Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (120)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Solution: A. Gross Business Income, PhilippinesДокумент9 страницSolution: A. Gross Business Income, Philippineslena cpa78% (9)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Civil Procedure Digest Pre MidtermsДокумент116 страницCivil Procedure Digest Pre Midtermskramsaga100% (1)

- Legal Ethics Cases (Downloaded)Документ72 страницыLegal Ethics Cases (Downloaded)Magazine BoxОценок пока нет

- Popliteus Calcaneus Nasus: in Scientific Terms What Is The Back of Our Knee Called?Документ36 страницPopliteus Calcaneus Nasus: in Scientific Terms What Is The Back of Our Knee Called?Ramon GasgasОценок пока нет

- Oral Com Preliminary TasksДокумент1 страницаOral Com Preliminary TasksRamon GasgasОценок пока нет

- Formal Theme WritingДокумент3 страницыFormal Theme WritingRamon GasgasОценок пока нет

- Cloyd Cases Not Final YetДокумент20 страницCloyd Cases Not Final YetRamon GasgasОценок пока нет

- Brentttt (Please Pa-Print)Документ2 страницыBrentttt (Please Pa-Print)Ramon GasgasОценок пока нет

- Genmath Fa9Документ3 страницыGenmath Fa9Ramon GasgasОценок пока нет

- Cell Theory, Parts and Types of CellsДокумент62 страницыCell Theory, Parts and Types of CellsRamon GasgasОценок пока нет

- Revised Faculty Incentive ProgramДокумент38 страницRevised Faculty Incentive ProgramRamon GasgasОценок пока нет

- Gen Math Problem Set Part 2Документ1 страницаGen Math Problem Set Part 2Ramon GasgasОценок пока нет

- Hand4out On Social EncyclicalsДокумент2 страницыHand4out On Social EncyclicalsRamon GasgasОценок пока нет

- SS 8 1617 Ancient Civilizations Activity SheetДокумент1 страницаSS 8 1617 Ancient Civilizations Activity SheetRamon GasgasОценок пока нет

- Exponents and LogarithmsДокумент56 страницExponents and LogarithmsRamon GasgasОценок пока нет

- Absentee Formative Assessment 1Документ4 страницыAbsentee Formative Assessment 1Ramon GasgasОценок пока нет

- God and Evil IIДокумент45 страницGod and Evil IIRamon GasgasОценок пока нет

- Gen Math Problem Set Part 2Документ1 страницаGen Math Problem Set Part 2Ramon GasgasОценок пока нет

- For Program LaterДокумент4 страницыFor Program LaterRamon GasgasОценок пока нет

- ENG 10 Revised NextGen Blended LM T1 15-16Документ14 страницENG 10 Revised NextGen Blended LM T1 15-16Ramon GasgasОценок пока нет

- TleДокумент2 страницыTleRamon GasgasОценок пока нет

- High School English Faculty: TRACK: Academic Strand: Core GRADE: 11 ACADEMIC YEAR: 2016-2017Документ12 страницHigh School English Faculty: TRACK: Academic Strand: Core GRADE: 11 ACADEMIC YEAR: 2016-2017Ramon Gasgas100% (1)

- Process A. ARRANGING REAL NUMBERS. Arrange The Following Real Numbers in Descending Order. WriteДокумент3 страницыProcess A. ARRANGING REAL NUMBERS. Arrange The Following Real Numbers in Descending Order. WriteRamon GasgasОценок пока нет

- Figurative LanguageДокумент39 страницFigurative LanguageRamon GasgasОценок пока нет

- Debate MindДокумент4 страницыDebate MindRamon GasgasОценок пока нет

- Alphabet of LinesДокумент20 страницAlphabet of LinesJoseph GanОценок пока нет

- Experiment 2.1 Periodic TrendsДокумент2 страницыExperiment 2.1 Periodic TrendsRamon GasgasОценок пока нет

- Presentargtion Figurative Vs Literal LanguageДокумент13 страницPresentargtion Figurative Vs Literal LanguageRamon GasgasОценок пока нет

- What Is Christian MoralityДокумент21 страницаWhat Is Christian MoralityRamon GasgasОценок пока нет

- Seven Major Themes In: Catholic Social TeachingДокумент21 страницаSeven Major Themes In: Catholic Social TeachingRamon GasgasОценок пока нет

- Seven Major Themes In: Catholic Social TeachingДокумент21 страницаSeven Major Themes In: Catholic Social TeachingRamon GasgasОценок пока нет

- 01 Leverages FTДокумент7 страниц01 Leverages FT1038 Kareena SoodОценок пока нет

