Вам также может понравиться

- JKR SPJ 2008 S4Документ187 страницJKR SPJ 2008 S4Ifkar AzmiОценок пока нет

- Industrial Training Report 2017: Name Matrix NoДокумент2 страницыIndustrial Training Report 2017: Name Matrix NosaifulsabdinОценок пока нет

- DWF 1 - Api PrecastДокумент2 страницыDWF 1 - Api PrecastsaifulsabdinОценок пока нет

- AS-BUILT SLOPE GRADIENT LEVEL 5EK-Layout2Документ1 страницаAS-BUILT SLOPE GRADIENT LEVEL 5EK-Layout2saifulsabdinОценок пока нет

- Atm Precast SDN BHD: L Shape Main Trunk Drain With SB 2700mm (H) X2700mm (W) X1.0m (L)Документ1 страницаAtm Precast SDN BHD: L Shape Main Trunk Drain With SB 2700mm (H) X2700mm (W) X1.0m (L)saifulsabdinОценок пока нет

- Is CCC The Only Contractual Requirement For The Delivery of VP in A Sales and Purchase AgreementДокумент3 страницыIs CCC The Only Contractual Requirement For The Delivery of VP in A Sales and Purchase AgreementRidha Razak100% (2)

- Pavement DistressДокумент64 страницыPavement DistressTrigger DineshОценок пока нет

- QUESTION 5 CEM SOCIETY (Complete)Документ2 страницыQUESTION 5 CEM SOCIETY (Complete)saifulsabdinОценок пока нет

- Research SummaryДокумент1 страницаResearch SummarysaifulsabdinОценок пока нет

- PDA Method Statement For Micropile-Raked PileДокумент7 страницPDA Method Statement For Micropile-Raked PilesaifulsabdinОценок пока нет

- Thiesson Polygon Method ExerciseДокумент1 страницаThiesson Polygon Method ExercisesaifulsabdinОценок пока нет

- Graph of Metacentric Height VS Angular Displacement (Left)Документ2 страницыGraph of Metacentric Height VS Angular Displacement (Left)saifulsabdinОценок пока нет

- Pavement DistressДокумент1 страницаPavement DistresssaifulsabdinОценок пока нет

- Flexible Pavement DistressДокумент13 страницFlexible Pavement DistressrajudeenОценок пока нет

- Tutorial 2Документ2 страницыTutorial 2saifulsabdin0% (1)

- (Please Ensure All The Components in This Table Are Inline) Endorsement by SV Panel 1 Panel 2 Objective 1Документ1 страница(Please Ensure All The Components in This Table Are Inline) Endorsement by SV Panel 1 Panel 2 Objective 1saifulsabdinОценок пока нет

- Thiesson Polygon Method ExerciseДокумент1 страницаThiesson Polygon Method ExercisesaifulsabdinОценок пока нет

- CEW541 Tutorial 1Документ2 страницыCEW541 Tutorial 1redz00Оценок пока нет

- Pavement DistressДокумент64 страницыPavement DistressTrigger DineshОценок пока нет

- AppendicesДокумент2 страницыAppendicessaifulsabdinОценок пока нет

- APPENDICESДокумент2 страницыAPPENDICESsaifulsabdinОценок пока нет

- Table of ContentДокумент1 страницаTable of ContentsaifulsabdinОценок пока нет

- Lesson Plan CEW532 MARCH-JULY2017 PDFДокумент3 страницыLesson Plan CEW532 MARCH-JULY2017 PDFsaifulsabdinОценок пока нет

- Lab Manual Cew532 - Sept2015-Jan2016Документ15 страницLab Manual Cew532 - Sept2015-Jan2016saifulsabdinОценок пока нет

- Manual Oel Ver 1 May 2013Документ60 страницManual Oel Ver 1 May 2013saifulsabdinОценок пока нет

- TorsionДокумент4 страницыTorsionsaifulsabdinОценок пока нет

- Level 1 (PRINT)Документ34 страницыLevel 1 (PRINT)saifulsabdinОценок пока нет

- MANUAL WORDsДокумент67 страницMANUAL WORDssaifulsabdinОценок пока нет

- Us 2612854Документ5 страницUs 2612854saifulsabdinОценок пока нет

- Diagnostic Test Ces 511 (Answer Sceme)Документ4 страницыDiagnostic Test Ces 511 (Answer Sceme)saifulsabdinОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Corporate Governance Government MeasuresДокумент9 страницCorporate Governance Government MeasurestawandaОценок пока нет

