Вам также может понравиться

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Outbound Regular InvoiceДокумент4 страницыOutbound Regular InvoiceSaruwatari MichiyoОценок пока нет

- TML-PSC-SQ Manufacturing Site Assessment Rev 2.0Документ24 страницыTML-PSC-SQ Manufacturing Site Assessment Rev 2.0Narendran MОценок пока нет

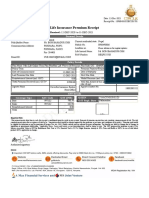

- Life Insurance Premium Receipt: Personal DetailsДокумент1 страницаLife Insurance Premium Receipt: Personal Detailschanam bedantaОценок пока нет

- Notes in Preferential TaxationДокумент57 страницNotes in Preferential TaxationJeremae Ann Ceriaco100% (1)

- Original Invoice: IDCIA087226Документ1 страницаOriginal Invoice: IDCIA087226ASC Tempest-128Оценок пока нет

- VAT in General - CIR V Magsaysay 146984Документ2 страницыVAT in General - CIR V Magsaysay 146984Christine Gel MadrilejoОценок пока нет

- Hlurb Position Paper (Sample)Документ10 страницHlurb Position Paper (Sample)ChesterDiego100% (10)

- Sop in Jail Search For VisitorsДокумент11 страницSop in Jail Search For Visitorsloveset08Оценок пока нет

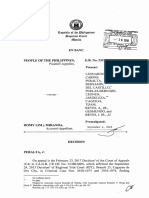

- Supreme Court upholds conviction of man for illegal drug possession and saleДокумент18 страницSupreme Court upholds conviction of man for illegal drug possession and saleMogsy Pernez100% (2)

- Formal-Offer Rule JURISДокумент1 страницаFormal-Offer Rule JURISChesterDiego100% (1)

- Federalism PDFДокумент29 страницFederalism PDFChesterDiegoОценок пока нет

- FederalismДокумент14 страницFederalismChesterDiegoОценок пока нет

- Bibingka RecipeДокумент2 страницыBibingka RecipeChesterDiego100% (1)

- OUTPUT VAT: ZERO RATED SALES GUIDEДокумент12 страницOUTPUT VAT: ZERO RATED SALES GUIDEA cОценок пока нет

- Syllabus of 3 Years LLBДокумент72 страницыSyllabus of 3 Years LLBanniee1993Оценок пока нет

- (Revised) Post Uplb S 046 13 Nanotech RevДокумент50 страниц(Revised) Post Uplb S 046 13 Nanotech RevGladys Bernabe de VeraОценок пока нет

- VNM48Документ205 страницVNM48hddkickОценок пока нет

- ML Aggarwal I S Chawla J Agarwal Munish Sethi Ravinder Singh - Self-Help To ICSE Class 10 X Understanding Mathematics Solutions of ML Aggarwal I S Chawla J Agarwal Munish Sethi Ravinder Singh and SonsДокумент692 страницыML Aggarwal I S Chawla J Agarwal Munish Sethi Ravinder Singh - Self-Help To ICSE Class 10 X Understanding Mathematics Solutions of ML Aggarwal I S Chawla J Agarwal Munish Sethi Ravinder Singh and SonsUtkarsh JainОценок пока нет

- 2306Документ2 страницы2306Anonymous e1WB7mAVJОценок пока нет

- Who May Claim For Refund - Apply For Issuance of Tax Credit CertificateДокумент7 страницWho May Claim For Refund - Apply For Issuance of Tax Credit CertificateyanyanersОценок пока нет

- PC Jeweller Motilal Oswal ICДокумент40 страницPC Jeweller Motilal Oswal ICvbsreddyОценок пока нет

- Taxability of Joint Development Agreement It GSTДокумент14 страницTaxability of Joint Development Agreement It GSTJay SorathiyaОценок пока нет

- Assessment and Appeal Under GSTДокумент19 страницAssessment and Appeal Under GSTGAMING WITH MADHURОценок пока нет

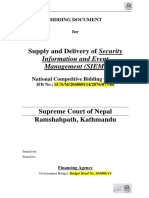

- Supply and Delivery of Security: Information and Event Management (SIEM)Документ83 страницыSupply and Delivery of Security: Information and Event Management (SIEM)lkted100% (1)

- Materials Management Manual: A GuideДокумент204 страницыMaterials Management Manual: A GuidesagarthegameОценок пока нет

- Tanzania Revenue AuthorityДокумент8 страницTanzania Revenue AuthorityIsmail MesayaОценок пока нет

- Tax rules for rental properties and holiday homesДокумент41 страницаTax rules for rental properties and holiday homesRoger DaltryОценок пока нет

- Investment Guide BOIДокумент64 страницыInvestment Guide BOIMansoor Ul Hassan SiddiquiОценок пока нет

- DIFFICULTДокумент3 страницыDIFFICULTClyde RamosОценок пока нет

- Fly Ash Work OrderДокумент2 страницыFly Ash Work OrderSRK QSОценок пока нет

- Field Training Report 127411Документ7 страницField Training Report 127411deepak mauryaОценок пока нет

- Tax Evasion in Bangladesh Assignment Analyzes Causes and ImpactsДокумент10 страницTax Evasion in Bangladesh Assignment Analyzes Causes and Impactscuteraha0% (1)

- 14 Hand Pump Spares List From BIS PDFДокумент125 страниц14 Hand Pump Spares List From BIS PDFNaresh Babu MuddamsettiОценок пока нет

- Schlafhorst Texlab: Catalogue of ServicesДокумент27 страницSchlafhorst Texlab: Catalogue of ServicesvenkatspinnerОценок пока нет

- TranslayteДокумент2 страницыTranslayteambaki1234Оценок пока нет

- CDIC Write-UpДокумент5 страницCDIC Write-UpVixen Aaron EnriquezОценок пока нет

- Mitigation ProjectДокумент12 страницMitigation ProjectMegha DalmiaОценок пока нет