Вам также может понравиться

- How To Buy and Sell Your Home With Confidence July 2012-1Документ14 страницHow To Buy and Sell Your Home With Confidence July 2012-1Josh LeBlancОценок пока нет

- The Government Subcontractor's Guide to Terms and ConditionsОт EverandThe Government Subcontractor's Guide to Terms and ConditionsОценок пока нет

- Massachusetts Mandatory Licensee Consumer Relationship DisclosureДокумент2 страницыMassachusetts Mandatory Licensee Consumer Relationship DisclosureRichard VetsteinОценок пока нет

- Agency Disclosure and Acknowledgement-DigiSignДокумент3 страницыAgency Disclosure and Acknowledgement-DigiSignMorenita ParelesОценок пока нет

- Loan Modifications, Foreclosures and Saving Your Home: With an Affordable Loan Modification AgreementОт EverandLoan Modifications, Foreclosures and Saving Your Home: With an Affordable Loan Modification AgreementОценок пока нет

- Short Sales - An Overview and Warning To Real Estate Licensees Re: Fraud, and Legal and Ethical MinefieldsДокумент7 страницShort Sales - An Overview and Warning To Real Estate Licensees Re: Fraud, and Legal and Ethical Minefieldsapi-25884946Оценок пока нет

- Raising Money – Legally: A Practical Guide to Raising CapitalОт EverandRaising Money – Legally: A Practical Guide to Raising CapitalРейтинг: 4 из 5 звезд4/5 (1)

- Eport:: Toxic Document Fallout ImpactsДокумент21 страницаEport:: Toxic Document Fallout ImpactsRichard Franklin Kessler100% (1)

- Real Estate Professionals: Licensing RequirementДокумент13 страницReal Estate Professionals: Licensing RequirementanjeeОценок пока нет

- Legal Concepts for Insurance Agent Ethics: How Agents Get Sued and Lose Their LicensesОт EverandLegal Concepts for Insurance Agent Ethics: How Agents Get Sued and Lose Their LicensesОценок пока нет

- Sample ContractДокумент12 страницSample ContractVictoria RoseОценок пока нет

- 2015 Working With A REALTORRДокумент1 страница2015 Working With A REALTORRJayОценок пока нет

- Consumer Alert : Warning Regarding Residential "Short" SalesДокумент3 страницыConsumer Alert : Warning Regarding Residential "Short" SalesSteve Mun Group100% (1)

- 16 AgencyAndBrokerage TextДокумент18 страниц16 AgencyAndBrokerage TextLillian KobusingyeОценок пока нет

- Connecticut Mandatory Disclosure of Real Estate Agency RelationshipsДокумент6 страницConnecticut Mandatory Disclosure of Real Estate Agency RelationshipsRobert OramОценок пока нет

- Law of Real Estate Agency PamphletДокумент7 страницLaw of Real Estate Agency PamphletSusan Marcoe DraperОценок пока нет

- Notary Must Not Have Interest in DocumentДокумент2 страницыNotary Must Not Have Interest in DocumentEileen CokerОценок пока нет

- Your House May Be Taken Away by A Ham Sandwich - Richard Kessler - December 19Документ3 страницыYour House May Be Taken Away by A Ham Sandwich - Richard Kessler - December 19DinSFLA100% (1)

- Professional NegligenceДокумент15 страницProfessional NegligenceAnuradi ShanikaОценок пока нет

- CIV Case DigestДокумент86 страницCIV Case DigestvalkyriorОценок пока нет

- Case Digests in Civil Law (1995-2001)Документ86 страницCase Digests in Civil Law (1995-2001)westernwound82Оценок пока нет

- Escrow Institute of CaliforniaДокумент5 страницEscrow Institute of California51 PegasiОценок пока нет

- OREA Course 2 QuestionsДокумент139 страницOREA Course 2 QuestionsCourseTree LearningОценок пока нет

- The ABCs of Agency (2018)Документ2 страницыThe ABCs of Agency (2018)Angel KnightОценок пока нет

