Вам также может понравиться

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- ILMA Purchase and Sale AgreementДокумент30 страницILMA Purchase and Sale AgreementDavid Dorr100% (1)

- Insurance Law OutlineДокумент8 страницInsurance Law OutlineKarl Marxcuz ReyesОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Celent Claims System VendorsДокумент47 страницCelent Claims System VendorsHavoc2003Оценок пока нет

- Guide For Principles and Practice of Insurance and Survey & Loss AssessmentДокумент18 страницGuide For Principles and Practice of Insurance and Survey & Loss AssessmentPankaj Gupta0% (1)

- LLB Refresher Notes Insurance LawДокумент43 страницыLLB Refresher Notes Insurance LawKriti Bhandari93% (14)

- Swiss Re - Exposure Rating of RiskДокумент32 страницыSwiss Re - Exposure Rating of Risk'Shahbaz Ahmed'0% (2)

- IFRS 17 - Insurance ContractsДокумент8 страницIFRS 17 - Insurance ContractsSaba Masood0% (1)

- IC-85 Reinsurance PDFДокумент342 страницыIC-85 Reinsurance PDFYesu Babu100% (1)

- Wesco Financial Munger LettersДокумент286 страницWesco Financial Munger LettersIrelandYardОценок пока нет

- The Philippine Guaranty Co., Inc. v. CIRДокумент1 страницаThe Philippine Guaranty Co., Inc. v. CIRMary BoaquiñaОценок пока нет

- SocGen New World OrderДокумент18 страницSocGen New World Ordera_sarosh7050Оценок пока нет

- ING Change of Ownership InterceptionДокумент3 страницыING Change of Ownership InterceptionDavid DorrОценок пока нет

- Gerova Financial GroupДокумент20 страницGerova Financial GroupDavid DorrОценок пока нет

- Lisa Actuarial Tables Female Smoker ANBДокумент1 страницаLisa Actuarial Tables Female Smoker ANBDavid DorrОценок пока нет

- Caldwell COIДокумент2 страницыCaldwell COIDavid DorrОценок пока нет

- Reg 198 NsoutreachtДокумент2 страницыReg 198 NsoutreachtDavid DorrОценок пока нет

- Lisa Actuarial Tables Female Smoker ANBДокумент1 страницаLisa Actuarial Tables Female Smoker ANBDavid DorrОценок пока нет

- Lisa Actuarial Tables Female Smoker ANBДокумент1 страницаLisa Actuarial Tables Female Smoker ANBDavid DorrОценок пока нет

- Trade Report February 09Документ7 страницTrade Report February 09David DorrОценок пока нет

- Trade Report January 09Документ11 страницTrade Report January 09David DorrОценок пока нет

- Sec 3-24-10Документ13 страницSec 3-24-10David DorrОценок пока нет

- Trade Report April 09Документ11 страницTrade Report April 09David DorrОценок пока нет

- Trade Report December 08Документ11 страницTrade Report December 08David DorrОценок пока нет

- The Role of Longevity Bonds in Optimal PortfolioДокумент17 страницThe Role of Longevity Bonds in Optimal PortfolioDavid DorrОценок пока нет

- The Design of Securitization For Longevity RiskДокумент52 страницыThe Design of Securitization For Longevity RiskDavid DorrОценок пока нет

- Trade Report June 09Документ9 страницTrade Report June 09David DorrОценок пока нет

- Trade Report May 09Документ10 страницTrade Report May 09David DorrОценок пока нет

- Trade Report March 09Документ9 страницTrade Report March 09David DorrОценок пока нет

- The Volatility of MortalityДокумент26 страницThe Volatility of MortalityDavid DorrОценок пока нет

- Securitizing and Tranching Longevity ExposuresДокумент41 страницаSecuritizing and Tranching Longevity ExposuresDavid DorrОценок пока нет

- Survivor DerivativesДокумент34 страницыSurvivor DerivativesDavid DorrОценок пока нет

- Stochastic Portfolio Specific MortalityДокумент20 страницStochastic Portfolio Specific MortalityDavid DorrОценок пока нет

- Securitized Senior Life SettlementsДокумент20 страницSecuritized Senior Life SettlementsDavid DorrОценок пока нет

