Вам также может понравиться

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Rocker Lab BurnerДокумент1 страницаRocker Lab BurnerIsma VelascoОценок пока нет

- Request For Complete DeliveryДокумент1 страницаRequest For Complete DeliveryIsma VelascoОценок пока нет

- 1 OBMC Biographical Data FillableДокумент6 страниц1 OBMC Biographical Data FillableIsma VelascoОценок пока нет

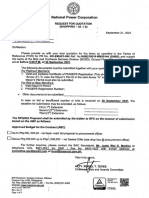

- Napocor Neco RFQ - Ho-Ema21-006 (Shb2), Ref No. Shb210519-Rm00145 (Shb2)Документ5 страницNapocor Neco RFQ - Ho-Ema21-006 (Shb2), Ref No. Shb210519-Rm00145 (Shb2)Isma VelascoОценок пока нет

- Napocor - Neco RFQ - Ho-Ema21-004 (Shb2)Документ5 страницNapocor - Neco RFQ - Ho-Ema21-004 (Shb2)Isma VelascoОценок пока нет

- Bid FormДокумент12 страницBid FormIsma VelascoОценок пока нет

- PhilFIDA QuotationДокумент1 страницаPhilFIDA QuotationIsma VelascoОценок пока нет

- Budget Circular No 2018 4 PDFДокумент245 страницBudget Circular No 2018 4 PDFJoey Villas MaputiОценок пока нет

- MenuДокумент12 страницMenuJhanelyn V. InopiaОценок пока нет

- Sponsor ChecklistДокумент3 страницыSponsor ChecklistIsma VelascoОценок пока нет

- Duties and ResponsibilitiesДокумент2 страницыDuties and ResponsibilitiesIsma VelascoОценок пока нет

- Announcement Coast Guard Medical DoctorДокумент1 страницаAnnouncement Coast Guard Medical DoctorArron BuenavistaОценок пока нет

- DPAДокумент48 страницDPAIsma VelascoОценок пока нет

- National Museum of The Philippines: Duties and ResponsibilitiesДокумент4 страницыNational Museum of The Philippines: Duties and ResponsibilitiesIsma VelascoОценок пока нет

- Duties and ResponsibilitiesДокумент2 страницыDuties and ResponsibilitiesIsma VelascoОценок пока нет

- September 21 2016Документ2 страницыSeptember 21 2016Isma VelascoОценок пока нет

- BRL Files 2011 10 BRL EthanolfermentationДокумент12 страницBRL Files 2011 10 BRL EthanolfermentationcarolineОценок пока нет

- Pcoduties PDFДокумент1 страницаPcoduties PDFIsma VelascoОценок пока нет

- Biosafety Regulation in The PhilippinesДокумент49 страницBiosafety Regulation in The PhilippinesKim DayagОценок пока нет

- DPAДокумент48 страницDPAIsma VelascoОценок пока нет

- 2013 Fermentation CalculationsДокумент1 страница2013 Fermentation Calculationsskipperz_10Оценок пока нет

- PRESERVATIVESДокумент2 страницыPRESERVATIVESIsma VelascoОценок пока нет

- LetterДокумент2 страницыLetterIsma VelascoОценок пока нет

- Summary of Inventory (Chemicals) Item No. Name Beginning PurchasesДокумент8 страницSummary of Inventory (Chemicals) Item No. Name Beginning PurchasesIsma VelascoОценок пока нет

- MemoДокумент1 страницаMemoIsma VelascoОценок пока нет

- Item Description Quantit Y Amount TotalДокумент2 страницыItem Description Quantit Y Amount TotalIsma VelascoОценок пока нет

- Inventory NovemberДокумент34 страницыInventory NovemberIsma VelascoОценок пока нет

- My Adventures in PalawanДокумент11 страницMy Adventures in PalawanIsma VelascoОценок пока нет

- Science Mathematics Pilipino Araling Panlipunan English E.S.P M.T.B MapehДокумент11 страницScience Mathematics Pilipino Araling Panlipunan English E.S.P M.T.B MapehIsma VelascoОценок пока нет

- Inventory July 2014Документ32 страницыInventory July 2014Isma VelascoОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (120)

- Ho Arts 7Документ3 страницыHo Arts 7Michelle Anne Legaspi Bawar75% (4)

- National Forest Policy ComaparisonДокумент28 страницNational Forest Policy ComaparisonYogender Sharma100% (1)

