Вам также может понравиться

- A 133 Year Lesson On How To Prepare For The Current Bull MarketДокумент4 страницыA 133 Year Lesson On How To Prepare For The Current Bull MarketDeepal DhamejaОценок пока нет

- Monthly Unit Generation Report 2013-2016Документ2 страницыMonthly Unit Generation Report 2013-2016Deepal DhamejaОценок пока нет

- Basic Fundamental AnalysisДокумент5 страницBasic Fundamental AnalysisDeepal DhamejaОценок пока нет

- A Detailed Analysis Into The Fundamental Factors Affecting Crude Oil Prices 12-02-141Документ12 страницA Detailed Analysis Into The Fundamental Factors Affecting Crude Oil Prices 12-02-141Deepal DhamejaОценок пока нет

- 10 MW Thermal EnergyДокумент3 страницы10 MW Thermal EnergyDeepal DhamejaОценок пока нет

- Account Closure Form PDFДокумент1 страницаAccount Closure Form PDFDeepal DhamejaОценок пока нет

- Crude Oil and Gasoline Price MonitoringДокумент23 страницыCrude Oil and Gasoline Price MonitoringDeepal DhamejaОценок пока нет

- Durga Maa Names MeaningДокумент1 страницаDurga Maa Names MeaningDeepal DhamejaОценок пока нет

- DForm AДокумент24 страницыDForm ADeepal DhamejaОценок пока нет

- MCXDailyMargin Jan292016Документ3 страницыMCXDailyMargin Jan292016NikiDhamejaОценок пока нет

- Manish TallyДокумент6 страницManish TallyDeepal DhamejaОценок пока нет

- Trading 101 BasicsДокумент3 страницыTrading 101 BasicsNaveen KumarОценок пока нет

- Tech AnalДокумент64 страницыTech Analjvinod2025Оценок пока нет

- Daily Commodity Report 22-DEC-2015Документ8 страницDaily Commodity Report 22-DEC-2015Deepal DhamejaОценок пока нет

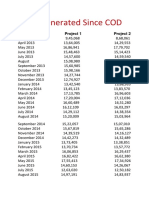

- Units Generated Since COD PDFДокумент2 страницыUnits Generated Since COD PDFDeepal DhamejaОценок пока нет

- 32535rtp May14 Ipcc-P7Документ38 страниц32535rtp May14 Ipcc-P7Hitesh ChintuОценок пока нет

- Client Income Declaration FormДокумент1 страницаClient Income Declaration FormDeepal DhamejaОценок пока нет

- Affidavit: (Before Me The Executive Magistrate Dist Thane)Документ1 страницаAffidavit: (Before Me The Executive Magistrate Dist Thane)Deepal DhamejaОценок пока нет

- List of Useful Codes With Descriptions To Be Used As Reference Status of TaxpayerДокумент5 страницList of Useful Codes With Descriptions To Be Used As Reference Status of TaxpayerJayОценок пока нет

- Vipassana PDF ManualДокумент4 страницыVipassana PDF ManualbenjaminzenkОценок пока нет

- MP Certificate for PAN CardДокумент1 страницаMP Certificate for PAN CardreddygrОценок пока нет

- 21911rtp May11 PCC 2Документ34 страницы21911rtp May11 PCC 2Deepal DhamejaОценок пока нет

- 21931nc PCCДокумент6 страниц21931nc PCCDeepal DhamejaОценок пока нет

- 18626pcc Compsuggans 6AIT Cp4Документ5 страниц18626pcc Compsuggans 6AIT Cp4spchheda4996Оценок пока нет

- 18609cp7 PCC Compsuggans TaxationДокумент6 страниц18609cp7 PCC Compsuggans TaxationDeepal DhamejaОценок пока нет

- 18609cp7 PCC Compsuggans TaxationДокумент6 страниц18609cp7 PCC Compsuggans TaxationDeepal DhamejaОценок пока нет

- Corporate AccountingДокумент749 страницCorporate AccountingDr. Mohammad Noor Alam71% (7)

