Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- Professor Vijay Shankar Vyas Iima Director Ids Imf Rbi World Bank & Advisor PmoДокумент1 страницаProfessor Vijay Shankar Vyas Iima Director Ids Imf Rbi World Bank & Advisor PmoKNOWLEDGE CREATORSОценок пока нет

- Social Entrepreneurship in Bikaner Article in Hindi Newspaper Dainik Yugpaksh Bikaner by Professor Trilok Kumar JainДокумент1 страницаSocial Entrepreneurship in Bikaner Article in Hindi Newspaper Dainik Yugpaksh Bikaner by Professor Trilok Kumar JainKNOWLEDGE CREATORSОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Poverty and Government Policies in Indian Context A Philosophical PerspectiveДокумент1 страницаPoverty and Government Policies in Indian Context A Philosophical PerspectiveKNOWLEDGE CREATORSОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Culture and Heritage of BIKANER in Hindi Newspaper Dainik Yugpaksh BikanerДокумент1 страницаCulture and Heritage of BIKANER in Hindi Newspaper Dainik Yugpaksh BikanerKNOWLEDGE CREATORSОценок пока нет

- Analysis of Revenue and Expenditure at Citi (Monica Alex Fernandes)Документ69 страницAnalysis of Revenue and Expenditure at Citi (Monica Alex Fernandes)Monica FernandesОценок пока нет

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Sub: Risk Assumption Letter: Insured & Vehicle DetailsДокумент2 страницыSub: Risk Assumption Letter: Insured & Vehicle Detailsumang malviyaОценок пока нет

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Challan Form SargodhaДокумент1 страницаChallan Form SargodhaUsama NazirОценок пока нет

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Sales IllustrationДокумент23 страницыSales IllustrationMahakala AnahatakeshwaraОценок пока нет

- Analysis of Icici PrudentialДокумент118 страницAnalysis of Icici PrudentialAnuj AgarwalОценок пока нет

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- Bharti Axa Bike Insurance OriginalДокумент1 страницаBharti Axa Bike Insurance OriginalAyaz SayedОценок пока нет

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- 2006 - Dec - QUS CAT T3Документ9 страниц2006 - Dec - QUS CAT T3asad190% (1)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- 03 05Документ24 страницы03 05CoolerAdsОценок пока нет

- Car Loan ApplicationДокумент2 страницыCar Loan Applicationapi-453439542Оценок пока нет

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Secured Transactions Spring 2010Документ81 страницаSecured Transactions Spring 2010Joshua Ryan Collums100% (1)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- A Report On NLIДокумент12 страницA Report On NLIMohammad AbdullahОценок пока нет

- Summary of Account As On 30-11-2022 I. Operative Account in INRДокумент25 страницSummary of Account As On 30-11-2022 I. Operative Account in INRAntony SureshОценок пока нет

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Non Binding Application Form 2019Документ10 страницNon Binding Application Form 2019AmalkpОценок пока нет

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1091)

- Class 11 AccoutancyДокумент5 страницClass 11 AccoutancyRavikumar BalasubramanianОценок пока нет

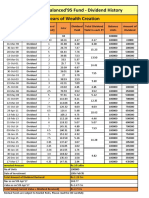

- Dividend HistoryДокумент1 страницаDividend HistoryJeetendra KumarОценок пока нет

- LC ApplicationДокумент2 страницыLC ApplicationShruti BudhirajaОценок пока нет

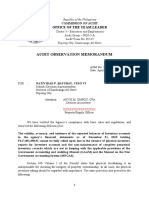

- Office of The Auditor Construction Industry Authority of The PhilippinesДокумент3 страницыOffice of The Auditor Construction Industry Authority of The PhilippinesHoven MacasinagОценок пока нет

- UntitledДокумент7 страницUntitledSimply Debt SolutionsОценок пока нет

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- About Payments System in PNG - Bank of Papua New Guinea (PNG) Port Moresby, Papua New GuineaДокумент2 страницыAbout Payments System in PNG - Bank of Papua New Guinea (PNG) Port Moresby, Papua New GuineaKSeegurОценок пока нет

- Notice For Seeking Public Comments - Panther TyresДокумент144 страницыNotice For Seeking Public Comments - Panther TyresMuhammad Ahmed MirzaОценок пока нет

- Financial Accounting Ii Sample QuizДокумент2 страницыFinancial Accounting Ii Sample QuizThea FloresОценок пока нет

- IC Exam Review 2Документ4 страницыIC Exam Review 2Jason BagadiongОценок пока нет

- AOM - Inventory v4Документ4 страницыAOM - Inventory v4russel1435Оценок пока нет

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Flow of Funds ReportДокумент2 страницыFlow of Funds ReportAlexia JingОценок пока нет

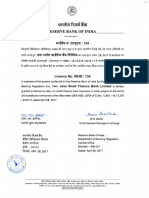

- RBI Approved BankДокумент1 страницаRBI Approved BankVįňäý Ğøwđã VįñîОценок пока нет

- C++ Flowchart Atm MachineДокумент1 страницаC++ Flowchart Atm MachineAshwin Asogan100% (1)

- Karnataka I PUC Accountancy 2019 Model Question Paper 1Документ7 страницKarnataka I PUC Accountancy 2019 Model Question Paper 1Lokesh Rao100% (1)

- Final Project of Indusind BankДокумент104 страницыFinal Project of Indusind Banknikhil chikhaleОценок пока нет

- Chapter 6 (Payment Systems in E-Commerce)Документ40 страницChapter 6 (Payment Systems in E-Commerce)Atik Israk LemonОценок пока нет

- Recording of Reissue of SharesДокумент6 страницRecording of Reissue of SharesRAJASEKAR176Оценок пока нет