Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- IfsДокумент23 страницыIfsRahul Kumar JainОценок пока нет

- Aud 2Документ7 страницAud 2Raymundo EirahОценок пока нет

- Đề thi thử Deloitte-ACE Intern 2021Документ60 страницĐề thi thử Deloitte-ACE Intern 2021Đặng Trần Huyền TrâmОценок пока нет

- Case Study On Equity ValuationДокумент3 страницыCase Study On Equity ValuationUbaid DarОценок пока нет

- Amplify University TrainingДокумент11 страницAmplify University Trainingshariz500100% (1)

- The Role of Investment Banking in IndiaДокумент13 страницThe Role of Investment Banking in IndiaGuneet SaurabhОценок пока нет

- Revised Corporation Code MnemonicsДокумент3 страницыRevised Corporation Code MnemonicsZicoОценок пока нет

- RWJ Chapter 1 - EUДокумент17 страницRWJ Chapter 1 - EULokkhi BowОценок пока нет

- DRAFT 1. Executive Summary and IntroductionДокумент12 страницDRAFT 1. Executive Summary and IntroductionAllana NacinoОценок пока нет

- Senior High School Department: Quarter 3 - Module 4: Debit and Credit-The Double - Entry SystemДокумент13 страницSenior High School Department: Quarter 3 - Module 4: Debit and Credit-The Double - Entry SystemJaye Ruanto100% (1)

- Characteristics of The RestaurantДокумент2 страницыCharacteristics of The RestaurantSudhansuSekharОценок пока нет

- Chapter 6 Sample ProblemsДокумент3 страницыChapter 6 Sample ProblemsShaiTengcoОценок пока нет

- Barings Bank CaseДокумент15 страницBarings Bank CaseRamya MattaОценок пока нет

- Spectrans M1 M2Документ7 страницSpectrans M1 M2Patricia CruzОценок пока нет

- Billing Address: Tax InvoiceДокумент1 страницаBilling Address: Tax InvoiceManojkumar DОценок пока нет

- Tax Invoice: Akbar & CompanyДокумент1 страницаTax Invoice: Akbar & CompanyTTIPLОценок пока нет

- Unit-1Financial Credit Risk AnalyticsДокумент40 страницUnit-1Financial Credit Risk AnalyticsAkshitОценок пока нет

- 3rd GovAcc 1SAY2324Документ9 страниц3rd GovAcc 1SAY2324Grand DuelistОценок пока нет

- ToolKit Roads&Highways Low-ResДокумент896 страницToolKit Roads&Highways Low-ResAbd Aziz MohamedОценок пока нет

- MBIДокумент16 страницMBIPankaj SharmaОценок пока нет

- Week 6 Case AnalysisДокумент2 страницыWeek 6 Case AnalysisVarun Abbineni0% (1)

- TT10 QuestionДокумент1 страницаTT10 QuestionUyển Nhi TrầnОценок пока нет

- Risk ManagementДокумент1 страницаRisk ManagementThảo NguyễnОценок пока нет

- LNT Grasim CaseДокумент9 страницLNT Grasim CaseRickMartinОценок пока нет

- CHAPTER 1 (STRUCTuRE OF MALAYSIAN FINANCIAL SYSTEM)Документ13 страницCHAPTER 1 (STRUCTuRE OF MALAYSIAN FINANCIAL SYSTEM)han guzelОценок пока нет

- Payment PDFДокумент1 страницаPayment PDFAMAN SAURAVОценок пока нет

- Ch.18 Revenue Recognition: Chapter Learning ObjectiveДокумент5 страницCh.18 Revenue Recognition: Chapter Learning ObjectiveFaishal Alghi FariОценок пока нет

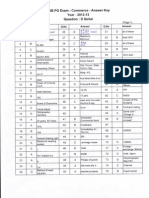

- TRB Commerce - PG - Answer Key 2012Документ2 страницыTRB Commerce - PG - Answer Key 2012babu4in1Оценок пока нет

- The Foreign Exchange Market NoteДокумент12 страницThe Foreign Exchange Market Noteరఘువీర్ సూర్యనారాయణОценок пока нет

- Internship Report On Deposit and Investment Management of Al Arafah Islami Bank LimitedДокумент211 страницInternship Report On Deposit and Investment Management of Al Arafah Islami Bank LimitedWahidHossainОценок пока нет