Вам также может понравиться

- WHAT'S F.R.E.E. CREDIT? the personal game changerОт EverandWHAT'S F.R.E.E. CREDIT? the personal game changerРейтинг: 2 из 5 звезд2/5 (1)

- Credit Card: Mini-LessonДокумент54 страницыCredit Card: Mini-LessonRachana NagpalОценок пока нет

- Credit CardsДокумент22 страницыCredit CardsEti Prince BajajОценок пока нет

- Credit Card Processing GlossaryДокумент14 страницCredit Card Processing Glossarykintirgum100% (1)

- Credit & Debit CardДокумент42 страницыCredit & Debit CardRimna Prakash100% (1)

- Hacking Point of Sale: Payment Application Secrets, Threats, and SolutionsОт EverandHacking Point of Sale: Payment Application Secrets, Threats, and SolutionsРейтинг: 5 из 5 звезд5/5 (1)

- Data2 Dapimage 1409021911 CreditCardApplication1409021911Документ4 страницыData2 Dapimage 1409021911 CreditCardApplication1409021911Michel ThompsonОценок пока нет

- Credit Card Response CodesДокумент5 страницCredit Card Response CodesCarlito Brigante100% (1)

- Debit Card Issued by A Bank Allowing The Holder To Transfer Money Electronically To Another Bank Account When Making A PurchaseДокумент9 страницDebit Card Issued by A Bank Allowing The Holder To Transfer Money Electronically To Another Bank Account When Making A PurchaseShovan ChowdhuryОценок пока нет

- Etihad Credit Card Authorization FormДокумент17 страницEtihad Credit Card Authorization FormFarha AnsariОценок пока нет

- Corporation Bank Credit CardsДокумент7 страницCorporation Bank Credit CardsSuriya KJ100% (1)

- Cloud AtmДокумент24 страницыCloud AtmNagesh Lakshminarayan100% (1)

- Understanding The Background of Credit CardДокумент17 страницUnderstanding The Background of Credit CarddeepanshuОценок пока нет

- Credit CardДокумент77 страницCredit CardSamuel DavisОценок пока нет

- Using CR CardsДокумент2 страницыUsing CR CardsFlaviub23Оценок пока нет

- Credit CardДокумент81 страницаCredit CardsuryakantshrotriyaОценок пока нет

- Us 15 Fillmore Crash Pay How To Own and Clone Contactless Payment DevicesДокумент60 страницUs 15 Fillmore Crash Pay How To Own and Clone Contactless Payment Devicescrhistian lennonОценок пока нет

- Automated Teller Machine (Atm) : Atms Have Become A Quick, Convenient Way To Access Money in Your AccountsДокумент24 страницыAutomated Teller Machine (Atm) : Atms Have Become A Quick, Convenient Way To Access Money in Your AccountsKamal KunduОценок пока нет

- Credit Card Tips You Should Not Ignorexdekr PDFДокумент2 страницыCredit Card Tips You Should Not Ignorexdekr PDFHerringBarnett98Оценок пока нет

- Credit Card ProcessingДокумент28 страницCredit Card ProcessingvluhadОценок пока нет

- Credit CardsДокумент15 страницCredit CardsAmit AdesharaОценок пока нет

- Operation of Credit CardsДокумент13 страницOperation of Credit CardsSudu PuthaОценок пока нет

- As 3769-1990 Automatic Teller Machines - User AccessДокумент8 страницAs 3769-1990 Automatic Teller Machines - User AccessSAI Global - APACОценок пока нет

- Debit - Credit Cards Without CreditДокумент7 страницDebit - Credit Cards Without CreditMaimai DuranoОценок пока нет

- Payslip Jul2023 EDU - 01098Документ1 страницаPayslip Jul2023 EDU - 01098PrabhuОценок пока нет

- Debit and Credit Card - EditedДокумент24 страницыDebit and Credit Card - EditedNikita MutrejaОценок пока нет

- Credit and Debit CardsДокумент3 страницыCredit and Debit CardsmaomaoОценок пока нет

