Divergent by Chuck ClaytongmelindaОценок пока нет

- Conducting Market ResearchДокумент37 страницConducting Market ResearchArnold Cavalida BucoyОценок пока нет

- Group 5 BLUE ClothingДокумент10 страницGroup 5 BLUE ClothingAntony Varghese PalamuttamОценок пока нет

- Group 4 BLUE Jet EnginesДокумент7 страницGroup 4 BLUE Jet EnginesAntony Varghese PalamuttamОценок пока нет

- Macroeconomic Analysis Wine IndustryДокумент8 страницMacroeconomic Analysis Wine IndustryAntony Varghese Palamuttam100% (1)

- Group 1 BLUE Canadian TelevisionДокумент6 страницGroup 1 BLUE Canadian TelevisionAntony Varghese PalamuttamОценок пока нет

- Group 6 BLUE Pharmaceuticals DiabetesДокумент8 страницGroup 6 BLUE Pharmaceuticals DiabetesAntony Varghese PalamuttamОценок пока нет

- Macroeconomic Analysis Wine IndustryДокумент8 страницMacroeconomic Analysis Wine IndustryAntony Varghese Palamuttam100% (1)

- Impact of Political Instability On Economic GrowthДокумент12 страницImpact of Political Instability On Economic GrowthAnas RizwanОценок пока нет

- From The Soviet Bloc To The European Union - Ivan T. BerendДокумент317 страницFrom The Soviet Bloc To The European Union - Ivan T. BerendLupuDanielОценок пока нет

- Sapna Hooda Thesis A Study of FDI and Indian EconomyДокумент153 страницыSapna Hooda Thesis A Study of FDI and Indian EconomyPranik123Оценок пока нет

- Bass Pro ShopДокумент30 страницBass Pro Shopapi-259569476Оценок пока нет

- Indian MSME SectorДокумент4 страницыIndian MSME SectorPranav MishraОценок пока нет

- Public Shariah MFR February 2018Документ42 страницыPublic Shariah MFR February 2018ieda1718Оценок пока нет

- Deagel 2025 Forecast ResurrectedДокумент7 страницDeagel 2025 Forecast ResurrectedCraig Stone100% (2)

- GDP, GNP and NI NotesДокумент5 страницGDP, GNP and NI NotesKhaleel KothdiwalaОценок пока нет

- The Problem of Digital Divide and Inequality in Big Data AnalysisДокумент11 страницThe Problem of Digital Divide and Inequality in Big Data AnalysisFrendi PascalisОценок пока нет

- Documented EssayДокумент3 страницыDocumented EssaybaldeОценок пока нет

- An Introduction To Doing Business in Indonesia 2023Документ76 страницAn Introduction To Doing Business in Indonesia 2023Eric FORTINОценок пока нет

- Vegas 2015Документ16 страницVegas 2015Rasha RabbaniОценок пока нет

- The Short-Term Fluctuations in Output, Employment, Financial Conditions, and Prices That We Call The Business CycleДокумент3 страницыThe Short-Term Fluctuations in Output, Employment, Financial Conditions, and Prices That We Call The Business CycleClevin CkОценок пока нет

- Assessing Social Sustainability PDFДокумент20 страницAssessing Social Sustainability PDFAnonymous vWcMCraH1OОценок пока нет

- Tourism Satellite Account 2022Документ6 страницTourism Satellite Account 2022Anonymous UpWci5Оценок пока нет

- My Mms ProjectДокумент115 страницMy Mms ProjectMichael NwogboОценок пока нет

- Practice Problems 8Документ2 страницыPractice Problems 8Kemi AwosanyaОценок пока нет

- 434311562motilal Oswal Passive Funds PitchBook 31 Jul 2020 - V2Документ95 страниц434311562motilal Oswal Passive Funds PitchBook 31 Jul 2020 - V2dabster7000Оценок пока нет

- Chapter 7 Fundamental Analysis - Economy AnalysisДокумент19 страницChapter 7 Fundamental Analysis - Economy AnalysisPraveshMalikОценок пока нет

- Eco 102 Review Questions 1Документ4 страницыEco 102 Review Questions 1Ahmed DahiОценок пока нет

- AML-2203 Advanced Python AI and ML Tools AssignmentДокумент19 страницAML-2203 Advanced Python AI and ML Tools AssignmentRohit NОценок пока нет

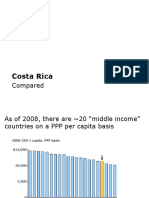

- Costa Rica AnalysisДокумент140 страницCosta Rica AnalysisAdrián GarcíaОценок пока нет

- DatabaseMarch2022 LifeДокумент266 страницDatabaseMarch2022 LifeZavršni radОценок пока нет

- RISC-RISEDoctoralPost-Doctoral School D TRAORE 10-09-21 FinalДокумент20 страницRISC-RISEDoctoralPost-Doctoral School D TRAORE 10-09-21 FinalJhera Mae CahoksonОценок пока нет

- Banc de Binary E-BookДокумент19 страницBanc de Binary E-BookBanc De Binary (BBinary)0% (1)

- South Africa 2000 enДокумент213 страницSouth Africa 2000 enYonnyОценок пока нет

- 54181CA Advertising Agencies in Canada Industry ReportДокумент52 страницы54181CA Advertising Agencies in Canada Industry ReportPaul BarbinОценок пока нет

- BBA 4 Year Curriculum 60 P PDFДокумент57 страницBBA 4 Year Curriculum 60 P PDFZohe Bohe100% (2)

- Regional Economic Impact of High-Speed Rail Development in People's Republic of ChinaДокумент33 страницыRegional Economic Impact of High-Speed Rail Development in People's Republic of ChinaADBI EventsОценок пока нет