Вам также может понравиться

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Chapter 6 - Process Capability AnalysisДокумент21 страницаChapter 6 - Process Capability AnalysisKaya Eralp AsanОценок пока нет

- Disc Brake System ReportДокумент20 страницDisc Brake System ReportGovindaram Rajesh100% (1)

- Therapeutic EffectsofWhole-BodyDevices Applying Pulsed Electromagnetic Fields (PEMF)Документ11 страницTherapeutic EffectsofWhole-BodyDevices Applying Pulsed Electromagnetic Fields (PEMF)Jeroan MonteiroОценок пока нет

- Same Virtus: Alarm ListДокумент23 страницыSame Virtus: Alarm ListLacatusu Mircea100% (1)

- Oracle Database 11g OverviewДокумент46 страницOracle Database 11g OverviewEddie Awad91% (11)

- NATCO Presentation - Desalters PDFДокумент12 страницNATCO Presentation - Desalters PDFshahmkamalОценок пока нет

- Theories of FX DeterminationДокумент52 страницыTheories of FX DeterminationJeisson OchoaОценок пока нет

- Derivatives in IndiaДокумент21 страницаDerivatives in IndiaShajupaulОценок пока нет

- in Our View,: Vrddhi Capital Investment AdvisorsДокумент5 страницin Our View,: Vrddhi Capital Investment AdvisorsMohit AgarwalОценок пока нет

- W 23784Документ31 страницаW 23784Elshen MennedovОценок пока нет

- "Planning Your Financial Future": Mangala Boyagoda 26 October 2010Документ71 страница"Planning Your Financial Future": Mangala Boyagoda 26 October 2010Inde Pendent LkОценок пока нет

- EPCA Seminar: Olefins Outlook: 9 October 2020Документ13 страницEPCA Seminar: Olefins Outlook: 9 October 2020Aswin KondapallyОценок пока нет

- Florida's April Employment Figures Released: Rick Scott Cynthia R. LorenzoДокумент16 страницFlorida's April Employment Figures Released: Rick Scott Cynthia R. LorenzoMichael AllenОценок пока нет

- FMG China Fund - PresentationДокумент15 страницFMG China Fund - PresentationSusan AllenОценок пока нет

- Florida's July Employment Figures Released: Charlie Crist Cynthia R. LorenzoДокумент16 страницFlorida's July Employment Figures Released: Charlie Crist Cynthia R. LorenzoMichael AllenОценок пока нет

- Philippine Rice Trade Liberalization: Impacts On Agriculture and The Economy, and Alternative Policy ActionsДокумент12 страницPhilippine Rice Trade Liberalization: Impacts On Agriculture and The Economy, and Alternative Policy ActionsJofred Dela VegaОценок пока нет

- J.C. Parets, CMTДокумент25 страницJ.C. Parets, CMTPunit TewaniОценок пока нет

- November 2008 Update: Why Are Electricity Prices in RTOs Increasingly Expensive?Документ8 страницNovember 2008 Update: Why Are Electricity Prices in RTOs Increasingly Expensive?RobertMcCulloughОценок пока нет

- Florida's October Employment Figures Released: TallahasseeДокумент16 страницFlorida's October Employment Figures Released: TallahasseeMichael AllenОценок пока нет

- Florida's November Employment Figures ReleasedДокумент16 страницFlorida's November Employment Figures ReleasedMichael AllenОценок пока нет

- CME - Comparing E-Minis and ETFs - Sep2012 PDFДокумент8 страницCME - Comparing E-Minis and ETFs - Sep2012 PDFbearsqОценок пока нет

- TALLAHASSEE - Florida's Seasonally Adjusted Unemployment Rate in January 2011 Is 11.9 PercentДокумент16 страницTALLAHASSEE - Florida's Seasonally Adjusted Unemployment Rate in January 2011 Is 11.9 PercentMichael AllenОценок пока нет

- Florida's September Employment Figures Released: Charlie Crist Cynthia R. LorenzoДокумент16 страницFlorida's September Employment Figures Released: Charlie Crist Cynthia R. LorenzoMichael AllenОценок пока нет

- What Is Really Killing The Irish EconomyДокумент1 страницаWhat Is Really Killing The Irish EconomyLuis Riestra Delgado100% (1)