- Working With A REALTOR - BrochureДокумент2 страницыWorking With A REALTOR - BrochureBrian WisemanОценок пока нет

- New York State Agency Disclosure FormДокумент2 страницыNew York State Agency Disclosure FormncontxtОценок пока нет

- AGENCY Asgment LawДокумент16 страницAGENCY Asgment LawIeka TaharОценок пока нет

- Table of ContentsДокумент10 страницTable of Contentsbello aminatОценок пока нет

- Creditors in Commerce Workshop SessionsДокумент17 страницCreditors in Commerce Workshop SessionsJulian Williams©™100% (17)

- (Ontario) 810 - Working With A REALTOR®Документ1 страница(Ontario) 810 - Working With A REALTOR®hkhalsaОценок пока нет

- Toxic Document Fallout 10-12-10Документ14 страницToxic Document Fallout 10-12-10Richard Franklin KesslerОценок пока нет

- Buyer AdvisoryДокумент11 страницBuyer AdvisoryThe Lucas GroupОценок пока нет

- California Contract LawДокумент32 страницыCalifornia Contract LawShelley YeamanОценок пока нет

- 2017 Legal Pulse First Quarter 2017 Newsletter 6-20-2017Документ19 страниц2017 Legal Pulse First Quarter 2017 Newsletter 6-20-2017National Association of REALTORS®Оценок пока нет

- REMIC AND UCC EXPLAINED BY Plus NotesДокумент66 страницREMIC AND UCC EXPLAINED BY Plus Notesfgtrulin100% (9)

- Buy The HouseДокумент9 страницBuy The HouseAnthony Juice Gaston Bey100% (4)

- Cash For KeysДокумент5 страницCash For KeysRamin OstowariОценок пока нет

- Inbound 7520803205202771696Документ9 страницInbound 7520803205202771696Aprilyn Montilla LaynoОценок пока нет

- ECF No. 1, Class Action Complaint 3.6.19Документ30 страницECF No. 1, Class Action Complaint 3.6.19Bethany EricksonОценок пока нет

- Insurance Law-IntermediariesДокумент12 страницInsurance Law-IntermediariesDavid FongОценок пока нет

- Broker Dealers Market Makers and Fiduciary DutiesДокумент20 страницBroker Dealers Market Makers and Fiduciary DutiesghalibОценок пока нет

- NY Business Law Journal - Atty. Wallshein Article On Advanced Standing Issues in Securitized MortgagesДокумент8 страницNY Business Law Journal - Atty. Wallshein Article On Advanced Standing Issues in Securitized Mortgages83jjmackОценок пока нет

- Petitioner Respondents Agcaoili & Associates Valenzuela Law Center, Victor Fernandez Ramon M. GuevaraДокумент15 страницPetitioner Respondents Agcaoili & Associates Valenzuela Law Center, Victor Fernandez Ramon M. GuevaraLiene Lalu NadongaОценок пока нет

- Secured Guaranties and Third Party Deeds of Trust 2010Документ13 страницSecured Guaranties and Third Party Deeds of Trust 2010mtandrewОценок пока нет

- My Home Is Mine PDFДокумент36 страницMy Home Is Mine PDFRoger Christensen100% (7)

- Commercial Agency and Distribution AgreementДокумент22 страницыCommercial Agency and Distribution AgreementMenna ElabdeenyОценок пока нет

- L3309 - Lesson 3 - Types of AgentsДокумент7 страницL3309 - Lesson 3 - Types of AgentsConnieОценок пока нет

- What Will A Trustee's Deed Tell?Документ3 страницыWhat Will A Trustee's Deed Tell?Billy BowlesОценок пока нет

- NY Disclosure Form For Buyer and Seller BuyerДокумент2 страницыNY Disclosure Form For Buyer and Seller BuyerPhillip KingОценок пока нет

- Home Buyers GuideДокумент16 страницHome Buyers GuideShafeek AbooubakerОценок пока нет

