Вам также может понравиться

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeОт Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeРейтинг: 1 из 5 звезд1/5 (1)

- Quiz TaxДокумент5 страницQuiz TaxRaven DahlenОценок пока нет

- F 941Документ4 страницыF 941gopaljiiОценок пока нет

- Tax p2 - Optional Standard DeductionДокумент16 страницTax p2 - Optional Standard DeductionMa. Elene MagdaraogОценок пока нет

- Taxation Law Bar Exam Questions 2011 AnswersДокумент14 страницTaxation Law Bar Exam Questions 2011 AnswersYochabel Eureca BorjeОценок пока нет

- CIR Vs Cebu Toyo CorporationДокумент2 страницыCIR Vs Cebu Toyo Corporationjancelmido1100% (2)

- Taxation Law Review Cases Digest IIДокумент34 страницыTaxation Law Review Cases Digest IIJohney DoeОценок пока нет

- Tax Amnesty Doctrines in Taxation DigestДокумент9 страницTax Amnesty Doctrines in Taxation DigestJuralexОценок пока нет

- Taxation Law BarДокумент12 страницTaxation Law BarJames DecolongonОценок пока нет

- 2021 Tax Review ExercisesДокумент14 страниц2021 Tax Review Exercisesgerald manog100% (1)

- Taxation Law 2017 Bar QuestionsДокумент6 страницTaxation Law 2017 Bar QuestionsBayan Ng RamonОценок пока нет

- CIR Vs Pineda DigestДокумент1 страницаCIR Vs Pineda DigestRoz Lourdiz CamachoОценок пока нет

- Tambunting PawnshopДокумент8 страницTambunting PawnshopNika RojasОценок пока нет

- 2017 Bar Exams Questions in Taxation LawДокумент7 страниц2017 Bar Exams Questions in Taxation LawJade Marlu DelaTorre100% (1)

- Taxation DigestsДокумент62 страницыTaxation DigestsPJr MilleteОценок пока нет

- Rohm Apollo v. CIRДокумент3 страницыRohm Apollo v. CIRGelaine MarananОценок пока нет

- CHUA Vs Absolute Management CorpДокумент3 страницыCHUA Vs Absolute Management CorpMsIc GabrielОценок пока нет

- CHUA Vs Absolute Management CorpДокумент3 страницыCHUA Vs Absolute Management CorpMsIc GabrielОценок пока нет

- CHUA Vs Absolute Management CorpДокумент3 страницыCHUA Vs Absolute Management CorpMsIc GabrielОценок пока нет

- ITR Acknowledgement T Durga PrasadДокумент1 страницаITR Acknowledgement T Durga PrasadEdu KondaluОценок пока нет

- Bar 2018 - MlquДокумент138 страницBar 2018 - MlquTimmy GonzalesОценок пока нет

- 90-15 Filing, Penalties, RemediesДокумент6 страниц90-15 Filing, Penalties, RemediesAljur SalamedaОценок пока нет

- Case Digest Taxation 2Документ50 страницCase Digest Taxation 2Pcl Nueva VizcayaОценок пока нет

- Taxation Law Bar Questions 06-14Документ49 страницTaxation Law Bar Questions 06-14CarmeloОценок пока нет

- Other Percentage TaxesДокумент8 страницOther Percentage TaxesRoxanne PeñaОценок пока нет

- Steag State Power, Inc vs. Commissioner of Internal Revenue FactsДокумент40 страницSteag State Power, Inc vs. Commissioner of Internal Revenue FactsRyannDeLeonОценок пока нет

- ReSA B44 TAX Final PB Exam Questions Answers and SolutionsДокумент14 страницReSA B44 TAX Final PB Exam Questions Answers and SolutionsDhainne EnriquezОценок пока нет

- CIR Vs Aluminum WheelsДокумент3 страницыCIR Vs Aluminum WheelsJenifferRimandoОценок пока нет

- Tax Recit With AnswersДокумент8 страницTax Recit With AnswersEnrique Legaspi IVОценок пока нет

- Velasquez, v. George, Et. Al.Документ1 страницаVelasquez, v. George, Et. Al.MsIc GabrielОценок пока нет

- Tax II Case DigestДокумент9 страницTax II Case DigestCesar P ValeraОценок пока нет

