Вам также может понравиться

- Blue Nile Case NotesДокумент18 страницBlue Nile Case Notesenergizerabby100% (1)

- Auditing Theory - 100Q: Audit Report CMPДокумент10 страницAuditing Theory - 100Q: Audit Report CMPMaria PauОценок пока нет

- W Final ExamДокумент42 страницыW Final ExamAnna TaylorОценок пока нет

- At5906 Audit ReportДокумент8 страницAt5906 Audit ReportImelda leeОценок пока нет

- Question Bank RawДокумент178 страницQuestion Bank RawLê Na100% (2)

- University of San Jose-Recoletos Auditing TheoryДокумент10 страницUniversity of San Jose-Recoletos Auditing TheoryAstraea Hoshi100% (1)

- AT ExamДокумент9 страницAT ExamKwatro SankaiОценок пока нет

- Cost Classification Overhead Costs AllocДокумент40 страницCost Classification Overhead Costs AllocAbayineh MesenbetОценок пока нет

- Ch14 - Audit ReportsДокумент25 страницCh14 - Audit ReportsMar Feilson Zulueta LatayanОценок пока нет

- At-5906 Audit ReportДокумент10 страницAt-5906 Audit Reportshambiruar100% (4)

- Solution Manual For Auditing and Assurance Services 4th Edition by LouwersДокумент14 страницSolution Manual For Auditing and Assurance Services 4th Edition by Louwersenergizerabby50% (4)

- Audit Report On Financial StatementsДокумент37 страницAudit Report On Financial StatementsPeter BanjaoОценок пока нет

- PSA 700, 705, 706, 710, 720 ExercisesДокумент11 страницPSA 700, 705, 706, 710, 720 ExercisesRalph Francis BirungОценок пока нет

- Panera Bread Case StudyДокумент18 страницPanera Bread Case StudyAvnchick100% (1)

- Configuration FICOДокумент253 страницыConfiguration FICOjiljil1980Оценок пока нет

- Mas Test BankДокумент23 страницыMas Test BankFrancine Holler100% (1)

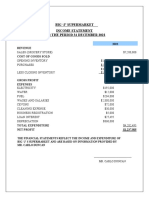

- Big 'J'S Supermarket Income Statement 2022Документ2 страницыBig 'J'S Supermarket Income Statement 2022Stephen Francis100% (1)

- Cpa Review School of The Philippines: Related Psas: Psa 700, 710, 720, 560, 570, 600 and 620Документ49 страницCpa Review School of The Philippines: Related Psas: Psa 700, 710, 720, 560, 570, 600 and 620Jasmine LimОценок пока нет

- Chapter 17 - Test BankДокумент52 страницыChapter 17 - Test Bankjuan100% (2)

- Chapter 10 Audit ReportsДокумент7 страницChapter 10 Audit ReportsSteffany RoqueОценок пока нет

- At 5906 Audit ReportДокумент11 страницAt 5906 Audit ReportZyl Diez MagnoОценок пока нет

- At PreboardДокумент12 страницAt PreboardKevin Ryan EscobarОценок пока нет

- CPAR CompilationДокумент49 страницCPAR CompilationMarjorie ParaynoОценок пока нет

- 7Документ25 страниц7Anonymous N9dx4ATEghОценок пока нет

- CH 12 QuizДокумент4 страницыCH 12 QuizwsviviОценок пока нет

- SUBJECT MATTER 6 - QuizДокумент4 страницыSUBJECT MATTER 6 - QuizKingChryshAnneОценок пока нет

- Auditors' Reports: True / False QuestionsДокумент13 страницAuditors' Reports: True / False QuestionsLime MОценок пока нет

- Post TestДокумент40 страницPost TestRubyJadeRoferosОценок пока нет

- Chapter13 BWДокумент14 страницChapter13 BWLiliОценок пока нет

- DebateДокумент9 страницDebateWed CornelОценок пока нет

- Audit Report Exer MC 1920 W Key1Документ8 страницAudit Report Exer MC 1920 W Key1aleachonОценок пока нет

