Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- 10 Profitability RatiosДокумент12 страниц10 Profitability RatiosirfantanjungОценок пока нет

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The Role of Intellectual Capital in The Succes of New VenturesДокумент22 страницыThe Role of Intellectual Capital in The Succes of New VenturesirfantanjungОценок пока нет

- CH02 Systems Techniques and DocumentationДокумент50 страницCH02 Systems Techniques and DocumentationirfantanjungОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- CH01 Accounting Information Systems - An OverviewДокумент46 страницCH01 Accounting Information Systems - An OverviewirfantanjungОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Intellectual Capital and Business Performance in The Portuguese Banking Industry Cabritabontisijtm43 PDFДокумент26 страницIntellectual Capital and Business Performance in The Portuguese Banking Industry Cabritabontisijtm43 PDFirfantanjungОценок пока нет

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Soal Cpns Bahasa Inggris2Документ9 страницSoal Cpns Bahasa Inggris2AlpajriОценок пока нет

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Corporate Governance, Bank Specific Characteristics, Banking Industry Characteristics, and Intellectual Capital (Ic) Performance of Banks in Arab Gulf Cooperation Council (GCC) CountriesДокумент20 страницCorporate Governance, Bank Specific Characteristics, Banking Industry Characteristics, and Intellectual Capital (Ic) Performance of Banks in Arab Gulf Cooperation Council (GCC) CountriesirfantanjungОценок пока нет

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Role of Intellectual Capital in The Succes of New VenturesДокумент22 страницыThe Role of Intellectual Capital in The Succes of New VenturesirfantanjungОценок пока нет

- Intellectual Capital Accounts Reporting and Managing Intellectual CapitalДокумент81 страницаIntellectual Capital Accounts Reporting and Managing Intellectual CapitalirfantanjungОценок пока нет

- Bontis JHRCAДокумент15 страницBontis JHRCARafaelrsantosОценок пока нет

- Organizational Culture PDFДокумент19 страницOrganizational Culture PDFirfantanjung100% (1)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Organizational Culture PDFДокумент19 страницOrganizational Culture PDFirfantanjung100% (1)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- f1 Answers Nov14Документ14 страницf1 Answers Nov14Atif Rehman100% (1)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Advanced Accounting Homework Week 6Документ5 страницAdvanced Accounting Homework Week 6JomarОценок пока нет

- Chapter Two International Public Sector Accounting Standard (Ipsas) Ipsas 1 Presentation of Financial StatementsДокумент21 страницаChapter Two International Public Sector Accounting Standard (Ipsas) Ipsas 1 Presentation of Financial StatementsSara NegashОценок пока нет

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Audit of Stockholders Equity StudentsДокумент5 страницAudit of Stockholders Equity StudentsJames R JunioОценок пока нет

- Apollo Global Asset Backed Finance White PaperДокумент16 страницApollo Global Asset Backed Finance White PaperstieberinspirujОценок пока нет

- AFAR 2204 Joint ArrangementsДокумент11 страницAFAR 2204 Joint ArrangementsJefferson ArayОценок пока нет

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Unity Small Finance Bank LimitedДокумент10 страницUnity Small Finance Bank LimitedMainathan NagarajanОценок пока нет

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- AR - KRAH - 2013 - PT Grand Kartech TBK (Resize) PDFДокумент145 страницAR - KRAH - 2013 - PT Grand Kartech TBK (Resize) PDFSetiaji ATОценок пока нет

- Cfas ReviewerДокумент6 страницCfas Reviewerkeisha santosОценок пока нет

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Assignment On Entrepreneurship and Economic DevelopmentДокумент28 страницAssignment On Entrepreneurship and Economic Developmentgosaye desalegn100% (2)

- IAS 16 Problem SolutionsДокумент2 страницыIAS 16 Problem SolutionsRimsha ArifОценок пока нет

- Chapter 13 - 8.9.2021Документ10 страницChapter 13 - 8.9.2021Zi Yan HoonОценок пока нет

- 3.13 Concept Map - Shareholders' Equity Part IДокумент2 страницы3.13 Concept Map - Shareholders' Equity Part IShawn Cassidy F. GarciaОценок пока нет

- Aquabest To PrintДокумент49 страницAquabest To PrintJohn Kenneth Bohol100% (1)

- Capital StructureДокумент30 страницCapital StructureAmit KumarОценок пока нет

- Sunshine Income Statement For The Year Ending September 30, 2014 NoteДокумент4 страницыSunshine Income Statement For The Year Ending September 30, 2014 Notesanjay blakeОценок пока нет

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Research ProposalДокумент34 страницыResearch ProposalSimon Muteke100% (1)

- 117 - Florete, Jr. V FloreteДокумент1 страница117 - Florete, Jr. V FloreteMaria Francheska Garcia100% (1)

- A Comparative Study of Performance of Local Banks in Sultanate of OmanДокумент10 страницA Comparative Study of Performance of Local Banks in Sultanate of OmanResearch StudiesОценок пока нет

- John Ervin Bonilla Bsba Fm2B 1. Admission by Purchase of InterestДокумент8 страницJohn Ervin Bonilla Bsba Fm2B 1. Admission by Purchase of InterestJohn Ervin Bonilla100% (4)

- Australian Dairy Industry: A Review of TheДокумент51 страницаAustralian Dairy Industry: A Review of Thevivek_pandeyОценок пока нет

- Cambium Annual Report 2009Документ56 страницCambium Annual Report 2009Qinhai XiaОценок пока нет

- PR 373Документ3 страницыPR 373Anonymous Feglbx5Оценок пока нет

- GRIRДокумент29 страницGRIRPromoth JaidevОценок пока нет

- Conceptual Framework - Chapter 1Документ2 страницыConceptual Framework - Chapter 1Miko Louis ManligoyОценок пока нет

- Determinants of Dividend PolicyДокумент15 страницDeterminants of Dividend PolicyJanvi AroraОценок пока нет

- Operating Activities:: What Are The Classification of Cash Flow?Документ5 страницOperating Activities:: What Are The Classification of Cash Flow?samm yuuОценок пока нет

- Bac 305 Financial Mkts Lecture Notes BackupДокумент150 страницBac 305 Financial Mkts Lecture Notes BackupHufzi KhanОценок пока нет

- India Hospitals - Capital Discipline Improving - HSIE-202104061417420581720Документ63 страницыIndia Hospitals - Capital Discipline Improving - HSIE-202104061417420581720Text81Оценок пока нет

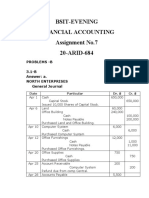

- Assignment No.7 AccountingДокумент7 страницAssignment No.7 Accountingibrar ghaniОценок пока нет