- South Indian Villages FinalДокумент17 страницSouth Indian Villages FinalRichard ClarkeОценок пока нет

- Final Portfolio JosemarieamadoДокумент68 страницFinal Portfolio JosemarieamadoSumbungan Ng Brgy TaraОценок пока нет

- FAO Strategy For Partnerships With Private SectorДокумент36 страницFAO Strategy For Partnerships With Private SectorLeonardo AguilarОценок пока нет

- Samos: A Tourist Guide in EnglishДокумент36 страницSamos: A Tourist Guide in EnglishMy Samos Blog100% (2)

- Chen 2013 Use in CHinaДокумент10 страницChen 2013 Use in CHinaKimОценок пока нет

- Indonesia Seaweed Companies ProfileДокумент21 страницаIndonesia Seaweed Companies ProfileMohammadAlfinWidyanto100% (1)

- Chapter - 6 Natural Vegetation of IndiaДокумент9 страницChapter - 6 Natural Vegetation of IndiaMansha ChhetriОценок пока нет

- NCERT Class 6 ScienceДокумент167 страницNCERT Class 6 ScienceKrishna Tripathi0% (1)

- Minor Project ArkaДокумент32 страницыMinor Project ArkaArka ChakrabortyОценок пока нет

- Ifea 248781Документ31 страницаIfea 248781ArqueologoОценок пока нет

- Catalogo Mataderos y Salas (Español-Inglés)Документ24 страницыCatalogo Mataderos y Salas (Español-Inglés)José Pablo Solano GómezОценок пока нет

- Piñatex Intro Card - A5Документ1 страницаPiñatex Intro Card - A5Samuel Arévalo GОценок пока нет

- Puno (C.J., Chairperson), Carpio, Azcuna JJ. Petition Granted, Assailed Decision Partially ModifiedДокумент49 страницPuno (C.J., Chairperson), Carpio, Azcuna JJ. Petition Granted, Assailed Decision Partially ModifiedVirnadette LopezОценок пока нет

- PDF Version of The NovelДокумент463 страницыPDF Version of The NovelSarita SinghОценок пока нет

- Second Practice First Partial English III - Katherinne BernardДокумент5 страницSecond Practice First Partial English III - Katherinne BernardKathe BernardОценок пока нет

- Pds-Cassida Rls GR 0Документ3 страницыPds-Cassida Rls GR 0Milena GonzalezОценок пока нет

- 11 Test 1plant KingdomДокумент3 страницы11 Test 1plant KingdomJaskirat SinghОценок пока нет

- Ma. Aika S. Doronela 2015-10952 CRSC U-2LДокумент5 страницMa. Aika S. Doronela 2015-10952 CRSC U-2LMaika DoronelaОценок пока нет

- (Geoffrey Lawrence, Kristen Lyons, Tabatha Walling (BookFi) PDFДокумент321 страница(Geoffrey Lawrence, Kristen Lyons, Tabatha Walling (BookFi) PDFIManОценок пока нет

- Review of Related LiteratureДокумент2 страницыReview of Related LiteratureVince ManahanОценок пока нет

- Coffee in Bangladesh (Done)Документ2 страницыCoffee in Bangladesh (Done)Towsif rashid0% (1)

- TangeloДокумент2 страницыTangeloAZIZRAHMANABUBAKARОценок пока нет

- Growing Kiwifruit: PNW 507 - Reprinted September 2000 $2.50Документ24 страницыGrowing Kiwifruit: PNW 507 - Reprinted September 2000 $2.50conkonagyОценок пока нет

- Genetic Modification and Gene Editing PPT 1416wfcfДокумент13 страницGenetic Modification and Gene Editing PPT 1416wfcfMeowОценок пока нет

- 1.1 Reference Crop Evapotranspiration, EtoДокумент20 страниц1.1 Reference Crop Evapotranspiration, EtoDamalash kabaОценок пока нет

- Soil FungiДокумент1 страницаSoil FungiDimasalang PerezОценок пока нет

- The Vision School System ChakwalДокумент2 страницыThe Vision School System ChakwalmathswithquratОценок пока нет

- RPP Perekaman Bunga Putri Maulia-Converted-CompressedДокумент8 страницRPP Perekaman Bunga Putri Maulia-Converted-CompressedFauzi SulthonОценок пока нет