- Income Taxation - Finals QuizzesДокумент12 страницIncome Taxation - Finals QuizzesJalyn Jalando-onОценок пока нет

- Jse Module5 Ae25 BTДокумент13 страницJse Module5 Ae25 BTTrisha Anne VenturaОценок пока нет

- Tax Review 194RДокумент4 страницыTax Review 194RDheeraj YadavОценок пока нет

- Chapter04.Personal ClaimsДокумент181 страницаChapter04.Personal Claimsmpradip1975Оценок пока нет

- UPES Admission ProcessДокумент5 страницUPES Admission ProcessSandeep ChoudhuryОценок пока нет

- Chapter 5 - Coporation Income TaxДокумент17 страницChapter 5 - Coporation Income TaxTiến TrươngОценок пока нет

- Solution Manual For Income Tax Fundamentals 2015 33rd Edition Gerald e Whittenburg Martha Altus Buller Steven GillДокумент34 страницыSolution Manual For Income Tax Fundamentals 2015 33rd Edition Gerald e Whittenburg Martha Altus Buller Steven Gillfavastassel82y30100% (38)

- Multiple Choice QuestionsДокумент17 страницMultiple Choice QuestionsTaha Wael QandeelОценок пока нет

- 2551Q Jan 2018 ENCS Final Rev 3Документ2 страницы2551Q Jan 2018 ENCS Final Rev 3MIS MijerssОценок пока нет

- Investment and Incentives LawДокумент219 страницInvestment and Incentives LawBechay PallasigueОценок пока нет

- Court Appeals: Blic of The Philippines of Tax Quezon CityДокумент34 страницыCourt Appeals: Blic of The Philippines of Tax Quezon CityYna YnaОценок пока нет

- Nepal Budget Highlights - 79-80 - APM & AssociatesДокумент89 страницNepal Budget Highlights - 79-80 - APM & Associatesaasthapoddar155Оценок пока нет

- Land Acquisitio - Group 2Документ7 страницLand Acquisitio - Group 2SNEHITHA SUNKARAPALLIОценок пока нет

- No 5Документ4 страницыNo 5Barbara IgnacioОценок пока нет

- Cia15 Study Guide 4 Bac 103 Taxation Income Taxation SfernandoДокумент23 страницыCia15 Study Guide 4 Bac 103 Taxation Income Taxation Sfernando5555-899341Оценок пока нет

- Tax Rev. Outline CompilationДокумент23 страницыTax Rev. Outline CompilationMichael James Madrid MalinginОценок пока нет

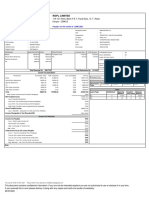

- RSPL Limited: Payslip For The Month of JUNE 2021Документ1 страницаRSPL Limited: Payslip For The Month of JUNE 2021Manju ManjappaОценок пока нет

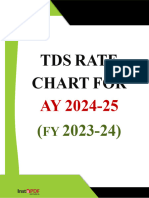

- Instapdf - in Tds Rate Chart Fy 2023 24 Ay 2024 25 355Документ7 страницInstapdf - in Tds Rate Chart Fy 2023 24 Ay 2024 25 355skassociatetaxconsultantОценок пока нет

- Income From House Property Notes For CA CSCMA StudentsДокумент28 страницIncome From House Property Notes For CA CSCMA StudentsSantosh Chavan100% (1)

- Chapter 10Документ4 страницыChapter 10Judith Salome Basquinas0% (1)

- Afisco Insurance Corporation vs. Court of Appeals 302 SCRA 1, January 25, 1999Документ21 страницаAfisco Insurance Corporation vs. Court of Appeals 302 SCRA 1, January 25, 1999Xtine CampuPotОценок пока нет

- China Rail Cons - 2012 Annual Results Announcement PDFДокумент359 страницChina Rail Cons - 2012 Annual Results Announcement PDFalan888Оценок пока нет

- RR 12-01Документ6 страницRR 12-01matinikkiОценок пока нет

- Income Taxation On IndividualsДокумент18 страницIncome Taxation On IndividualsCindy Felipe100% (1)

- CIR V CTA Smith Kilne & Fresh OverseasДокумент2 страницыCIR V CTA Smith Kilne & Fresh OverseasGRОценок пока нет

- BIR Ruling No. 317-18 (BVI Law)Документ3 страницыBIR Ruling No. 317-18 (BVI Law)LizОценок пока нет

- Top Ten States With The Lowest Tax BurdenДокумент3 страницыTop Ten States With The Lowest Tax BurdenAndreea Anamaria WОценок пока нет

- Golpo 10 Task Performance 1.taxationДокумент13 страницGolpo 10 Task Performance 1.taxationNin JahОценок пока нет