- MO DisclosureДокумент2 страницыMO DisclosureJay VoglerОценок пока нет

- Moorish Republic Trust: The Official Website of TheДокумент3 страницыMoorish Republic Trust: The Official Website of Thescribd6099Оценок пока нет

- Writ of Mandamus vs. Ohio Department of InsuranceДокумент23 страницыWrit of Mandamus vs. Ohio Department of InsuranceOAITA100% (3)

- Colorado CourtДокумент14 страницColorado CourtheatherОценок пока нет

- Buyer Advisory: Arizona Department of Real EstateДокумент9 страницBuyer Advisory: Arizona Department of Real EstateJacqueline JensenОценок пока нет

- Monmouth-Ocean NJ MLS Listing Agreement Multiple Documents-6Документ4 страницыMonmouth-Ocean NJ MLS Listing Agreement Multiple Documents-6geoscrbdОценок пока нет

- Distance Learning CenterДокумент12 страницDistance Learning CenterYagana Ifeoma bukarОценок пока нет

- Zillow Suit VHTДокумент89 страницZillow Suit VHTJohn CookОценок пока нет

- Data Sharing Dilemmas CCRE WhitepaperДокумент24 страницыData Sharing Dilemmas CCRE WhitepaperAmber TaufenОценок пока нет

- Mega Camp 2015 - Market Update - MykwДокумент31 страницаMega Camp 2015 - Market Update - MykwAmber TaufenОценок пока нет

- Denial of Third-Party Discovery Requests in Move Inc./Zillow LawsuitДокумент4 страницыDenial of Third-Party Discovery Requests in Move Inc./Zillow LawsuitAmber TaufenОценок пока нет

- Declarationjlovejoy 040715Документ184 страницыDeclarationjlovejoy 040715Amber TaufenОценок пока нет

- Pending Home SalesДокумент2 страницыPending Home SalesAmber TaufenОценок пока нет

- Chris Crocker Declaration in Zillow Group/Move Inc. SuitДокумент4 страницыChris Crocker Declaration in Zillow Group/Move Inc. SuitAmber TaufenОценок пока нет

- Objection OppositionДокумент11 страницObjection OppositionbelrilОценок пока нет

- Social Agent RecruitingPresentation 11-17-14-2Документ14 страницSocial Agent RecruitingPresentation 11-17-14-2Amber TaufenОценок пока нет

- Social Agent RecruitingPresentation 11-17-14-2Документ14 страницSocial Agent RecruitingPresentation 11-17-14-2Amber TaufenОценок пока нет

- Filed: (Motion To Shorten Time Pending)Документ17 страницFiled: (Motion To Shorten Time Pending)Amber TaufenОценок пока нет

- Declaration of Singer 041015Документ7 страницDeclaration of Singer 041015Amber TaufenОценок пока нет

- Declaration of Singer 041015Документ7 страницDeclaration of Singer 041015Amber TaufenОценок пока нет

- Quieting TitleДокумент4 страницыQuieting TitleRemar ElumbaringОценок пока нет

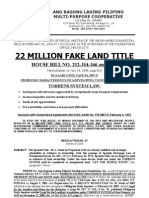

- House Bill No. 212-314-346 and 2702 (22 Million Fake Land Title)Документ6 страницHouse Bill No. 212-314-346 and 2702 (22 Million Fake Land Title)Engr. Stanlymer Mulet100% (2)

- Airbnb Ordinance LawsuitДокумент73 страницыAirbnb Ordinance LawsuitAnonymous 6f8RIS6Оценок пока нет

- Acebedo Vs AbesamisДокумент1 страницаAcebedo Vs AbesamisIvy ColiliОценок пока нет

- P.w.d.handbook Chapter-37 Part-II-Valuation N.v.merani 1980Документ58 страницP.w.d.handbook Chapter-37 Part-II-Valuation N.v.merani 1980Rahul Mahadik100% (3)

- Special Proceedings Rules 72 - 109Документ119 страницSpecial Proceedings Rules 72 - 10919950323Оценок пока нет