- On InflationДокумент10 страницOn Inflationmajor raveendraОценок пока нет

- Florida's August Employment Figures Released: Charlie Crist Cynthia R. LorenzoДокумент16 страницFlorida's August Employment Figures Released: Charlie Crist Cynthia R. LorenzoMichael AllenОценок пока нет

- September 2010Документ1 страницаSeptember 2010Stephanie Miller HofmanОценок пока нет

- Proceso Obtencion de EtanoДокумент26 страницProceso Obtencion de EtanorubenpeОценок пока нет

- 23) Sacramento, CA: Figure 157: Year/Year Change in Existing Home Prices - Sacramento, CAДокумент11 страниц23) Sacramento, CA: Figure 157: Year/Year Change in Existing Home Prices - Sacramento, CAsacrealstatsОценок пока нет

- Trading Journal Template 34Документ2 страницыTrading Journal Template 34Dery AnggaraОценок пока нет

- athenian-shipbrokers-NOV 2010Документ17 страницathenian-shipbrokers-NOV 2010Nguyen Le Thu HaОценок пока нет

- Gantt Chart 17Документ1 страницаGantt Chart 17Bharti KashyapОценок пока нет

- The Pessimist Complains About The Wind The Optimist Expects It To Change The Realist Adjusts The Sails.Документ36 страницThe Pessimist Complains About The Wind The Optimist Expects It To Change The Realist Adjusts The Sails.brundbakenОценок пока нет

- (Four County Totals) Price Per SQ Foot vs. Residential Resale InventoryДокумент5 страниц(Four County Totals) Price Per SQ Foot vs. Residential Resale InventoryJim HamiltonОценок пока нет

- Livestock Price Volatility: Eric BelascoДокумент15 страницLivestock Price Volatility: Eric BelascoGlen YОценок пока нет

- Equity Debt Strategy For Mar20Документ25 страницEquity Debt Strategy For Mar20Saad KhanОценок пока нет

- Update On IDFC Arbitrage FundДокумент6 страницUpdate On IDFC Arbitrage FundGОценок пока нет

- Rents and Yields Q1-2009Документ5 страницRents and Yields Q1-2009avisitoronscribdОценок пока нет

- Chart PendingsДокумент1 страницаChart PendingsHeather MendoncaОценок пока нет

- MHIFU HandoutДокумент2 страницыMHIFU HandoutThunder PigОценок пока нет

- Florida's June Employment Figures Released: Governor DirectorДокумент16 страницFlorida's June Employment Figures Released: Governor DirectorMichael AllenОценок пока нет

- Innovation and The Financial CrisisДокумент20 страницInnovation and The Financial Crisisttunguz100% (3)

- Lupin Corporate Governance EthicsДокумент13 страницLupin Corporate Governance Ethicshagar sudhaОценок пока нет

- Liquidity Risk in Corporate Bond Markets: George Chacko Harvard Business School & IFLДокумент26 страницLiquidity Risk in Corporate Bond Markets: George Chacko Harvard Business School & IFLbadaberaОценок пока нет

- Southeast Texas Labor StatisticsДокумент1 страницаSoutheast Texas Labor StatisticsCharlie FoxworthОценок пока нет

- ch015Документ11 страницch015iatfirmforyouОценок пока нет

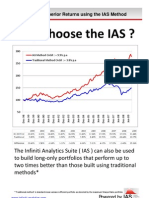

- Why Choose The IASДокумент6 страницWhy Choose The IASPeter UrbaniОценок пока нет

- Gerald CorcoranДокумент9 страницGerald CorcoranMarketsWikiОценок пока нет

- 74 Sme Mining Engineering HandbookДокумент1 страница74 Sme Mining Engineering HandbookYeimsОценок пока нет

- Hanford Performance Indicator Forum Statistical Process Control June 2005Документ25 страницHanford Performance Indicator Forum Statistical Process Control June 2005Vi KraОценок пока нет

- Managing The Financial Crisis: Argentina (2002)Документ63 страницыManaging The Financial Crisis: Argentina (2002)ankushishwarОценок пока нет

- Hondacivic ArДокумент2 страницыHondacivic Arapi-3709675Оценок пока нет

- Chart PricesДокумент1 страницаChart PricesHeather MendoncaОценок пока нет

- Unemployment DataДокумент2 страницыUnemployment Datakettle1Оценок пока нет

- Price To Earnings Ratio A State of Art ReviewДокумент6 страницPrice To Earnings Ratio A State of Art ReviewAYMAN HALALОценок пока нет