- DocxДокумент22 страницыDocxElaine Joyce GarciaОценок пока нет

- Chapter 17 Audits ReportДокумент48 страницChapter 17 Audits ReportShundei OtawaraОценок пока нет

- Chapter 17 Audits ReportДокумент16 страницChapter 17 Audits ReportAndyОценок пока нет

- Audit Reports: Statements Is Contained in TheДокумент10 страницAudit Reports: Statements Is Contained in TheElaine Joyce GarciaОценок пока нет

- RevisedQuali atДокумент21 страницаRevisedQuali atlisa juganОценок пока нет

- Audit Report: Mark Glenn G. Parpan, CpaДокумент41 страницаAudit Report: Mark Glenn G. Parpan, CpaChristine Joy Duterte RemorozaОценок пока нет

- Pretest Aud001Документ8 страницPretest Aud001KathleenОценок пока нет

- Audit Report - QuestionnaireДокумент11 страницAudit Report - QuestionnaireZhykiie MackОценок пока нет

- Auditing and Assurance Services 15th Edition Chapter 3 Homework AnswersДокумент5 страницAuditing and Assurance Services 15th Edition Chapter 3 Homework AnswersPenghui Shi50% (2)

- AT Quizzer 13 - Reporting Issues (2TAY1718) PDFДокумент10 страницAT Quizzer 13 - Reporting Issues (2TAY1718) PDFWihl Mathew Zalatar0% (1)

- Understanding Audit ReportsДокумент39 страницUnderstanding Audit ReportsBorutoОценок пока нет

- C13 ReviewerДокумент18 страницC13 Reviewerlender kent alicanteОценок пока нет

- Chapter 3 Quiz KeyДокумент2 страницыChapter 3 Quiz KeyAmna MalikОценок пока нет

- Which of The Following Information IsДокумент6 страницWhich of The Following Information IsCarlo ParasОценок пока нет

- EXAM1 SampleДокумент12 страницEXAM1 SampleCandace WagnerОценок пока нет

- Quiz On Audit Report and DocumentationДокумент6 страницQuiz On Audit Report and DocumentationTrisha Mae AlburoОценок пока нет

- Review Materials I (20230225193838)Документ11 страницReview Materials I (20230225193838)Fake AccountОценок пока нет

- At Quizzer 14 - Reporting IssuesДокумент18 страницAt Quizzer 14 - Reporting IssuesRachel Leachon50% (2)

- Audit ReportsДокумент27 страницAudit ReportsMa Lourdes T CahatianОценок пока нет

- Qualified "Except For" GAAP: Justified Departure Gaap Going Concern: (After Opinion Paragraph)Документ11 страницQualified "Except For" GAAP: Justified Departure Gaap Going Concern: (After Opinion Paragraph)Steffan MilesОценок пока нет

- Audit Report - HighlightedДокумент11 страницAudit Report - Highlighteddewlate abinaОценок пока нет

- Test Bank Chapter 17 - Falak Jan EnayatДокумент19 страницTest Bank Chapter 17 - Falak Jan EnayatFalak EnayatОценок пока нет

- Cpa Review School of The Philippines: Related Psas: Psa 700, 710, 720, 560, 570, 600 and 620Документ20 страницCpa Review School of The Philippines: Related Psas: Psa 700, 710, 720, 560, 570, 600 and 620melody btobОценок пока нет

- Audited Financial StatementsДокумент6 страницAudited Financial StatementsfredluxxОценок пока нет

- CPA A 1 Audit ReportsДокумент26 страницCPA A 1 Audit ReportsLilliane EstrellaОценок пока нет

- Brainscape 4Документ7 страницBrainscape 4Bea chuaОценок пока нет

- Chapter 6Документ15 страницChapter 6Moti Bekele100% (1)

- CHP 12 MCДокумент3 страницыCHP 12 MCMatt HОценок пока нет

- Audit ReportsДокумент30 страницAudit ReportsTerrene LeacockОценок пока нет

- Engagement Essentials: Preparation, Compilation, and Review of Financial StatementsОт EverandEngagement Essentials: Preparation, Compilation, and Review of Financial StatementsОценок пока нет