- Macario Lim Gaw, JR., Petitioner, vs. Commissioner OF Internal Revenue, Respondent. Tijam, J.: FactsДокумент4 страницыMacario Lim Gaw, JR., Petitioner, vs. Commissioner OF Internal Revenue, Respondent. Tijam, J.: FactsmgeeОценок пока нет

- TLR Quiz No. 7 and 8 20230405 and 20230412Документ3 страницыTLR Quiz No. 7 and 8 20230405 and 20230412Carlo John C. RuelanОценок пока нет

- Mar 11 Tax CasesДокумент13 страницMar 11 Tax CasesMeg PalerОценок пока нет

- Bar Examination Questions in TaxationДокумент27 страницBar Examination Questions in TaxationKevin Chrysler MarcoОценок пока нет

- 2014 Bar ExaminationsДокумент9 страниц2014 Bar ExaminationsNFNLОценок пока нет

- Taxation B QДокумент6 страницTaxation B QChampo RadoОценок пока нет

- Qanda 2014Документ9 страницQanda 2014JortsОценок пока нет

- 2014 Tax Bar QAДокумент20 страниц2014 Tax Bar QAMo RockyОценок пока нет

- Tax Mock Answers KeyДокумент31 страницаTax Mock Answers KeypaulОценок пока нет

- Cordillera Career Development College Taxation Law 2 ACADEMIC YEAR 2019-2020 Final ExaminationДокумент5 страницCordillera Career Development College Taxation Law 2 ACADEMIC YEAR 2019-2020 Final ExaminationDoneli PuruggananОценок пока нет

- Phil. Journalists, Inc. v. CIR, G.R. No. 162852, Dec. 16, 2004.)Документ104 страницыPhil. Journalists, Inc. v. CIR, G.R. No. 162852, Dec. 16, 2004.)Alvin III SiapianОценок пока нет

- Tax 1 Final 2021Документ5 страницTax 1 Final 2021Karen Faye TorrecampoОценок пока нет

- Long-Examination 2 ARELLANO W Ans-1Документ8 страницLong-Examination 2 ARELLANO W Ans-1Kim RoqueОценок пока нет

- 2014 Taxation Law Bar Exam Questions and Suggested AnswersДокумент30 страниц2014 Taxation Law Bar Exam Questions and Suggested AnswersSyrine MallorcaОценок пока нет

- For GericahДокумент22 страницыFor GericahTauniño Jillandro Gamallo NeriОценок пока нет

- 2017 Bar Questions On Taxation Gen Pri and IncomeДокумент3 страницы2017 Bar Questions On Taxation Gen Pri and IncomeSheena PalmaresОценок пока нет

- 2009 TaxationДокумент16 страниц2009 TaxationBonito BulanОценок пока нет

- Taxation Law AssignmentДокумент23 страницыTaxation Law AssignmentTauniño Jillandro Gamallo NeriОценок пока нет

- AMBOL-Seatwork - RemediesДокумент8 страницAMBOL-Seatwork - RemediesCetacean HumpbackОценок пока нет

- Taxation Law Bar Questions 2017Документ7 страницTaxation Law Bar Questions 2017manol_salaОценок пока нет

- 2014 Bar Questions On Taxation Gen Pri and IncomeДокумент4 страницы2014 Bar Questions On Taxation Gen Pri and IncomeSheena PalmaresОценок пока нет

- 1st Mock Bar Tax Review February 27 20211Документ9 страниц1st Mock Bar Tax Review February 27 20211Francis Louie Allera HumawidОценок пока нет

- Taxation Review (Assignment)Документ4 страницыTaxation Review (Assignment)Glenn Mark Frejas RinionОценок пока нет

- 2017 Bar - Taxation LawДокумент5 страниц2017 Bar - Taxation LawMiamor NatividadОценок пока нет

- Taxation I True or FalseДокумент7 страницTaxation I True or FalseJms SapОценок пока нет

- Tax Bar 2010Документ7 страницTax Bar 2010Homer Lopez PabloОценок пока нет

- GR198729-30 CBK V CIRДокумент9 страницGR198729-30 CBK V CIRdskymaximusОценок пока нет

- Bersamin Case Digests TaxationДокумент16 страницBersamin Case Digests TaxationMargaret BeauchampОценок пока нет