- HPBS DSN Sub J0436 3942 0Документ2 страницыHPBS DSN Sub J0436 3942 0otoumsuhib_973854071Оценок пока нет

- Deed of Extrajudicial SettlementДокумент5 страницDeed of Extrajudicial SettlementConrad BrionesОценок пока нет

- Videoke Rental Agreement.07.18.2021Документ2 страницыVideoke Rental Agreement.07.18.2021Maycee Palencia100% (2)

- Final Fairbnb-Update-Report Jan 9 2019Документ10 страницFinal Fairbnb-Update-Report Jan 9 2019eq2 securityОценок пока нет

- SLEM Proposed Policy On Collateral For Salary-Based LoansДокумент4 страницыSLEM Proposed Policy On Collateral For Salary-Based LoansMoira Enegue AbenioОценок пока нет

- Franks Qual 2021Документ8 страницFranks Qual 2021Frank GregoireОценок пока нет

- Rem2 Notes SpecProДокумент22 страницыRem2 Notes SpecProCrnc NavidadОценок пока нет

- Estate Tax: Feria and La O For Appellants. Attorney-General Jaranilla For AppelleeДокумент26 страницEstate Tax: Feria and La O For Appellants. Attorney-General Jaranilla For AppelleeLyssa TabbuОценок пока нет

- UNIT 10.property LawДокумент31 страницаUNIT 10.property Lawanhlh09.ipcОценок пока нет

- Tatvam Villas BrochureДокумент16 страницTatvam Villas BrochureSunil SheoranОценок пока нет

- Family LawДокумент10 страницFamily LawAiman Kulsoom RizviОценок пока нет

- January 2012 Real Estate On Nova Scotia's South ShoreДокумент152 страницыJanuary 2012 Real Estate On Nova Scotia's South ShoreNancy BainОценок пока нет

- Legal Forms - GNДокумент85 страницLegal Forms - GNPau Teh100% (2)

- Residential House Lease Agreement: 1. Parties 1.1. TenantsДокумент3 страницыResidential House Lease Agreement: 1. Parties 1.1. TenantsSajith PrasangaОценок пока нет

- Property Law 2 ProjectДокумент16 страницProperty Law 2 ProjectSandeep Choudhary100% (1)

- Legal Notice-The WireДокумент17 страницLegal Notice-The WireThe Wire100% (1)

- 4 Ways To Avoid Probate - Wikihow PDFДокумент6 страниц4 Ways To Avoid Probate - Wikihow PDFMISTAcareОценок пока нет

- Lease Agreement - TemplateДокумент9 страницLease Agreement - TemplateDonald T. GrahnОценок пока нет

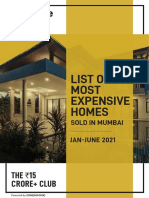

- List of Most Expensive Homes: THE 15 Crore+ ClubДокумент15 страницList of Most Expensive Homes: THE 15 Crore+ ClubHarsh ShahОценок пока нет

- A Guide To The Maharashtra Stamp Duty ActДокумент8 страницA Guide To The Maharashtra Stamp Duty ActRohit ChhajedОценок пока нет

- Nism 5 A - Mutual Fund Exam - Real Feel Mock Test PDFДокумент54 страницыNism 5 A - Mutual Fund Exam - Real Feel Mock Test PDFAnand Gandhi33% (3)

- Orion Savings Bank V Suzuki 740 SCRA 345Документ23 страницыOrion Savings Bank V Suzuki 740 SCRA 345jan lorenzoОценок пока нет

- Iii. RULE 1, Sections 1 To 6, ROCДокумент57 страницIii. RULE 1, Sections 1 To 6, ROCRabelais MedinaОценок пока нет

- Tenancy Agreement (Template)Документ9 страницTenancy Agreement (Template)Kok Keong TanОценок пока нет

- Learn the Essentials of Business Law in 15 DaysОт EverandLearn the Essentials of Business Law in 15 DaysРейтинг: 4 из 5 звезд4/5 (13)