- Virtual Debit Card FAQДокумент9 страницVirtual Debit Card FAQKelly C. GilesОценок пока нет

- E-Commerce: Credit Cards & SetДокумент18 страницE-Commerce: Credit Cards & SetAbirami SridharОценок пока нет

- Chip and Pin Is BrokenДокумент14 страницChip and Pin Is BrokenPacketerrorОценок пока нет

- Canara Credit Cards User Manual Cor 4Документ11 страницCanara Credit Cards User Manual Cor 4Parag BarmanОценок пока нет

- Mis Project ReportДокумент44 страницыMis Project Reportw8ingforuОценок пока нет

- Goods and Services Tax/harmonized Sales Tax Credit (GST/HSTC) NoticeДокумент3 страницыGoods and Services Tax/harmonized Sales Tax Credit (GST/HSTC) NoticeSam StormeОценок пока нет

- GSM Based Smart Information System For Lost Atm Cards.Документ8 страницGSM Based Smart Information System For Lost Atm Cards.Emin KültürelОценок пока нет

- EMVДокумент13 страницEMVMauricio ManghiОценок пока нет

- Evaluation of Some Online Payment Providers Services: Best Online Banks and Visa/Master Cards IssuersОт EverandEvaluation of Some Online Payment Providers Services: Best Online Banks and Visa/Master Cards IssuersОценок пока нет

- CRATMCARDSДокумент2 страницыCRATMCARDSFlaviub23100% (1)

- Code ListДокумент192 страницыCode ListMohammad Alamgir HossainОценок пока нет

- Woot13 RolandДокумент13 страницWoot13 RolandEnigmaОценок пока нет

- Credit Cards: Personal FinanceДокумент36 страницCredit Cards: Personal FinanceAmara MaduagwuОценок пока нет

- Contactless PaymentДокумент40 страницContactless PaymentmikeОценок пока нет

- Strategies and Techniques of Banking Security and ATMsДокумент6 страницStrategies and Techniques of Banking Security and ATMsVIVA-TECH IJRIОценок пока нет

- Report On RoborticsДокумент22 страницыReport On Roborticsasma246Оценок пока нет

- Bill of Supply For Electricity: Due DateДокумент1 страницаBill of Supply For Electricity: Due DateVinnay DahiyaОценок пока нет

- GuideДокумент26 страницGuideJaikishan KumaraswamyОценок пока нет

- Electronic Payment SystemsДокумент36 страницElectronic Payment Systemsjoe_inba100% (1)

- Statement 14-APR-23 AC 63755886 16042114Документ6 страницStatement 14-APR-23 AC 63755886 16042114Shauna DunnОценок пока нет

- Credit CardДокумент18 страницCredit CardRs TiwariОценок пока нет

- Cards: March XX, 2010Документ57 страницCards: March XX, 2010Keerti MannanОценок пока нет

- You’Re a Business Owner, Not a Dummy!: Understand Your Merchant AccountОт EverandYou’Re a Business Owner, Not a Dummy!: Understand Your Merchant AccountРейтинг: 2 из 5 звезд2/5 (1)

- 2、贝宝转账流程 - 英文Документ11 страниц2、贝宝转账流程 - 英文Andri Anto100% (1)

- Credit Card: Dr. Yamini Sharma D.M.SДокумент31 страницаCredit Card: Dr. Yamini Sharma D.M.SJames RossОценок пока нет

- Debit Card (Also Known As A Bank Card or Check Card) Is A Plastic Card That Provides AnДокумент7 страницDebit Card (Also Known As A Bank Card or Check Card) Is A Plastic Card That Provides Anmuthukumaran28Оценок пока нет

- MDZ01-200 Seller Contract 13sept2018Документ5 страницMDZ01-200 Seller Contract 13sept2018Vaithiswari100% (1)

- MIS A Report On Plastic MoneyДокумент16 страницMIS A Report On Plastic Moneyshah faisal100% (2)

- Credit Card Information 1Документ3 страницыCredit Card Information 1api-3710686770% (1)

- Merchant Guide To The Visa Address Verification ServiceДокумент21 страницаMerchant Guide To The Visa Address Verification ServiceCesar ChОценок пока нет