- Annual Update and Practice Issues for Preparation, Compilation, and Review EngagementsОт EverandAnnual Update and Practice Issues for Preparation, Compilation, and Review EngagementsОценок пока нет

- Codification of Statements on Standards for Accounting and Review Services: Numbers 1 - 23От EverandCodification of Statements on Standards for Accounting and Review Services: Numbers 1 - 23Оценок пока нет

- Audit Risk Alert: General Accounting and Auditing Developments, 2017/18От EverandAudit Risk Alert: General Accounting and Auditing Developments, 2017/18Оценок пока нет

- Strategies For Competing in Foreign Markets Multiple Choice QuestionsДокумент45 страницStrategies For Competing in Foreign Markets Multiple Choice QuestionsenergizerabbyОценок пока нет

- Jennifer Hood Discussion Board 4Документ3 страницыJennifer Hood Discussion Board 4energizerabbyОценок пока нет

- Medical Group: 1-888-236-2263. Our Office Hours Are Monday Through Friday 8:00a.m.to 4:30p.mДокумент3 страницыMedical Group: 1-888-236-2263. Our Office Hours Are Monday Through Friday 8:00a.m.to 4:30p.menergizerabbyОценок пока нет

- 10Документ19 страниц10energizerabbyОценок пока нет

- CH 6Документ54 страницыCH 6energizerabby0% (1)

- CH 6Документ54 страницыCH 6energizerabby0% (1)

- Hotel DataДокумент1 страницаHotel DataenergizerabbyОценок пока нет

- Wee K Readings/Resources Used Due DatesДокумент2 страницыWee K Readings/Resources Used Due DatesenergizerabbyОценок пока нет

- Wage Industry Occupation Education South Nonwh Hisp FemaleДокумент6 страницWage Industry Occupation Education South Nonwh Hisp FemaleenergizerabbyОценок пока нет

- Team League Wins ERA BA HRДокумент2 страницыTeam League Wins ERA BA HRenergizerabbyОценок пока нет

- wk8 DBДокумент2 страницыwk8 DBenergizerabbyОценок пока нет

- Listed AssignmentsДокумент6 страницListed AssignmentsenergizerabbyОценок пока нет

- Year Cars Sold (In Millions) Percent GMДокумент1 страницаYear Cars Sold (In Millions) Percent GMenergizerabbyОценок пока нет

- Panera Bread Company: Case Study #8Документ26 страницPanera Bread Company: Case Study #8energizerabbyОценок пока нет

- Db1 Answer 1Документ5 страницDb1 Answer 1energizerabbyОценок пока нет

- 5e Apollo Shoes CaseДокумент163 страницы5e Apollo Shoes CaseenergizerabbyОценок пока нет

- Homeowrk SpreadshetsДокумент2 страницыHomeowrk SpreadshetsenergizerabbyОценок пока нет

- Homeowrk SpreadshetsДокумент6 страницHomeowrk SpreadshetsenergizerabbyОценок пока нет

- Something Went Sour at ParmalatДокумент1 страницаSomething Went Sour at Parmalatenergizerabby100% (1)

- Homework AnswersДокумент37 страницHomework AnswersenergizerabbyОценок пока нет

- Social Media and Its Effect On BusinessДокумент7 страницSocial Media and Its Effect On BusinessenergizerabbyОценок пока нет

- ScheduleДокумент1 страницаScheduleenergizerabbyОценок пока нет

- BUSN 491 Syllabus Template - 8 WK - OL - 2015Документ14 страницBUSN 491 Syllabus Template - 8 WK - OL - 2015energizerabbyОценок пока нет

- Team League Wins ERA BA HRДокумент2 страницыTeam League Wins ERA BA HRenergizerabbyОценок пока нет

- References: Trial. Retrieved January 22, 2015, From ReutersДокумент1 страницаReferences: Trial. Retrieved January 22, 2015, From ReutersenergizerabbyОценок пока нет

