Вам также может понравиться

- Deductions From Gross Total Income: HapterДокумент20 страницDeductions From Gross Total Income: HapterJAWED MOHAMMADОценок пока нет

- CSДокумент26 страницCSAnjuElsaОценок пока нет

- IT Deductions Allowed Under Chapter VI-A Sec 80C, 80CCC, 80CCD, 80D, 80DD, 80DDB Etc - APTEACHERS WebsiteДокумент13 страницIT Deductions Allowed Under Chapter VI-A Sec 80C, 80CCC, 80CCD, 80D, 80DD, 80DDB Etc - APTEACHERS WebsiteKIMS IECОценок пока нет

- Question:-Q Write Note On Deduction U/s 80 C To 80 UДокумент15 страницQuestion:-Q Write Note On Deduction U/s 80 C To 80 UnikhilОценок пока нет

- Direct Taxes Semester 3 Roll No: 19P0310307: Filing Your Income Tax ReturnДокумент5 страницDirect Taxes Semester 3 Roll No: 19P0310307: Filing Your Income Tax ReturnPriya KudnekarОценок пока нет

- NMIMS Global Access School For Continuing Education (NGA-SCE) Course: Taxation-Direct and Indirect Internal Assignment Applicable For June 2020 ExaminationДокумент10 страницNMIMS Global Access School For Continuing Education (NGA-SCE) Course: Taxation-Direct and Indirect Internal Assignment Applicable For June 2020 ExaminationAnkit SharmaОценок пока нет

- Incometax Sections PDFДокумент13 страницIncometax Sections PDFmohanОценок пока нет

- Income Tax NitДокумент6 страницIncome Tax NitrensisamОценок пока нет

- National Institute of Technology CalicutДокумент7 страницNational Institute of Technology CalicutraghuramaОценок пока нет

- Atc AtuДокумент9 страницAtc AtuKeshav SagarОценок пока нет

- General Deductions (Under Section 80) : Basic Rules Governing Deductions Under Sections 80C To 80UДокумент67 страницGeneral Deductions (Under Section 80) : Basic Rules Governing Deductions Under Sections 80C To 80UVENKATESAN DОценок пока нет

- Chapter 12 TaxdeductionsДокумент16 страницChapter 12 TaxdeductionsRiya SharmaОценок пока нет

- Income Tax ProjectДокумент26 страницIncome Tax ProjectVinay KumarОценок пока нет

- Exemptions Under Various Sections of The Income Tax, India: 1) Section 80 C (Limit: Rs. 1,00,000)Документ5 страницExemptions Under Various Sections of The Income Tax, India: 1) Section 80 C (Limit: Rs. 1,00,000)Ramakoteswar NampalliОценок пока нет

- Deductions U/S 80C TO 80U: By: Sumit BediДокумент69 страницDeductions U/S 80C TO 80U: By: Sumit BediKittu NemaniОценок пока нет

- Aditya Sharma - II Mid Term Paper Shikha MamДокумент9 страницAditya Sharma - II Mid Term Paper Shikha MamAditya SharmaОценок пока нет

- DeductionsДокумент11 страницDeductionsguest1Оценок пока нет

- Direct Taxes CircularДокумент34 страницыDirect Taxes CircularratiОценок пока нет

- Taxation Law ProjectДокумент15 страницTaxation Law Projectraj vardhan agarwalОценок пока нет

- MockДокумент18 страницMockSmarty ShivamОценок пока нет

- Handicap Direct Taxes Circular - Sec..Документ2 страницыHandicap Direct Taxes Circular - Sec..Dharmpaji2010Оценок пока нет

- 1 .Income Tax On Salaries - (01.06.2015)Документ57 страниц1 .Income Tax On Salaries - (01.06.2015)yvОценок пока нет

- Investments Considered Under This Section Are: 1. Maximum Limit Rs.150000/-2. Available For Self, Spouse and ChildrenДокумент8 страницInvestments Considered Under This Section Are: 1. Maximum Limit Rs.150000/-2. Available For Self, Spouse and ChildrenGourav BathejaОценок пока нет

- Pressrelease 02012008Документ1 страницаPressrelease 02012008nettmann2001Оценок пока нет

- Deductions Under Chapter VI A of The Income Tax Act, 1961: (Submitted by CA. Jayesh Satish Behede, Jalgaon, Maharashtra)Документ13 страницDeductions Under Chapter VI A of The Income Tax Act, 1961: (Submitted by CA. Jayesh Satish Behede, Jalgaon, Maharashtra)Anfal MoidinОценок пока нет

- 19769ipcc It Vol1 Cp7Документ60 страниц19769ipcc It Vol1 Cp7Joseph SalidoОценок пока нет

- VRS NotesДокумент82 страницыVRS NotesrisingiocmОценок пока нет

- Deductions To Be Made in Computing Total IncomeДокумент15 страницDeductions To Be Made in Computing Total IncomeAbey FrancisОценок пока нет

- Deductions On Section 80CДокумент12 страницDeductions On Section 80CViraja GuruОценок пока нет

