Вам также может понравиться

- Medical Insurance Policy - FirstFix - Version3Документ3 страницыMedical Insurance Policy - FirstFix - Version3marklee torres100% (1)

- Pmsby PDFДокумент3 страницыPmsby PDFmd mubarakОценок пока нет

- The Consumer Protection Act 2018 Edited CopyДокумент75 страницThe Consumer Protection Act 2018 Edited CopyAbhishek K100% (1)

- Consumer Protection Act - Question BankДокумент9 страницConsumer Protection Act - Question BankDr. S. PRIYA DURGA MBA-STAFFОценок пока нет

- On Ford Car Services SatisfactionДокумент32 страницыOn Ford Car Services SatisfactionPrayag Dubey50% (2)

- Consumerism: "It Is The Shame of The Total Marketing Concept." - Peter F. DuckerДокумент20 страницConsumerism: "It Is The Shame of The Total Marketing Concept." - Peter F. DuckerdfchandОценок пока нет

- Loan Agreement 3Документ1 страницаLoan Agreement 3Lj PolcaОценок пока нет

- FOUNDATION COURSE Sem IV - QUESTION BANK (1) .En - MRДокумент17 страницFOUNDATION COURSE Sem IV - QUESTION BANK (1) .En - MRVishalОценок пока нет

- CSR Activities of Titan: A. IntroductionДокумент6 страницCSR Activities of Titan: A. IntroductionNeXuS BLZОценок пока нет

- Health Insurance in India-An Overview: K.Swathi, R.AnuradhaДокумент4 страницыHealth Insurance in India-An Overview: K.Swathi, R.AnuradhaAnkit YadavОценок пока нет

- Icici Life InsuranceДокумент40 страницIcici Life Insurancekrittika03Оценок пока нет

- Job-Interview NDA PDFДокумент2 страницыJob-Interview NDA PDFMikee AngelesОценок пока нет

- Lva1 App6892Документ62 страницыLva1 App6892Pallavi PalluОценок пока нет

- Memorandum of AgreementДокумент3 страницыMemorandum of AgreementjenelleОценок пока нет

- ICICI Bank Case StudyДокумент11 страницICICI Bank Case StudySunil RawatОценок пока нет

- Vipul Corp Lnsurance TPA PVT LTD.: Memorandum of Understanding (Mou)Документ7 страницVipul Corp Lnsurance TPA PVT LTD.: Memorandum of Understanding (Mou)Swapnil NageОценок пока нет

- Health InsuranceДокумент18 страницHealth Insurancekeerthi93Оценок пока нет

- Bank Marketing Mix New Stretegy in TodayДокумент10 страницBank Marketing Mix New Stretegy in TodayMirjana StefanovskiОценок пока нет

- MI Sumeet and Has Decided To Give Manufacturing and Selling Rights For TheДокумент4 страницыMI Sumeet and Has Decided To Give Manufacturing and Selling Rights For TheAdvAbhishek GokhaleОценок пока нет

- 04 Sample-Billboard-Agreement PDFДокумент4 страницы04 Sample-Billboard-Agreement PDFAbhishek SinghОценок пока нет

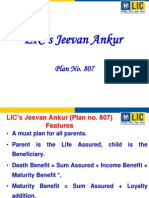

- Jeevan Ankur Ppt-Eng - LIC - 9884635430 - Child PlanДокумент17 страницJeevan Ankur Ppt-Eng - LIC - 9884635430 - Child PlanBabujee K.NОценок пока нет

- Kotak Mahindra (Indemnity)Документ3 страницыKotak Mahindra (Indemnity)gaurishguruОценок пока нет

- Case Study GroupДокумент9 страницCase Study GroupPrabhujot SinghОценок пока нет

- Us Service Level Agreements BPO 121214 (1) - Evgeny RomakinДокумент10 страницUs Service Level Agreements BPO 121214 (1) - Evgeny RomakinEvgeny RomakinОценок пока нет

- CHANGES IN INSURANCE SECTOR (A Study On Public Awareness)Документ47 страницCHANGES IN INSURANCE SECTOR (A Study On Public Awareness)Ramaduta80% (5)

- Presentation On Hire Purchase and LeasingДокумент25 страницPresentation On Hire Purchase and Leasingmanoj100% (1)

- Privatization of Insurance Sector in IndiaДокумент14 страницPrivatization of Insurance Sector in IndiaProf. R V SinghОценок пока нет

