Вам также может понравиться

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Essential Business LettersДокумент245 страницEssential Business Lettersmaestro921189% (18)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- Affidavit of TransferorДокумент1 страницаAffidavit of TransferorIvyGwynn214100% (2)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Suggested Answers in Criminal Law Bar ExamsДокумент88 страницSuggested Answers in Criminal Law Bar ExamsRoni Tapeño75% (8)

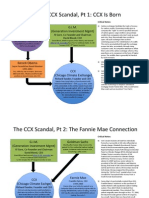

- CCX Scandal, Chicago Carbon ExchangeДокумент4 страницыCCX Scandal, Chicago Carbon ExchangeKim HedumОценок пока нет

- Bar Qs 1990-2015 Updated CRIMINAL LAWДокумент117 страницBar Qs 1990-2015 Updated CRIMINAL LAWjade123_12985% (13)

- Alvie Explains It : Assignment Fraud - BifurcationДокумент8 страницAlvie Explains It : Assignment Fraud - BifurcationA. CampbellОценок пока нет

- Affidavit of SupportДокумент2 страницыAffidavit of SupportIvyGwynn21490% (10)

- Self-Adjudication of Real Estate PropertyДокумент2 страницыSelf-Adjudication of Real Estate PropertyIvyGwynn214Оценок пока нет

- Affidavit of TransfereeДокумент1 страницаAffidavit of TransfereeIvyGwynn214100% (3)

- Affidavit of Discrepancy (Middle Name)Документ1 страницаAffidavit of Discrepancy (Middle Name)IvyGwynn214100% (1)

- Affidavit of Withdrawal As CounselДокумент2 страницыAffidavit of Withdrawal As CounselIvyGwynn214Оценок пока нет

- Affidavit on business name change complianceДокумент1 страницаAffidavit on business name change complianceIvyGwynn21483% (6)

- Affidavit of Guardianship for Minor's PAG-IBIG BenefitsДокумент1 страницаAffidavit of Guardianship for Minor's PAG-IBIG BenefitsIvyGwynn214Оценок пока нет

- Affidavit of employment without contractДокумент1 страницаAffidavit of employment without contractIvyGwynn214Оценок пока нет

- Mortgages SlidesДокумент66 страницMortgages SlidesFuck You100% (1)

- TI-BAII Plus TVM Functions PDFДокумент32 страницыTI-BAII Plus TVM Functions PDFPutera Petir GundalaОценок пока нет

- Generic Motion To Dismiss ForeclosureДокумент6 страницGeneric Motion To Dismiss ForeclosureJames V Magee JrОценок пока нет

- Affidavit of Loss (PHILHEALTH ID)Документ1 страницаAffidavit of Loss (PHILHEALTH ID)IvyGwynn214Оценок пока нет

- Court Rules Legal Interest Rate Applies to Unpaid LoanДокумент1 страницаCourt Rules Legal Interest Rate Applies to Unpaid LoanCharles Roger Raya100% (1)

- Affidavit of ownership for pledge of vehicle and computerДокумент2 страницыAffidavit of ownership for pledge of vehicle and computerIvyGwynn214100% (2)

- Affidavit corrects child's nameДокумент1 страницаAffidavit corrects child's nameIvyGwynn21475% (4)

- Affidavit of Non-Operation of BusinessДокумент1 страницаAffidavit of Non-Operation of BusinessIvyGwynn214Оценок пока нет

- Affidavit of Non EmploymentДокумент1 страницаAffidavit of Non EmploymentIvyGwynn21425% (4)

- Affidavit of WarrantyДокумент2 страницыAffidavit of WarrantyIvyGwynn21467% (3)

- Affidavit transfer land sale PhilippinesДокумент2 страницыAffidavit transfer land sale PhilippinesIvyGwynn214100% (1)

- Affidavit of Discrepancy (Date of Marriage of Parents)Документ1 страницаAffidavit of Discrepancy (Date of Marriage of Parents)IvyGwynn214100% (1)

- Affidavit of PublicationДокумент1 страницаAffidavit of PublicationIvyGwynn214Оценок пока нет

- Unblock stolen Samsung Galaxy S IIIДокумент2 страницыUnblock stolen Samsung Galaxy S IIIIvyGwynn214100% (1)

- Correct birth name affidavitДокумент2 страницыCorrect birth name affidavitIvyGwynn214100% (3)

- Lost SSS ID AffidavitДокумент1 страницаLost SSS ID AffidavitIvyGwynn214Оценок пока нет