- Aditya Sharma - II Mid Term Paper Shikha Mam 1Документ11 страницAditya Sharma - II Mid Term Paper Shikha Mam 1Aditya SharmaОценок пока нет

- Income Tax ActДокумент4 страницыIncome Tax ActgoborgonesОценок пока нет

- Income Tax Section 80Документ19 страницIncome Tax Section 80DEV HUGENОценок пока нет

- 1.7.7.1. Entertainment Allowance (U/s 16 (Ii) ) : 1.7.7. Deduction Out of Gross Salary (Section 16)Документ5 страниц1.7.7.1. Entertainment Allowance (U/s 16 (Ii) ) : 1.7.7. Deduction Out of Gross Salary (Section 16)Vinod PillaiОценок пока нет

- DeductionsДокумент7 страницDeductionsAnurag BishtОценок пока нет

- Income Tax Rate 2010Документ6 страницIncome Tax Rate 2010Vishal JwellОценок пока нет

- Deduction U/s 80D MediclaimДокумент3 страницыDeduction U/s 80D MediclaimVijayaraj KvrОценок пока нет

- Preparation &Submission-ITR-I-June-16Документ7 страницPreparation &Submission-ITR-I-June-16আদি ত্যОценок пока нет

- Tax AmendmentДокумент10 страницTax AmendmentVinay BoradОценок пока нет

- Investment Declaration Form (Hemarus)Документ4 страницыInvestment Declaration Form (Hemarus)Shashi NaganurОценок пока нет

- Instructions For Filling Out FORM ITR-2: Page 1 of 10Документ10 страницInstructions For Filling Out FORM ITR-2: Page 1 of 10mehtakvijayОценок пока нет

- Tax DeductionДокумент20 страницTax DeductionTushar JoshiОценок пока нет

- Taxation (Nov. 2007)Документ17 страницTaxation (Nov. 2007)P VenkatesanОценок пока нет

- It ClarificationДокумент1 страницаIt ClarificationTNGTFОценок пока нет

- Bilaspur ChapterДокумент96 страницBilaspur ChapterYash SharmaОценок пока нет

- Instructions For Filling Out FORM ITR-2Документ7 страницInstructions For Filling Out FORM ITR-2Harminder Singh DhamОценок пока нет

- On Deductions Under Section 80C To 80U (Unit - 4) Bcom 6 SEMДокумент11 страницOn Deductions Under Section 80C To 80U (Unit - 4) Bcom 6 SEMMudasir LoneОценок пока нет

- The Following Clause 10 (D) of Section 10 by The Finance Act, 2003, W.E.F. 1-4-2004Документ10 страницThe Following Clause 10 (D) of Section 10 by The Finance Act, 2003, W.E.F. 1-4-2004120133Оценок пока нет

- DeductionsДокумент7 страницDeductionsManjeet KaurОценок пока нет

- Sanskar Bangera TCM2223003Документ5 страницSanskar Bangera TCM2223003Sanskar BangeraОценок пока нет

- Budget 2013 - 2014Документ11 страницBudget 2013 - 2014sdfdhgtj894Оценок пока нет

- RMC 27-2011Документ0 страницRMC 27-2011Peggy SalazarОценок пока нет

- Income Tax Guide FY 2023-24Документ11 страницIncome Tax Guide FY 2023-24akshay yadavОценок пока нет

- ASSESSMENT YEAR 2014 Tax Rates and DetailsДокумент6 страницASSESSMENT YEAR 2014 Tax Rates and Detailsamit2201Оценок пока нет

- Section 80CCD (1B) Deduction - About NPS Scheme & Tax BenefitsДокумент7 страницSection 80CCD (1B) Deduction - About NPS Scheme & Tax BenefitsP B ChaudharyОценок пока нет

- Taxation Direct and IndirectДокумент6 страницTaxation Direct and Indirectdivyakashyapbharat1Оценок пока нет

- Personal Income Tax Under The New Regime and Old RegimeДокумент4 страницыPersonal Income Tax Under The New Regime and Old RegimeAiswarya BОценок пока нет

- Income Which Do Not Form Part of Total Income: HapterДокумент33 страницыIncome Which Do Not Form Part of Total Income: HapterAleti NithishОценок пока нет

- IT Declaration Form Revised SalaryДокумент1 страницаIT Declaration Form Revised SalaryMANUBHOPALОценок пока нет

- Unit 5Документ9 страницUnit 5piyush.birru25Оценок пока нет

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisОт EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisОценок пока нет

- Basic Fundamental AnalysisДокумент5 страницBasic Fundamental AnalysisDeepal DhamejaОценок пока нет

- Daily Commodity Report 22-DEC-2015Документ8 страницDaily Commodity Report 22-DEC-2015Deepal DhamejaОценок пока нет

- Account Closure Form PDFДокумент1 страницаAccount Closure Form PDFDeepal DhamejaОценок пока нет

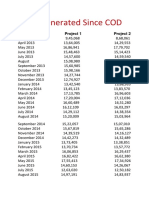

- Units Generated Since CODДокумент2 страницыUnits Generated Since CODDeepal DhamejaОценок пока нет