- Legal Formalities For Starting A BusinessДокумент4 страницыLegal Formalities For Starting A BusinessVareen voraОценок пока нет

- Cascading Effect Pre and Post GSTДокумент21 страницаCascading Effect Pre and Post GSTkaranОценок пока нет

- IB N C MRKTДокумент326 страницIB N C MRKTRana PrathapОценок пока нет

- MediclaimДокумент71 страницаMediclaimPushkar Koltharkar100% (6)

- A Project Report ON: "Customer Satisfaction Survey OnДокумент66 страницA Project Report ON: "Customer Satisfaction Survey Onsshane kumarОценок пока нет

- Declaration Us 194C Format2Документ1 страницаDeclaration Us 194C Format2CA SHOBHIT GoelОценок пока нет

- ReinsuranceДокумент40 страницReinsuranceAbid ParkarОценок пока нет

- Banking Allied ServicesДокумент30 страницBanking Allied ServicesSrinivasula Reddy P50% (2)

- List of Indian Accounting Standards Along With Comparative Accounting Standard (AS)Документ6 страницList of Indian Accounting Standards Along With Comparative Accounting Standard (AS)Krishna PrasadОценок пока нет

- Maklumat Pinjaman Kereta - IslamicДокумент6 страницMaklumat Pinjaman Kereta - IslamicIsham119Оценок пока нет

- A Report On: Customer Relationship Management of Idbi Federal Life InsuranceДокумент95 страницA Report On: Customer Relationship Management of Idbi Federal Life InsuranceamitОценок пока нет

- Problems and Prospects of General Insurance in BangladeshДокумент56 страницProblems and Prospects of General Insurance in BangladeshAmirul Islam75% (4)

- Role and Function of Health Insurance IndiaДокумент66 страницRole and Function of Health Insurance IndiakkccommerceprojectОценок пока нет

- Sample Letter For Cancel A Letter of Credit .Документ1 страницаSample Letter For Cancel A Letter of Credit .srijayasampathОценок пока нет

- Ninjacart Sign MoU - 1Документ12 страницNinjacart Sign MoU - 1Tahir OmarОценок пока нет

- Business Profile SampleДокумент5 страницBusiness Profile SampleVinayОценок пока нет

- Loan PolicyДокумент5 страницLoan PolicySoumya BanerjeeОценок пока нет

- Jio Terms and ConditionsДокумент29 страницJio Terms and ConditionsRELIANCE JIOОценок пока нет

- Updated SME Luxe Proposal For Triforce GlobalДокумент21 страницаUpdated SME Luxe Proposal For Triforce GlobalallangreslyОценок пока нет

- Group 6 - Ethics in Pharmaceutical Industry..Документ15 страницGroup 6 - Ethics in Pharmaceutical Industry..rohanОценок пока нет

- UNIT 1 Core Banking Vs Allied Banking Activities AKG-1Документ21 страницаUNIT 1 Core Banking Vs Allied Banking Activities AKG-1A Walk To InfinityОценок пока нет

- IRDA Report 2018Документ235 страницIRDA Report 2018aaha74100% (1)

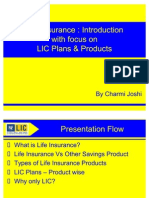

- LICДокумент8 страницLICCharmi Joshi100% (1)

- Star CompanyДокумент15 страницStar CompanyCandsz JcaОценок пока нет

- Article Tax Benefits For DisabledДокумент6 страницArticle Tax Benefits For DisabledMadhu KiranОценок пока нет

- Proposal NSDCДокумент2 страницыProposal NSDCDheeraj SaxenaОценок пока нет

- This MOU Is Made On 31-October-21Документ4 страницыThis MOU Is Made On 31-October-21udayОценок пока нет

- Benefits Summary PhilippinesДокумент2 страницыBenefits Summary PhilippinesRose GeeОценок пока нет

- Consent Form PDFДокумент1 страницаConsent Form PDFAshu Thakur50% (2)

- 4Ps of Ayurvedic ProductsДокумент3 страницы4Ps of Ayurvedic ProductsSreyasОценок пока нет

- Group Mediclaim Manual KingfisherДокумент5 страницGroup Mediclaim Manual KingfisherRajiv KumarОценок пока нет