- Atlanta TieredДокумент1 страницаAtlanta Tieredkettle1Оценок пока нет

- Growth-Trend Timing and 60-40 Variations: Lethargic Asset Allocation (LAA)Документ15 страницGrowth-Trend Timing and 60-40 Variations: Lethargic Asset Allocation (LAA)Ricardo GutierrezОценок пока нет

- South Korean Energy Outlook 2015Документ13 страницSouth Korean Energy Outlook 2015Afifa KamilaОценок пока нет

- Drainase Dan Sanitasi: Kelompok 4 Kelas BДокумент25 страницDrainase Dan Sanitasi: Kelompok 4 Kelas BDimas AzhariОценок пока нет

- Goldman Asia Conviction Call Catch-Up 13sep10Документ11 страницGoldman Asia Conviction Call Catch-Up 13sep10tanmartinОценок пока нет

- Itr-V: Income Tax Return Verification Form IndianДокумент1 страницаItr-V: Income Tax Return Verification Form Indianapi-25886395Оценок пока нет

- NullДокумент13 страницNullapi-25886395Оценок пока нет

- Form ITR-1Документ3 страницыForm ITR-1Rajeev PuthuparambilОценок пока нет

- Reserve Bank of India Foreign Exchange Department Central Office Mumbai - 400 001Документ2 страницыReserve Bank of India Foreign Exchange Department Central Office Mumbai - 400 001api-25886395Оценок пока нет

- NotificationДокумент7 страницNotificationapi-25886395Оценок пока нет

- Reserve Bank of India Foreign Exchange Department Central Office Mumbai - 400 001Документ2 страницыReserve Bank of India Foreign Exchange Department Central Office Mumbai - 400 001api-25886395Оценок пока нет

- NullДокумент22 страницыNullapi-25886395Оценок пока нет

- Important Notice: As Per Recent RBI GuidelinesДокумент1 страницаImportant Notice: As Per Recent RBI Guidelinesapi-25886395Оценок пока нет

- Securities and Exchange Board of India: WWW - Corpfiling.co - inДокумент1 страницаSecurities and Exchange Board of India: WWW - Corpfiling.co - inapi-25886395Оценок пока нет

- Highlights of BudgetДокумент3 страницыHighlights of Budgetapi-25886395Оценок пока нет

- Important Notice: As Per Recent RBI GuidelinesДокумент1 страницаImportant Notice: As Per Recent RBI Guidelinesapi-25886395Оценок пока нет

- Various Examples :illustration : - 1 CompanyДокумент6 страницVarious Examples :illustration : - 1 Companyapi-25886395Оценок пока нет

- Report Highlights: India's GDP To Quadruple To INR 205 TRNДокумент7 страницReport Highlights: India's GDP To Quadruple To INR 205 TRNapi-25886395Оценок пока нет

- Highlights of BudgetДокумент3 страницыHighlights of Budgetapi-25886395Оценок пока нет

- Key Features of Budget 2010-2011Документ14 страницKey Features of Budget 2010-2011api-25886395Оценок пока нет

- (Published in The Gazette of IndiaДокумент6 страниц(Published in The Gazette of Indiaapi-25886395Оценок пока нет

- NullДокумент20 страницNullapi-25886395Оценок пока нет

- Reserve Bank of India: UBD - PCB.Cir. No. 50 /13.05.000/2007-08Документ1 страницаReserve Bank of India: UBD - PCB.Cir. No. 50 /13.05.000/2007-08api-25886395Оценок пока нет

- S&P CNX Nif T yДокумент15 страницS&P CNX Nif T yapi-25886395Оценок пока нет

- Legal DigestДокумент1 страницаLegal Digestapi-25886395Оценок пока нет

- Key Features of Budget 2010-2011Документ14 страницKey Features of Budget 2010-2011api-25886395Оценок пока нет

- (Published in The Gazette of IndiaДокумент6 страниц(Published in The Gazette of Indiaapi-25886395Оценок пока нет

- Views On Union BudgetДокумент1 страницаViews On Union Budgetapi-25886395Оценок пока нет