- 1060-2022 PO ATL M.S Bismillah AccessoriesДокумент1 страница1060-2022 PO ATL M.S Bismillah AccessoriesYounus SheikhОценок пока нет

- Adwords Fundamental Exam Questions Answers 2016Документ21 страницаAdwords Fundamental Exam Questions Answers 2016Avinash VermaОценок пока нет

- BridgestoneДокумент1 страницаBridgestoneRam JainОценок пока нет

- Salesforce Blog Article - Lightning Bolt TrailblazersДокумент4 страницыSalesforce Blog Article - Lightning Bolt TrailblazersBayCreativeОценок пока нет

- Budget Circular No 2018 4 PDFДокумент245 страницBudget Circular No 2018 4 PDFJoey Villas MaputiОценок пока нет

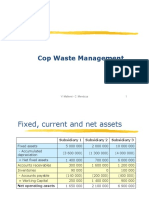

- Cop Waste Management SolutionДокумент5 страницCop Waste Management SolutionPaul GhanimehОценок пока нет

- H. Aronson & Co., Inc. v. Associated Labor UnionДокумент4 страницыH. Aronson & Co., Inc. v. Associated Labor UnionChing ApostolОценок пока нет

- Substantive Procedures For Sales RevenueДокумент5 страницSubstantive Procedures For Sales RevenuePubg DonОценок пока нет

- Doing Business in BruneiДокумент67 страницDoing Business in BruneiAyman MehassebОценок пока нет

- Brand ManagementДокумент172 страницыBrand ManagementNusrat JahanОценок пока нет

- Bodie Investments 12e IM CH23Документ3 страницыBodie Investments 12e IM CH23lexon_kbОценок пока нет

- Accreditation Is Not:: Benefits of Accreditation To The Accredited Conformity Assessment BodyДокумент5 страницAccreditation Is Not:: Benefits of Accreditation To The Accredited Conformity Assessment BodyFanilo RazafindralamboОценок пока нет

- Tutorial Letter 102/3/2020: Forms of Business EnterprisesДокумент15 страницTutorial Letter 102/3/2020: Forms of Business EnterprisesXolisaОценок пока нет

- Activity 1:: Date Account Titles and Explanation P.R. Debit CreditДокумент3 страницыActivity 1:: Date Account Titles and Explanation P.R. Debit Creditemem resuentoОценок пока нет

- Session 31Документ25 страницSession 31Yashwanth Reddy AnumulaОценок пока нет

- BMC Colg WorkДокумент3 страницыBMC Colg Workvishal sinhaОценок пока нет

- A Case Study On RIL vs. RNRL DisputeДокумент6 страницA Case Study On RIL vs. RNRL DisputeAparajita SharmaОценок пока нет

- WEEK 6 Seminar Q&AsДокумент26 страницWEEK 6 Seminar Q&AsMeenakshi SinhaОценок пока нет

- Service MarketingДокумент21 страницаService MarketingKunwar AdityaОценок пока нет

- Rapport Annuel Awb - Vangl PDFДокумент86 страницRapport Annuel Awb - Vangl PDFcasaОценок пока нет

- Strategic Management MCQ and Answers For MBA StudentsДокумент11 страницStrategic Management MCQ and Answers For MBA Studentsmarieieiem100% (3)

- (A) Was Entering The Indian Market With A Standardised Product A Mistake? JustifyДокумент6 страниц(A) Was Entering The Indian Market With A Standardised Product A Mistake? JustifyShanoJeeОценок пока нет

- Auditing and Investigation Acc 412Документ7 страницAuditing and Investigation Acc 412saidsulaiman2095Оценок пока нет

- Distribution Network DesignДокумент18 страницDistribution Network DesignAnik AlamОценок пока нет

- Peachtree AccountingДокумент170 страницPeachtree AccountingKyaw Moe Hain100% (4)

- Tourism Market ResearchДокумент14 страницTourism Market ResearchLoping Lee100% (1)

- DisposalДокумент107 страницDisposaljohnisflyОценок пока нет

- Q&A InvestorДокумент2 страницыQ&A Investorjns1992Оценок пока нет

- EIU Research Proposal Approval Form - Updated 2Документ20 страницEIU Research Proposal Approval Form - Updated 2RozhanОценок пока нет