- 10 MW Thermal EnergyДокумент3 страницы10 MW Thermal EnergyDeepal DhamejaОценок пока нет

- Affidavit: (Before Me The Executive Magistrate Dist Thane)Документ1 страницаAffidavit: (Before Me The Executive Magistrate Dist Thane)Deepal DhamejaОценок пока нет

- (To Be Submitted in Duplicate) : Details of First / Sole HolderДокумент1 страница(To Be Submitted in Duplicate) : Details of First / Sole HolderDeepal DhamejaОценок пока нет

- 35 Ipcc Accounting Practice ManualДокумент218 страниц35 Ipcc Accounting Practice ManualDeepal Dhameja100% (6)

- Nestle SpeechДокумент3 страницыNestle Speechkapil chandwaniОценок пока нет

- Chapter 6Документ2 страницыChapter 6Christy Mae EderОценок пока нет

- JPMorgan Chase London Whale HДокумент12 страницJPMorgan Chase London Whale HMaksym ShodaОценок пока нет

- Tax Ordinance-Books 1-30 FCTBДокумент51 страницаTax Ordinance-Books 1-30 FCTBRaiha MoriyomОценок пока нет

- The Advanced Guide To Equity Research Report WritingДокумент23 страницыThe Advanced Guide To Equity Research Report Writingsara_isarОценок пока нет

- BDAДокумент9 страницBDAEmaan SalmanОценок пока нет

- Senka Dindic - CV EnglishДокумент2 страницыSenka Dindic - CV EnglishAntonela ĐinđićОценок пока нет

- Industrial Relations and Labour LawsДокумент229 страницIndustrial Relations and Labour LawsAkash LokhandeОценок пока нет

- EKN224 244 Course Information 2022Документ16 страницEKN224 244 Course Information 2022HappinessОценок пока нет

- MATH Excellence-WPS OfficeДокумент14 страницMATH Excellence-WPS OfficeKyla Joy T. SanchezОценок пока нет

- Commercial Bank Management Midsem NotesДокумент12 страницCommercial Bank Management Midsem NotesWinston WongОценок пока нет

- Human Resource Management: Case Study: 1Документ5 страницHuman Resource Management: Case Study: 1Sailpoint Course0% (1)

- Operations Strategy in A Global Environment: Prof: Dr. Sadam Wedyan Student: AREEJ KHRAIMДокумент19 страницOperations Strategy in A Global Environment: Prof: Dr. Sadam Wedyan Student: AREEJ KHRAIMDania Al-ȜbadiОценок пока нет

- Kami Export - Microsoft Word - Choose To Save Lesson Plan 2 4 1 - Https - Mail-Attachment Googleusercontent Com-Attachment-U-0Документ4 страницыKami Export - Microsoft Word - Choose To Save Lesson Plan 2 4 1 - Https - Mail-Attachment Googleusercontent Com-Attachment-U-0api-296019366Оценок пока нет

- Workforce Utilization and Employment Practices Part - 2Документ13 страницWorkforce Utilization and Employment Practices Part - 2HOD CommerceОценок пока нет

- Hofstede Dimensions of Canada and South KoreaДокумент8 страницHofstede Dimensions of Canada and South KoreaWhileUsleepОценок пока нет

- WEF A Partner in Shaping HistoryДокумент190 страницWEF A Partner in Shaping HistoryAbi SolaresОценок пока нет

- IFRS 9 - Financial InstrumentsДокумент63 страницыIFRS 9 - Financial InstrumentsMonirul Islam MoniirrОценок пока нет

- Tutorial 11Документ4 страницыTutorial 11TING POH YEEОценок пока нет

- SWOT Analysis of ItalyДокумент22 страницыSWOT Analysis of ItalyTarunendra Pratap SinghОценок пока нет

- A Leadership Case Study - How HR Caused Toyota CrashДокумент6 страницA Leadership Case Study - How HR Caused Toyota CrashLminith100% (1)

- Fringe Benefit Tax PDFДокумент9 страницFringe Benefit Tax PDFLorraine TomasОценок пока нет

- The Oriental Express Case StudyДокумент5 страницThe Oriental Express Case Studysehajsomi008Оценок пока нет

- Oracle 11: Drop ShipmentДокумент69 страницOracle 11: Drop ShipmentShivangiSinghMadnaniОценок пока нет

- June Month CalendarДокумент1 страницаJune Month CalendarBABA SIDОценок пока нет

- Icaew Cfab Mi 2018 Sample Exam 3Документ30 страницIcaew Cfab Mi 2018 Sample Exam 3Anonymous ulFku1v100% (2)

- Benefits of Sole PropДокумент12 страницBenefits of Sole PropRisha Mae SalingayОценок пока нет

- Ice Cream Parlor Business Plan TemplateДокумент44 страницыIce Cream Parlor Business Plan TemplateTasnim EdreesОценок пока нет

- Indian Institute of Management Lucknow Post Graduate Programme, 2012-13Документ3 страницыIndian Institute of Management Lucknow Post Graduate Programme, 2012-13Vikas HajelaОценок пока нет

- Agreement FormatДокумент5 страницAgreement Formatpurshottam hunsigiОценок пока нет