Вам также может понравиться

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (120)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Case 15 Pacific Healthcare - B - Student - 6th EditionДокумент1 страницаCase 15 Pacific Healthcare - B - Student - 6th EditionAhmed MahmoudОценок пока нет

- Chap - 33 Aggregate Demand & Aggregate SupplyДокумент28 страницChap - 33 Aggregate Demand & Aggregate SupplyUdevir SinghОценок пока нет

- Treasurer'S Affidavit: Republic of The Philippines) City of Taguig) S.S. Metro Manila)Документ2 страницыTreasurer'S Affidavit: Republic of The Philippines) City of Taguig) S.S. Metro Manila)Maria Andres50% (2)

- Business Plan On HIRING A MAIDДокумент21 страницаBusiness Plan On HIRING A MAIDharsha100% (1)

- 2017 Walters Global Salary SurveyДокумент428 страниц2017 Walters Global Salary SurveyDebbie CollettОценок пока нет

- Freehold and LeaseholdДокумент3 страницыFreehold and LeaseholdDayah AyoebОценок пока нет

- RAD Project PlanДокумент9 страницRAD Project PlannasoonyОценок пока нет

- A Comparative Analysis On Fuel-Oil Distribution Companies of BangladeshДокумент15 страницA Comparative Analysis On Fuel-Oil Distribution Companies of BangladeshTanzir HasanОценок пока нет

- Design and Implementation of Real Processing in Accounting Information SystemДокумент66 страницDesign and Implementation of Real Processing in Accounting Information Systemenbassey100% (2)

- Project Appraisal FinanceДокумент20 страницProject Appraisal Financecpsandeepgowda6828Оценок пока нет

- NAFTA Verification and Audit ManualДокумент316 страницNAFTA Verification and Audit Manualbiharris22Оценок пока нет

- Helmet Jan19 PDFДокумент31 страницаHelmet Jan19 PDFLokeshОценок пока нет

- Product Differentiation and Market Segmentation As Alternative Marketing StrategiesДокумент7 страницProduct Differentiation and Market Segmentation As Alternative Marketing Strategiesshoka1388Оценок пока нет

- Sky Roofing - PresentationДокумент10 страницSky Roofing - PresentationViswanathan RamasamyОценок пока нет

- Alliance Governance at Klarna: Managing and Controlling Risks of An Alliance PortfolioДокумент9 страницAlliance Governance at Klarna: Managing and Controlling Risks of An Alliance PortfolioAbhishek SinghОценок пока нет

- BEGovSoc323 CSR 4Документ24 страницыBEGovSoc323 CSR 4Romeo DupaОценок пока нет

- VP Director Sales Pharmaceuticals in Philadelphia PA Resume James BruniДокумент3 страницыVP Director Sales Pharmaceuticals in Philadelphia PA Resume James BruniJamesBruni10% (1)

- Lesson 5Документ31 страницаLesson 5Glenda DestrizaОценок пока нет

- Governance, Risk and Dataveillance in The War On TerrorДокумент25 страницGovernance, Risk and Dataveillance in The War On Terroreliasox123Оценок пока нет

- TALO - 21Q - Listening Unit 2 - Phan Thị Hoài Thu30Документ17 страницTALO - 21Q - Listening Unit 2 - Phan Thị Hoài Thu30Mi HíОценок пока нет

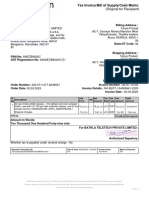

- InvoiceДокумент1 страницаInvoicetanya.prasadОценок пока нет

- Midsemester Practice QuestionsДокумент6 страницMidsemester Practice Questionsoshane126Оценок пока нет

- SM TAYTAY - New Tenant Profile Form PDFДокумент2 страницыSM TAYTAY - New Tenant Profile Form PDFtokstutonОценок пока нет

- Hypothesis Testing For A Single PopulationДокумент37 страницHypothesis Testing For A Single PopulationAna Salud LimОценок пока нет

- Shivani Singhal: Email: PH: 9718369255Документ4 страницыShivani Singhal: Email: PH: 9718369255ravigompaОценок пока нет

- Training Levies: Rationale and Evidence From EvaluationsДокумент17 страницTraining Levies: Rationale and Evidence From EvaluationsGakuya KamboОценок пока нет

- Perfetti (Himanshu)Документ84 страницыPerfetti (Himanshu)Sanjay Panwar33% (3)

- Macro 03Документ381 страницаMacro 03subroto36100% (1)

- Curriculum ViateДокумент1 страницаCurriculum ViateOssaОценок пока нет