- Digested Cases RevisedДокумент13 страницDigested Cases Revisedᜉᜂᜎᜊᜒᜀᜃ ᜎᜓᜌᜓᜎОценок пока нет

- 2017 Bar Q and AДокумент7 страниц2017 Bar Q and AAnonymous Mickey MouseОценок пока нет

- Ucc Mock Board Exam 2021 Taxation 70Документ15 страницUcc Mock Board Exam 2021 Taxation 70Veronika BlairОценок пока нет

- Tax RevДокумент4 страницыTax RevCanapi AmerahОценок пока нет

- Poli Rev Tax CasesДокумент26 страницPoli Rev Tax CasesBilton Cheng SyОценок пока нет

- PART I - 50% Unless Otherwise Indicated, Each of The Following Questions Is Worth 2%Документ3 страницыPART I - 50% Unless Otherwise Indicated, Each of The Following Questions Is Worth 2%Roxanne Datuin UsonОценок пока нет

- Santos - Case DigestДокумент4 страницыSantos - Case DigestHazel SantosОценок пока нет

- (J. Bersamin) : Code of Services Subject To VAT Is ExclusiveДокумент7 страниц(J. Bersamin) : Code of Services Subject To VAT Is ExclusiveED RCОценок пока нет

- Gen Principles DigestДокумент12 страницGen Principles DigestCzarina Joy PenaОценок пока нет

- TAX ProjectДокумент3 страницыTAX ProjectJames Ibrahim AlihОценок пока нет

- CIR V Phil. AluminumДокумент7 страницCIR V Phil. AluminumJeunaj LardizabalОценок пока нет

- Christmas Party Letter To NeighbourДокумент1 страницаChristmas Party Letter To NeighbourMsIc GabrielОценок пока нет

- Digest Tax2 Day4Документ23 страницыDigest Tax2 Day4MsIc GabrielОценок пока нет

- CREA Request For Legal OpinionДокумент1 страницаCREA Request For Legal OpinionMsIc GabrielОценок пока нет

- General Audit Procedures and DocumentationДокумент7 страницGeneral Audit Procedures and DocumentationCaroline MastersОценок пока нет

- Paray Vs Rodriguez FullДокумент26 страницParay Vs Rodriguez FullMsIc GabrielОценок пока нет

- Guaranty Full CasesДокумент35 страницGuaranty Full CasesMsIc GabrielОценок пока нет

- Civil Law PrinciplesДокумент10 страницCivil Law PrinciplesMsIc GabrielОценок пока нет

- Trade Investment Full CaseДокумент8 страницTrade Investment Full CaseMsIc GabrielОценок пока нет

- Deposit Full CasesДокумент13 страницDeposit Full CasesMsIc GabrielОценок пока нет

- SPES&GIP RequirementsДокумент2 страницыSPES&GIP RequirementsMsIc GabrielОценок пока нет

- Partnership 3 CasesДокумент8 страницPartnership 3 CasesMsIc GabrielОценок пока нет

- Agro Vs CA FactsДокумент2 страницыAgro Vs CA FactsMsIc GabrielОценок пока нет

- Partnership 3 CasesДокумент8 страницPartnership 3 CasesMsIc GabrielОценок пока нет

- Cta Last 2 CaseДокумент2 страницыCta Last 2 CaseMsIc GabrielОценок пока нет

- Sample Scripts WordДокумент22 страницыSample Scripts WordMsIc GabrielОценок пока нет

- Balatbat vs. CAДокумент5 страницBalatbat vs. CAMsIc GabrielОценок пока нет

- Lopez Vs Fajardo Lease MSWДокумент12 страницLopez Vs Fajardo Lease MSWMsIc GabrielОценок пока нет

- Cir Union First PartДокумент2 страницыCir Union First PartMsIc GabrielОценок пока нет

- Agasen vs. CAДокумент3 страницыAgasen vs. CAMsIc GabrielОценок пока нет

- Family Rights: FC Art. 69 FC Art. 71 FC Art. 72Документ10 страницFamily Rights: FC Art. 69 FC Art. 71 FC Art. 72MsIc GabrielОценок пока нет