- A Presentation On Mediassist ProcessДокумент19 страницA Presentation On Mediassist Processassaassa2351Оценок пока нет

- Guidelines Mediclaim L&TДокумент5 страницGuidelines Mediclaim L&Tnidnitrkl051296Оценок пока нет

- ASHP COVID 19 Evidence TableДокумент61 страницаASHP COVID 19 Evidence TablerehankhankhanОценок пока нет

- Schedule - Action Plan Q3, 2021 (Skype/Zoom Session) : Dates Day Rainbow SpectrumДокумент1 страницаSchedule - Action Plan Q3, 2021 (Skype/Zoom Session) : Dates Day Rainbow SpectrumrehankhankhanОценок пока нет

- License Required For PSD & Vector Images: December 27, 2019Документ2 страницыLicense Required For PSD & Vector Images: December 27, 2019rehankhankhanОценок пока нет

- Case Report: Timothy J Harkin, Kevin M Rurak, John Martins, Corey Eber, Arnold H Szporn, Mary Beth BeasleyДокумент3 страницыCase Report: Timothy J Harkin, Kevin M Rurak, John Martins, Corey Eber, Arnold H Szporn, Mary Beth BeasleyrehankhankhanОценок пока нет

- Room DiffДокумент2 страницыRoom DiffrehankhankhanОценок пока нет

- If Ppih Covid 19 RecommendationsДокумент6 страницIf Ppih Covid 19 RecommendationsrehankhankhanОценок пока нет

- Experiences With Ceftazidime in The Therapy of Neonatal InfectionsДокумент4 страницыExperiences With Ceftazidime in The Therapy of Neonatal InfectionsrehankhankhanОценок пока нет

- Dem Roster June 2015 NewДокумент3 страницыDem Roster June 2015 NewrehankhankhanОценок пока нет

- Cost Difference: Room Category Cost/Room No. of Participants 10,500 12 14,050Документ2 страницыCost Difference: Room Category Cost/Room No. of Participants 10,500 12 14,050rehankhankhanОценок пока нет

- Boy and His KiteertettДокумент1 страницаBoy and His KiteertettrehankhankhanОценок пока нет

- Attending a Wedding شادی کی تقریب PDFДокумент4 страницыAttending a Wedding شادی کی تقریب PDFrehankhankhanОценок пока нет

- Evaluating Resources Chapter 4Документ50 страницEvaluating Resources Chapter 4rehankhankhanОценок пока нет

- MCQsДокумент2 страницыMCQsrehankhankhanОценок пока нет

- Three Areas Where Business Schools FailДокумент2 страницыThree Areas Where Business Schools Failrehan_ku032031Оценок пока нет

- New Rehan KhanДокумент2 страницыNew Rehan KhanrehankhankhanОценок пока нет

- Furqan 2004Документ30 страницFurqan 2004rehankhankhanОценок пока нет

- HrsДокумент6 страницHrsrehankhankhanОценок пока нет

- AddisonДокумент6 страницAddisonrehankhankhanОценок пока нет

- Lec 3 WarehousingДокумент30 страницLec 3 Warehousingrehankhankhan100% (1)

- Furqan 2004Документ30 страницFurqan 2004rehankhankhanОценок пока нет

- Reliability: Case Processing SummaryДокумент18 страницReliability: Case Processing SummaryrehankhankhanОценок пока нет

- MasonДокумент2 страницыMasonrehankhankhanОценок пока нет

- Calcium and Its Role in HealthДокумент6 страницCalcium and Its Role in HealthrehankhankhanОценок пока нет

- TercicaДокумент1 страницаTercicarehankhankhanОценок пока нет

- IGCSE Biology (O610) Workbook: Balanced DietДокумент5 страницIGCSE Biology (O610) Workbook: Balanced DietPatrick Abidra100% (1)

- KEMH Guidelines On Cardiac Disease in PregnancyДокумент7 страницKEMH Guidelines On Cardiac Disease in PregnancyAyesha RazaОценок пока нет

- Snake Bite SOPДокумент5 страницSnake Bite SOPRaza Muhammad SoomroОценок пока нет

- NSTP Project Proposal 1Документ8 страницNSTP Project Proposal 1Laila J. Ignacio100% (2)

- Correlation Between Body Mass Index and Heart Rate in Males and Females of Different Age GroupДокумент7 страницCorrelation Between Body Mass Index and Heart Rate in Males and Females of Different Age GroupAdriel Jian NaldoОценок пока нет