- Affidavit of Certifcation of TrueДокумент1 страницаAffidavit of Certifcation of TrueIvyGwynn214Оценок пока нет

- Affidavit of IllegitimacyДокумент1 страницаAffidavit of IllegitimacyIvyGwynn214Оценок пока нет

- Affidavit of NonTenancyДокумент2 страницыAffidavit of NonTenancyIvyGwynn214Оценок пока нет

- Affidavit of Consent For Travel of A Minor AbroadДокумент2 страницыAffidavit of Consent For Travel of A Minor AbroadIvyGwynn214Оценок пока нет

- Affidavit of Loss (Passport)Документ2 страницыAffidavit of Loss (Passport)IvyGwynn214Оценок пока нет

- Affidavit of Birth by Two Disinterested PersonsДокумент2 страницыAffidavit of Birth by Two Disinterested PersonsIvyGwynn214Оценок пока нет

- Affidavit of DesistanceДокумент2 страницыAffidavit of DesistanceIvyGwynn214Оценок пока нет

- RE: Debt Owed To AGL Retail Energy Limited (The Creditor) Property AddressДокумент2 страницыRE: Debt Owed To AGL Retail Energy Limited (The Creditor) Property Addressapi-74302875Оценок пока нет

- June 24Документ48 страницJune 24fijitimescanadaОценок пока нет

- Be A Property MillionaireДокумент4 страницыBe A Property Millionairengsw9999Оценок пока нет

- Resume - Tushar A. Kudtarkar FinalДокумент2 страницыResume - Tushar A. Kudtarkar FinalTushki TricksОценок пока нет

- 02 Sales Carrasoco V CAДокумент3 страницы02 Sales Carrasoco V CAOjie SantillanОценок пока нет

- HorngrenIMA14eSM ch07Документ57 страницHorngrenIMA14eSM ch07Aries Siringoringo50% (2)

- Commercial Banking in IndiaДокумент8 страницCommercial Banking in IndiaJavadsha VagadaОценок пока нет

- Bakhtar Bank Case StudyДокумент2 страницыBakhtar Bank Case StudyMuhammad Shafiq GulОценок пока нет

- Introduction of A Bank - EcoДокумент5 страницIntroduction of A Bank - EcoRoshni Singh100% (2)

- Trade Finance GuideДокумент2 страницыTrade Finance GuideMBASTUDENTPUPОценок пока нет

- Rising Interest RatesДокумент4 страницыRising Interest RatesRAJESH BHANDERIОценок пока нет

- Transforming Green Bond Markets Using Financial Innovation and Technology To Expand Green Bond Issuance in Latin America and The Caribbean enДокумент36 страницTransforming Green Bond Markets Using Financial Innovation and Technology To Expand Green Bond Issuance in Latin America and The Caribbean enJuan David DuarteОценок пока нет

- Review of Literature: Chapter-2Документ5 страницReview of Literature: Chapter-2Juan JacksonОценок пока нет

- Project OnДокумент17 страницProject OnashishОценок пока нет

- Housing Loan Suggestions and ChallengesДокумент4 страницыHousing Loan Suggestions and Challengesmariyam fathimaОценок пока нет

- Syed Md. Moinuddin Masum, ID: B123008, BBA (Finance & Banking) 1Документ59 страницSyed Md. Moinuddin Masum, ID: B123008, BBA (Finance & Banking) 1jennath moonОценок пока нет

- Straumann enДокумент26 страницStraumann enyeochunhongОценок пока нет

- MmiДокумент11 страницMmiaadeezusmanОценок пока нет

- Influence of Microfinance On Small Business Development in Namakkal District, TamilnaduДокумент5 страницInfluence of Microfinance On Small Business Development in Namakkal District, Tamilnaduarcherselevators100% (1)

- Insurance Law Quiz 2Документ2 страницыInsurance Law Quiz 2Samantha BaricauaОценок пока нет

- Offices of Thrift Services and Aurora Loan ServicingДокумент29 страницOffices of Thrift Services and Aurora Loan ServicingKelloggmanОценок пока нет

- Session 3-Summary PDFДокумент4 страницыSession 3-Summary PDFRajAt D Everaj EverajОценок пока нет

- Transcript of Philippine Star Interview With Rody DuterteДокумент5 страницTranscript of Philippine Star Interview With Rody DuterteRochelle Arayata AguilarОценок пока нет