- Raul Case PDFДокумент1 страницаRaul Case PDFMsIc GabrielОценок пока нет

- Issues Schedule Witnesses: 29 AUGUST 2015Документ2 страницыIssues Schedule Witnesses: 29 AUGUST 2015MsIc GabrielОценок пока нет

- Issues Schedule Witnesses Issue 1 SEPTEMBER 17, 2015 Plaintiff: 1. Karlo Noche Defendant 2. Jeff VinasДокумент2 страницыIssues Schedule Witnesses Issue 1 SEPTEMBER 17, 2015 Plaintiff: 1. Karlo Noche Defendant 2. Jeff VinasMsIc GabrielОценок пока нет

- IPL Case FullДокумент28 страницIPL Case FullMsIc GabrielОценок пока нет

- Statement of Comprihebsive IncomeДокумент3 страницыStatement of Comprihebsive IncomeMuhammad MahmoodОценок пока нет

- Homework Number 4Документ8 страницHomework Number 4ARISОценок пока нет

- Cta 2D CV 06616 D 2008feb14 Ass PDFДокумент40 страницCta 2D CV 06616 D 2008feb14 Ass PDFGe LatoОценок пока нет

- TAXATIONДокумент17 страницTAXATIONLamaire Abalos BatoyogОценок пока нет

- Last Date of Submission 14/11/19: S.no Student - Name ClassДокумент2 страницыLast Date of Submission 14/11/19: S.no Student - Name ClassAmritansh ShrivastavaОценок пока нет

- Busi Tax 3Документ2 страницыBusi Tax 3Jason MalikОценок пока нет

- PIN Certificate: This Is To Certify That Taxpayer Shown Herein Has Been Registered With Kenya Revenue AuthorityДокумент1 страницаPIN Certificate: This Is To Certify That Taxpayer Shown Herein Has Been Registered With Kenya Revenue AuthorityFelix BrianОценок пока нет

- Money and Banking Objective QuestionsДокумент5 страницMoney and Banking Objective QuestionsrudhrasivamОценок пока нет

- Quiz 9 &10Документ17 страницQuiz 9 &10Uzma Siddiqui100% (1)

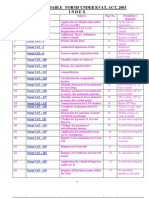

- Forms KvatДокумент63 страницыForms KvatShashi KanthОценок пока нет

- Worksheet#5-MCQ-2018 Engineering EconomyДокумент4 страницыWorksheet#5-MCQ-2018 Engineering EconomyOmar F'KassarОценок пока нет

- GST Session 43Документ20 страницGST Session 43manjulaОценок пока нет

- Taxbanter Special Topic MaterialsДокумент84 страницыTaxbanter Special Topic MaterialsJessica YuОценок пока нет

- Not Soppl: WingreensДокумент2 страницыNot Soppl: WingreensR ChandruОценок пока нет

- Latar Belakang GST Di MalaysiaДокумент49 страницLatar Belakang GST Di MalaysiaBenny WeeОценок пока нет

- BIR Form 0616 Amnesty Tax Payment Form PDFДокумент1 страницаBIR Form 0616 Amnesty Tax Payment Form PDFLeichelle BautistaОценок пока нет

- HR Block Income Tax Return Checklist Individuals 0620 FAДокумент1 страницаHR Block Income Tax Return Checklist Individuals 0620 FAdeОценок пока нет

- Summer Training ReportДокумент58 страницSummer Training ReportKani ShkaОценок пока нет

- Lecture - 15: Computation of Income Under The Head House Property (Basic Terminology)Документ41 страницаLecture - 15: Computation of Income Under The Head House Property (Basic Terminology)Harjot SinghОценок пока нет

- Bill FormsДокумент12 страницBill FormsVeerapandianОценок пока нет

- Franking Account WorkpaperДокумент6 страницFranking Account WorkpaperCarol YaoОценок пока нет

- Cta 3D CV 09255 D 2019apr04 Ass PDFДокумент32 страницыCta 3D CV 09255 D 2019apr04 Ass PDFaudreydql5Оценок пока нет

- Health Ensure Floater - Policy Schedule: Proposer DetailsДокумент3 страницыHealth Ensure Floater - Policy Schedule: Proposer DetailsValand NileshОценок пока нет