- Social Media and Its Effect On BusinessДокумент7 страницSocial Media and Its Effect On BusinessenergizerabbyОценок пока нет

- A Study On Ratio Analysis of Axis BankДокумент70 страницA Study On Ratio Analysis of Axis BankVishal SinghОценок пока нет

- Casestudy RestaurantДокумент13 страницCasestudy RestaurantAbhishek RastogiОценок пока нет

- QUESTION 1 - Piskoti Pty Ltd-SolutionДокумент2 страницыQUESTION 1 - Piskoti Pty Ltd-SolutionStaid LynxОценок пока нет

- Full Download Financial Reporting Financial Statement Analysis and Valuation 9th Edition Wahlen Test BankДокумент36 страницFull Download Financial Reporting Financial Statement Analysis and Valuation 9th Edition Wahlen Test Bankjulianwellsueiy100% (30)

- Санхүүгийн Тайлангийн МАЯГТ Англи Хэл ДээрДокумент13 страницСанхүүгийн Тайлангийн МАЯГТ Англи Хэл Дээрmunkhtsetseg.tsogooОценок пока нет

- CF Remdial AssignmentДокумент5 страницCF Remdial AssignmentMadhav RajbanshiОценок пока нет

- BBA - JNU - 101 Fundamentals of Accounting PDFДокумент201 страницаBBA - JNU - 101 Fundamentals of Accounting PDFJTSalesОценок пока нет

- Exercises For Final PDFДокумент11 страницExercises For Final PDFThanh HằngОценок пока нет

- Paper - 19: Cost and Management Audit: MTP - Final - Syllabus-2016 - June 2020 - Set - 1Документ272 страницыPaper - 19: Cost and Management Audit: MTP - Final - Syllabus-2016 - June 2020 - Set - 1madebod832Оценок пока нет

- Chapter 1 Test BankДокумент4 страницыChapter 1 Test BankshanjidakterimiОценок пока нет

- MBA516 Assignment 1Документ2 страницыMBA516 Assignment 1ShamittaaОценок пока нет

- Payout Policy: © 2019 Pearson Education LTDДокумент7 страницPayout Policy: © 2019 Pearson Education LTDLeanne TehОценок пока нет

- Insurance Contracts Issued by Mutual Entities: Ifrs FoundationДокумент14 страницInsurance Contracts Issued by Mutual Entities: Ifrs FoundationIotalaseria PutuОценок пока нет

- Cpa Review School of The PhilippinesДокумент6 страницCpa Review School of The PhilippinesMarwin AceОценок пока нет

- IAS 8 - Accounting Policies, Changes in Accounting Estimates and Errors (With Notes) PDFДокумент91 страницаIAS 8 - Accounting Policies, Changes in Accounting Estimates and Errors (With Notes) PDF2123123asdasdaОценок пока нет

- Investments: SolutionДокумент8 страницInvestments: SolutionAce LimpinОценок пока нет

- Allowance For Doubtful DebtДокумент2 страницыAllowance For Doubtful DebtN Fatini FatahОценок пока нет

- Chapter 4 Free Cash Flows To Equity FrimДокумент22 страницыChapter 4 Free Cash Flows To Equity FrimMeena MkОценок пока нет

- Solution Manual03Документ68 страницSolution Manual03yellowberries100% (2)

- ch13 CURRENT LIABILITIES AND CONTINGENCIES PDFДокумент37 страницch13 CURRENT LIABILITIES AND CONTINGENCIES PDFRenz AlconeraОценок пока нет

- Copia de Caso Healthy Bear 2022Документ4 страницыCopia de Caso Healthy Bear 2022rataОценок пока нет

- Solution:: Purchases, Cash Basis P 2,850,000Документ2 страницыSolution:: Purchases, Cash Basis P 2,850,000Jen Deloy50% (2)

- The Disadvantages of BalancesheetДокумент5 страницThe Disadvantages of BalancesheetRiyas ParakkattilОценок пока нет

- ch24 2006Документ31 страницаch24 2006ChrisBaconОценок пока нет