- Asthma Case StudyДокумент39 страницAsthma Case StudyDimitris TasiouОценок пока нет

- Response To States 4.2 Motion in Limine Character of VictimДокумент10 страницResponse To States 4.2 Motion in Limine Character of VictimLaw of Self DefenseОценок пока нет

- Therapeutic Relationship Is Between Therapist and Patient and Has Always Been Viewed As SacredДокумент3 страницыTherapeutic Relationship Is Between Therapist and Patient and Has Always Been Viewed As Sacredcbargrad100% (1)

- MiraMate Light Pad InstructionsДокумент8 страницMiraMate Light Pad InstructionsLaurentMartinonОценок пока нет

- Sarah J. (Englert) Dunham RN, BSN, MS, FNPДокумент3 страницыSarah J. (Englert) Dunham RN, BSN, MS, FNPapi-309264509Оценок пока нет

- Rachel Tucker Resume 2020Документ1 страницаRachel Tucker Resume 2020api-489845523Оценок пока нет

- Disability MatrixДокумент21 страницаDisability MatrixAngelika MendozaОценок пока нет

- Hazard Analysis in The WorkplaceДокумент7 страницHazard Analysis in The WorkplaceUghlahnОценок пока нет

- Polytechnic of Health Denpasar Is An Institution of Higher Education Official of The Department of Health Which Is The Technical Implementation UnitДокумент1 страницаPolytechnic of Health Denpasar Is An Institution of Higher Education Official of The Department of Health Which Is The Technical Implementation UnitDewi PradnyaniОценок пока нет

- Presentation 1Документ16 страницPresentation 1Azhari AhmadОценок пока нет

- Urtikaria Pada Perempuan Usia 39 Tahun: Laporan Kasus: Moh. Wahid Agung, Diany Nurdin, M. SabirДокумент5 страницUrtikaria Pada Perempuan Usia 39 Tahun: Laporan Kasus: Moh. Wahid Agung, Diany Nurdin, M. SabirZakia AjaОценок пока нет

- Covid-19 RT-PCR Test Report & Certification: Certificate IssuedДокумент1 страницаCovid-19 RT-PCR Test Report & Certification: Certificate IssuedJerome OliverosОценок пока нет

- Back Pain During PregnancyДокумент3 страницыBack Pain During PregnancyDr. Sadhana KalaОценок пока нет

- Predicting and Controlling Influenza Outbreaks - Published Article - IJERSTE - Vol.12 Issue 2, Feb 2023Документ4 страницыPredicting and Controlling Influenza Outbreaks - Published Article - IJERSTE - Vol.12 Issue 2, Feb 2023dimple kharwarОценок пока нет

- Tcharestresumefinal 1009Документ2 страницыTcharestresumefinal 1009tcharestОценок пока нет

- 2008 04 Lecture 1 Interface Dermatitis FrishbergДокумент6 страниц2008 04 Lecture 1 Interface Dermatitis FrishbergYudistra R ShafarlyОценок пока нет

- Hirschsprung NCM 109 Case PresentationДокумент10 страницHirschsprung NCM 109 Case PresentationValerie LeddaОценок пока нет

- ESI ER CompleteДокумент45 страницESI ER Completetammy2121Оценок пока нет

- Blood and Tissue Flagellates BSCДокумент27 страницBlood and Tissue Flagellates BSCSisay FentaОценок пока нет

- AcupunctureДокумент10 страницAcupunctureAngel Iulian Popescu0% (2)

- Pharmacy Job InterviewQuestionsДокумент4 страницыPharmacy Job InterviewQuestionsRadha MandapalliОценок пока нет

- Types Causes Signs and Symptomps Intellectual DisabilityДокумент2 страницыTypes Causes Signs and Symptomps Intellectual DisabilityMae Ann Jean JustolОценок пока нет

- Trail Mix Cookies IKДокумент24 страницыTrail Mix Cookies IKDwi Intan WОценок пока нет

- OrphenadrineДокумент4 страницыOrphenadrineGermin CesaОценок пока нет

- Pathophysiology of Neonatal Sepsis Secondary To Neonatal PneumoniaДокумент4 страницыPathophysiology of Neonatal Sepsis Secondary To Neonatal Pneumoniapaul andrew laranjo asuncion80% (5)