- Speech of Mamata Banerjee Introducing The RailwayДокумент47 страницSpeech of Mamata Banerjee Introducing The Railwayapi-25886395Оценок пока нет

- RESERVE BANK of INDIA Foreign Exchange DepartmentДокумент2 страницыRESERVE BANK of INDIA Foreign Exchange Departmentapi-25886395Оценок пока нет

- RBI - BPLR To Base Rate ChangeДокумент4 страницыRBI - BPLR To Base Rate Changeankit_gupta_92Оценок пока нет

- Speech of Mamata Banerjee Introducing The RailwayДокумент47 страницSpeech of Mamata Banerjee Introducing The Railwayapi-25886395Оценок пока нет

- Rbi/2009-10/323 Dpss - Co.chd - No. 1832 / 04.07.05 / 2009-10Документ6 страницRbi/2009-10/323 Dpss - Co.chd - No. 1832 / 04.07.05 / 2009-10api-25886395Оценок пока нет

- Mechanism of Muscle ContractionДокумент24 страницыMechanism of Muscle Contractionfisika100% (1)

- Edan M3B Vital Signs Monitor User ManualДокумент92 страницыEdan M3B Vital Signs Monitor User ManualJosé marino Franco AlzateОценок пока нет

- Formula Sheet: Basic Trigonometric IdentitiesДокумент4 страницыFormula Sheet: Basic Trigonometric Identitieschetan temkarОценок пока нет

- Mbs PartitionwallДокумент91 страницаMbs PartitionwallRamsey RasmeyОценок пока нет

- 7PA30121AA000 Datasheet enДокумент2 страницы7PA30121AA000 Datasheet enMirko DjukanovicОценок пока нет

- 02 WholeДокумент344 страницы02 WholeedithgclemonsОценок пока нет

- Alimak Alc - IIДокумент62 страницыAlimak Alc - IImoiburОценок пока нет

- The Library of Babel - WikipediaДокумент35 страницThe Library of Babel - WikipediaNeethu JosephОценок пока нет

- Pile FoundationДокумент38 страницPile FoundationChowdhury PriodeepОценок пока нет

- Module 1 Grade 8 (De Guzman)Документ9 страницModule 1 Grade 8 (De Guzman)Kim De GuzmanОценок пока нет

- Chapter One PDFДокумент74 страницыChapter One PDFAdelu BelleteОценок пока нет

- Completing The Square PDFДокумент10 страницCompleting The Square PDFgreg heffleyОценок пока нет

- List of GHS Hazard Statement & PictogramsДокумент33 страницыList of GHS Hazard Statement & PictogramsKhairul BarsriОценок пока нет

- 1SFC132367M0201 PSE Internal Modbus RTUДокумент22 страницы1SFC132367M0201 PSE Internal Modbus RTUAhmed OsmanОценок пока нет

- X-Plane Mobile ManualДокумент66 страницX-Plane Mobile ManualRafael MunizОценок пока нет

- Type 85 Di Box DatasheetДокумент2 страницыType 85 Di Box DatasheetmegadeОценок пока нет

- RTL8139D DataSheetДокумент60 страницRTL8139D DataSheetRakesh NettemОценок пока нет

- Acuvim II Profibus Modules Users Manual v1.10Документ36 страницAcuvim II Profibus Modules Users Manual v1.10kamran719Оценок пока нет

- RomerДокумент20 страницRomerAkistaaОценок пока нет

- Algebra 2: 9-Week Common Assessment ReviewДокумент5 страницAlgebra 2: 9-Week Common Assessment Reviewapi-16254560Оценок пока нет

- DC Power Supply and Voltage RegulatorsДокумент73 страницыDC Power Supply and Voltage RegulatorsRalph Justine NevadoОценок пока нет

- Latihan Matematik DLP Minggu 1Документ3 страницыLatihan Matematik DLP Minggu 1Unit Sains Komputer MRSM PendangОценок пока нет

- Index Terms LinksДокумент31 страницаIndex Terms Linksdeeptiwagle5649Оценок пока нет

- Student - The Passive Voice Without AnswersДокумент5 страницStudent - The Passive Voice Without AnswersMichelleОценок пока нет

- Magnetism NotesДокумент14 страницMagnetism Notesapi-277818647Оценок пока нет