- Pricing Longevity Bonds Using Implied Survival ProbabilitiesДокумент21 страницаPricing Longevity Bonds Using Implied Survival ProbabilitiesDavid DorrОценок пока нет

- Static Hedging Effectiveness For Longevity RiskДокумент35 страницStatic Hedging Effectiveness For Longevity RiskDavid DorrОценок пока нет

- Q Forwards JP MorganДокумент4 страницыQ Forwards JP MorganDavid DorrОценок пока нет

- Quadratic Stochastic Intensity and Prospective Mortality TablesДокумент43 страницыQuadratic Stochastic Intensity and Prospective Mortality TablesDavid DorrОценок пока нет

- Options On Normal UnderlyingsДокумент29 страницOptions On Normal UnderlyingsDavid DorrОценок пока нет

- Open Source PresentationДокумент10 страницOpen Source PresentationDavid DorrОценок пока нет

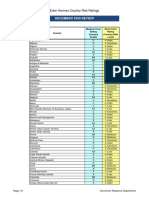

- December 2020 Review: Euler Hermes Country Risk RatingsДокумент5 страницDecember 2020 Review: Euler Hermes Country Risk RatingsLFОценок пока нет

- CIR v. BOAC 149 SCRA 395Документ11 страницCIR v. BOAC 149 SCRA 395Marge OstanОценок пока нет

- CPCU 520 Mid Term Exam Answer Guide V 2Документ9 страницCPCU 520 Mid Term Exam Answer Guide V 2asdfsdfОценок пока нет

- Principles of Insurance INS21 - Chapter05Документ11 страницPrinciples of Insurance INS21 - Chapter05SMonalisaPatroОценок пока нет

- Insurance QBДокумент63 страницыInsurance QBkrishna chaitanyaОценок пока нет

- Enmienda IFRS 17 IFRS2020 PDFДокумент140 страницEnmienda IFRS 17 IFRS2020 PDFOmarОценок пока нет

- PD1270Документ2 страницыPD1270Ronadale Zapata-AcostaОценок пока нет

- 3FAT - Corporate ProfileДокумент16 страниц3FAT - Corporate ProfileKrishna SaiОценок пока нет

- Captive List (New Format) - 03312021Документ70 страницCaptive List (New Format) - 03312021vipinsahniОценок пока нет

- Implementing Rules (AMLA)Документ22 страницыImplementing Rules (AMLA)AMBОценок пока нет

- Suncorp ResultsДокумент7 страницSuncorp ResultsTim MooreОценок пока нет

- Insurance Lecture 1Документ21 страницаInsurance Lecture 1Manjare Hassin RaadОценок пока нет

- Basic Reinsurance Guide PDFДокумент80 страницBasic Reinsurance Guide PDFKandeel AfzalОценок пока нет

- Advanced Diploma in Insurance: The Chartered Insurance InstituteДокумент8 страницAdvanced Diploma in Insurance: The Chartered Insurance InstituteSultan AlrasheedОценок пока нет

- Curriculum Vitae of a.W.J. (Tony) Fernandez, 13-Jun-13Документ22 страницыCurriculum Vitae of a.W.J. (Tony) Fernandez, 13-Jun-13awjfernandezОценок пока нет

- Weather and Climate Extremes: Peter HoeppeДокумент10 страницWeather and Climate Extremes: Peter HoeppeDário MacedoОценок пока нет

- The Nature of Reinsurance: A List of Potentially Interesting Web Sites of Relevance To This BookДокумент26 страницThe Nature of Reinsurance: A List of Potentially Interesting Web Sites of Relevance To This BookDean RodriguezОценок пока нет

- Half-Year Financial Report Munich ReДокумент54 страницыHalf-Year Financial Report Munich Rekovi mОценок пока нет

- Everything You Need To Know About The PCS Catastrophe Loss IndexДокумент7 страницEverything You Need To Know About The PCS Catastrophe Loss IndexTom Johansmeyer100% (1)

- A5 Valuation OutlinesДокумент124 страницыA5 Valuation OutlinesThiện Trần ĐứcОценок пока нет

- Risk Final Exam QuestionsДокумент6 страницRisk Final Exam Questionsnathnael75% (4)