- 22442ittstm U1 cp1Документ12 страниц22442ittstm U1 cp1Deepal DhamejaОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Important Banking abbreviations and their full formsДокумент10 страницImportant Banking abbreviations and their full formsSivaChand DuggiralaОценок пока нет

- PSP Study Guide 224 Q & A Revision Answers OlnyДокумент214 страницPSP Study Guide 224 Q & A Revision Answers OlnyMohyuddin A Maroof100% (1)

- Universidad de Lima Study Session 5 Questions and AnswersДокумент36 страницUniversidad de Lima Study Session 5 Questions and Answersjzedano95Оценок пока нет

- Merchandise Planning: PGDM Iv-7Документ19 страницMerchandise Planning: PGDM Iv-7Rajdeep JainОценок пока нет

- Murphy Et Al v. Kohlberg Kravis Roberts & Company Et Al - Document No. 16Документ15 страницMurphy Et Al v. Kohlberg Kravis Roberts & Company Et Al - Document No. 16Justia.comОценок пока нет

- Ets 2021Документ4 страницыEts 2021Khang PhạmОценок пока нет

- Kalyan Pharma Ltd.Документ33 страницыKalyan Pharma Ltd.Parth V. PurohitОценок пока нет

- IC August 2014Документ68 страницIC August 2014sabah8800Оценок пока нет

- Aarthi Mba Project FinalДокумент20 страницAarthi Mba Project FinalBnaren NarenОценок пока нет

- Ikea 6Документ39 страницIkea 6My PhamОценок пока нет

- Stages in Consumer Decision Making ProcessДокумент19 страницStages in Consumer Decision Making ProcessAnshita GargОценок пока нет

- What Causes Small Businesses To FailДокумент11 страницWhat Causes Small Businesses To Failmounirs719883Оценок пока нет

- Module 6 Legality of A Contract FinalДокумент27 страницModule 6 Legality of A Contract FinalKeshav JatwaniОценок пока нет

- Special Meeting TonightДокумент48 страницSpecial Meeting TonightHOA_Freedom_FighterОценок пока нет

- Odb 3Документ4 страницыOdb 3Onnatan DinkaОценок пока нет

- Role of Business Research ch#1 of Zikmound BookДокумент18 страницRole of Business Research ch#1 of Zikmound Bookzaraa1994100% (1)

- Working Capital Management at BSRM SteelДокумент144 страницыWorking Capital Management at BSRM SteelPushpa Barua100% (1)

- Samsung Care Plus Terms and Conditions PDFДокумент10 страницSamsung Care Plus Terms and Conditions PDFav86Оценок пока нет

- Latest Scheme BrochureДокумент46 страницLatest Scheme Brochurerohit klshaanОценок пока нет

- Tally PPT For Counselling1Документ11 страницTally PPT For Counselling1lekhraj sahuОценок пока нет

- Risk Report: Marriott HotelДокумент19 страницRisk Report: Marriott HotelBao Thy Pho100% (1)

- Convince Converts What Great Brands Do in Content Marketing Ebook PDFДокумент8 страницConvince Converts What Great Brands Do in Content Marketing Ebook PDFA100% (1)

- Schneider EnglishДокумент134 страницыSchneider EnglishpepitoОценок пока нет

- Ghani GlassДокумент75 страницGhani GlassAftabMughal100% (1)

- Kwality WallsДокумент18 страницKwality WallsKanak Gehlot0% (2)

- Bank Companies Act 1991 GuideДокумент16 страницBank Companies Act 1991 GuideismailabtiОценок пока нет

- Section What Is Entrepreneurship? Section Characteristics of An EntrepreneurДокумент12 страницSection What Is Entrepreneurship? Section Characteristics of An EntrepreneurAashir RajputОценок пока нет

- Dominos PizzaДокумент14 страницDominos PizzahemantОценок пока нет

- Vinati Organics Ltd financial analysis and key metrics from 2011 to 2020Документ30 страницVinati Organics Ltd financial analysis and key metrics from 2011 to 2020nhariОценок пока нет

- XUB 3rd Convocation 22nd March2017Документ160 страницXUB 3rd Convocation 22nd March2017Chinmoy BandyopadhyayОценок пока нет