- Platinum Ser GuideДокумент97 страницPlatinum Ser GuideRohit RoyОценок пока нет

- Travel For Holiday & Inspecting Rental Property: What Is Deductible?Документ3 страницыTravel For Holiday & Inspecting Rental Property: What Is Deductible?AdrianОценок пока нет

- As485070 Dec2022 PayslipДокумент2 страницыAs485070 Dec2022 PayslipAKM Enterprises Pvt LtdОценок пока нет

- Bangladesh Railway: Shohoz - Synesis - Vincen JVДокумент1 страницаBangladesh Railway: Shohoz - Synesis - Vincen JVসাইদুর রহমানОценок пока нет

- Annex C RR 11-2018Документ1 страницаAnnex C RR 11-2018KB WorldОценок пока нет

- TR 17 ReverseДокумент1 страницаTR 17 ReverseAbdul Rehman CheemaОценок пока нет

- Installment No 2 - 2022075Документ1 страницаInstallment No 2 - 2022075IsmailОценок пока нет

- Campus Date of Joining: Noida Institute of Engineering & Technology (NIET) July 18, 2022Документ2 страницыCampus Date of Joining: Noida Institute of Engineering & Technology (NIET) July 18, 2022KESHAV JHAОценок пока нет

- CC PDFДокумент6 страницCC PDFJaya JayavardhanОценок пока нет

- Rentohay Manullang Manajemen Perpajakan - Transfer PricingДокумент9 страницRentohay Manullang Manajemen Perpajakan - Transfer PricingRento ManullangОценок пока нет

- BM2324I003897254Документ3 страницыBM2324I003897254Shubham ShuklaОценок пока нет

- MEDITECH - MEDITECH Statement 20191128 PDFДокумент49 страницMEDITECH - MEDITECH Statement 20191128 PDFLion Micheal OtitolaiyeОценок пока нет

- Flamen, Inc.: Statement of Management Responsibility For Annual Income Tax ReturnДокумент2 страницыFlamen, Inc.: Statement of Management Responsibility For Annual Income Tax Returndaryl canozaОценок пока нет

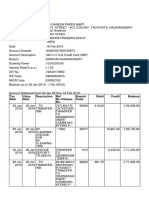

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceДокумент3 страницыStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceTanuj KukretiОценок пока нет

- Accounting Voucher 60Документ1 страницаAccounting Voucher 60Pavan BhandareОценок пока нет

- Shabu Batak TaxationДокумент41 страницаShabu Batak TaxationJOSHUA M. ESCOTOОценок пока нет

- Tax Invoice: BHAKTI ENTERPRISES - (From 1-Apr-2018Документ1 страницаTax Invoice: BHAKTI ENTERPRISES - (From 1-Apr-2018Parth DamaОценок пока нет

- ICGAB New Tax Syllabus (Sep-19)Документ9 страницICGAB New Tax Syllabus (Sep-19)Aminul HaqОценок пока нет

- Additional Income and Adjustments To IncomeДокумент1 страницаAdditional Income and Adjustments To IncomeSz. RolandОценок пока нет

- Isbm UNI CMI IIM Naip Bepuk: Personal DetailsДокумент2 страницыIsbm UNI CMI IIM Naip Bepuk: Personal DetailsPranoj P FrancisОценок пока нет

- Work Sheet Computation of Income Under The Head "Capital Gains"Документ4 страницыWork Sheet Computation of Income Under The Head "Capital Gains"Vishal SarkarОценок пока нет

- ACCT 3061 Asignación Cap 4 y 5Документ4 страницыACCT 3061 Asignación Cap 4 y 5gpm-81Оценок пока нет

- BSNL Odisha BillДокумент3 страницыBSNL Odisha BillASANTA SWAINОценок пока нет

- Ca Edd Form 1099GДокумент1 страницаCa Edd Form 1099Gjorge Gregorio seguraОценок пока нет

- Jan Bill - AnandДокумент1 страницаJan Bill - AnandanandОценок пока нет