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingОт EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingРейтинг: 4.5 из 5 звезд4.5/5 (98)

- Buffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorОт EverandBuffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorРейтинг: 4.5 из 5 звезд4.5/5 (132)

- Law of Leverage: The Key to Exponential WealthОт EverandLaw of Leverage: The Key to Exponential WealthРейтинг: 4.5 из 5 звезд4.5/5 (6)

- Introduction to Negotiable Instruments: As per Indian LawsОт EverandIntroduction to Negotiable Instruments: As per Indian LawsРейтинг: 5 из 5 звезд5/5 (1)

- Getting Through: Cold Calling Techniques To Get Your Foot In The DoorОт EverandGetting Through: Cold Calling Techniques To Get Your Foot In The DoorРейтинг: 4.5 из 5 звезд4.5/5 (63)

- AI For Lawyers: How Artificial Intelligence is Adding Value, Amplifying Expertise, and Transforming CareersОт EverandAI For Lawyers: How Artificial Intelligence is Adding Value, Amplifying Expertise, and Transforming CareersОценок пока нет

- Disloyal: A Memoir: The True Story of the Former Personal Attorney to President Donald J. TrumpОт EverandDisloyal: A Memoir: The True Story of the Former Personal Attorney to President Donald J. TrumpРейтинг: 4 из 5 звезд4/5 (215)

- Secrecy World: Inside the Panama Papers Investigation of Illicit Money Networks and the Global EliteОт EverandSecrecy World: Inside the Panama Papers Investigation of Illicit Money Networks and the Global EliteРейтинг: 4.5 из 5 звезд4.5/5 (6)

- Wall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementОт EverandWall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementРейтинг: 4.5 из 5 звезд4.5/5 (20)

- The Startup Visa: U.S. Immigration Visa Guide for Startups and FoundersОт EverandThe Startup Visa: U.S. Immigration Visa Guide for Startups and FoundersОценок пока нет

- California Employment Law: An Employer's Guide: Revised and Updated for 2024От EverandCalifornia Employment Law: An Employer's Guide: Revised and Updated for 2024Оценок пока нет

- The Motley Fool's Rule Makers, Rule Breakers: The Foolish Guide to Picking StocksОт EverandThe Motley Fool's Rule Makers, Rule Breakers: The Foolish Guide to Picking StocksРейтинг: 4 из 5 звезд4/5 (3)

- The SHRM Essential Guide to Employment Law, Second Edition: A Handbook for HR Professionals, Managers, Businesses, and OrganizationsОт EverandThe SHRM Essential Guide to Employment Law, Second Edition: A Handbook for HR Professionals, Managers, Businesses, and OrganizationsОценок пока нет

- Nolo's Quick LLC: All You Need to Know About Limited Liability CompaniesОт EverandNolo's Quick LLC: All You Need to Know About Limited Liability CompaniesРейтинг: 4.5 из 5 звезд4.5/5 (7)

- International Business Law: Cases and MaterialsОт EverandInternational Business Law: Cases and MaterialsРейтинг: 5 из 5 звезд5/5 (1)

- Eagle on the Street: The SEC and Wall Street during the Reagan YearsОт EverandEagle on the Street: The SEC and Wall Street during the Reagan YearsРейтинг: 5 из 5 звезд5/5 (1)

- The Chickenshit Club: Why the Justice Department Fails to Prosecute ExecutivesWhite Collar CriminalsОт EverandThe Chickenshit Club: Why the Justice Department Fails to Prosecute ExecutivesWhite Collar CriminalsРейтинг: 5 из 5 звезд5/5 (24)

- Contract Law in America: A Social and Economic Case StudyОт EverandContract Law in America: A Social and Economic Case StudyОценок пока нет

- New York Management Law: The Practical Guide to Employment Law for Business Owners and ManagersОт EverandNew York Management Law: The Practical Guide to Employment Law for Business Owners and ManagersОценок пока нет