Вам также может понравиться

- Finance Jobs ReportДокумент22 страницыFinance Jobs Reportvincenzo21010Оценок пока нет

- Zoning Inspector Trainee: Passbooks Study GuideОт EverandZoning Inspector Trainee: Passbooks Study GuideОценок пока нет

- Making Money Out of Thin Air: Salesteamlive Special ReportДокумент8 страницMaking Money Out of Thin Air: Salesteamlive Special ReportThomas SettleОценок пока нет

- Credit Policy PDFДокумент4 страницыCredit Policy PDFMichaelsam100% (1)

- Advantages of Trade CreditДокумент22 страницыAdvantages of Trade CredityadavgunwalОценок пока нет

- Loan Processing or Underwriting Customer Service (Call Center) oДокумент4 страницыLoan Processing or Underwriting Customer Service (Call Center) oapi-76958881Оценок пока нет

- The Fastest Way To Become A Property Expert GuaranteedДокумент94 страницыThe Fastest Way To Become A Property Expert GuaranteedGrahamОценок пока нет

- Employee Retention Credit: Covid-19 Business SupportДокумент1 страницаEmployee Retention Credit: Covid-19 Business SupportMini NavarroОценок пока нет

- E-Banking Delivery Channels and ApplicationsДокумент45 страницE-Banking Delivery Channels and ApplicationsAditi MangalОценок пока нет

- Cash and Marketable Securities MGTДокумент16 страницCash and Marketable Securities MGTAldrin ZolinaОценок пока нет

- Four Steps To Government RegistrationsДокумент7 страницFour Steps To Government RegistrationsJustin HansenОценок пока нет

- Debt Consolidation TipsДокумент6 страницDebt Consolidation TipsKrittiОценок пока нет

- Maverick Lending - ERTC Credit One PagerДокумент1 страницаMaverick Lending - ERTC Credit One PagerKenton ChikОценок пока нет

- Digital Billboards Pose Serious Highway Safety and Environmental RisksДокумент19 страницDigital Billboards Pose Serious Highway Safety and Environmental Risksmiss_mkccОценок пока нет

- Yardi 102: I. Module I OverviewДокумент4 страницыYardi 102: I. Module I OverviewmanagerОценок пока нет

- Marketing Strategies For Mortgage Lenders and BrokersДокумент2 страницыMarketing Strategies For Mortgage Lenders and BrokersTodd Lake100% (7)

- Flip & Gap First Position Funding (FGFPF) Processing Application FormДокумент5 страницFlip & Gap First Position Funding (FGFPF) Processing Application FormDarnell WoodardОценок пока нет

- Contingent consideration-PWCДокумент23 страницыContingent consideration-PWCKath OОценок пока нет

- Kathleen Coggin S: Administrative AssistantДокумент2 страницыKathleen Coggin S: Administrative AssistantRubayet Hasan RobiОценок пока нет

- The 7 Key Functions of a Central BankДокумент23 страницыThe 7 Key Functions of a Central BankRehan AhmadОценок пока нет

- Real Estate Valuation and Strategy: A Guide for Family Offices and Their AdvisorsОт EverandReal Estate Valuation and Strategy: A Guide for Family Offices and Their AdvisorsОценок пока нет

- Easy Creative Financing Techniques With Quick ClosesДокумент3 страницыEasy Creative Financing Techniques With Quick Closesmel fellerОценок пока нет

- Factoring in Finance ArrangementsДокумент9 страницFactoring in Finance Arrangementsduncanmac200777Оценок пока нет

- The ABCs of Agency (2018)Документ2 страницыThe ABCs of Agency (2018)Angel KnightОценок пока нет

- The Future of Invoice FinancingДокумент5 страницThe Future of Invoice FinancingSingapore Green Building Council100% (1)

- Mortgage Loan BasicsДокумент7 страницMortgage Loan BasicsJyoti SinghОценок пока нет

- Introduction To Private Equity - SeminarДокумент171 страницаIntroduction To Private Equity - Seminarapritul3539Оценок пока нет

- Business Law Presentation FINALДокумент24 страницыBusiness Law Presentation FINALNur Liyana Izzati Roslan100% (1)

- Short Sale Seminar Bakersfield, CAДокумент22 страницыShort Sale Seminar Bakersfield, CAMiguel GarciaОценок пока нет

- Property Scout Introduction - Prospecting For ProfitsДокумент12 страницProperty Scout Introduction - Prospecting For ProfitsMichael Durden100% (1)

- Fix & Flip ProgramsДокумент2 страницыFix & Flip ProgramsDarnellОценок пока нет

- Mobile Home Goldmine: Unlocking Profits In The Mobile Home Real Estate Market: A Comprehensive Guide To Investing, Buying, Selling and Managing Mobile Home Parks For Maximum ReturnsОт EverandMobile Home Goldmine: Unlocking Profits In The Mobile Home Real Estate Market: A Comprehensive Guide To Investing, Buying, Selling and Managing Mobile Home Parks For Maximum ReturnsОценок пока нет

- Accounts Receivable Process Diagnostic QuestionnaireДокумент13 страницAccounts Receivable Process Diagnostic QuestionnaireRodney LabayОценок пока нет

- Finance and Mortgage Broking: Useful WebsitesДокумент6 страницFinance and Mortgage Broking: Useful WebsitesForin NeimОценок пока нет

- Airbnb Business: Net Income 10,100.00Документ2 страницыAirbnb Business: Net Income 10,100.00Angelo InabanganОценок пока нет

- The Investment Handbook: A one-stop guide to investment, capital and business: The Essential Funding Guide for EntrepreneursОт EverandThe Investment Handbook: A one-stop guide to investment, capital and business: The Essential Funding Guide for EntrepreneursОценок пока нет

- Bizmanualz Banking Management Policies and Procedures SampleДокумент6 страницBizmanualz Banking Management Policies and Procedures SampleYe PhoneОценок пока нет

- Discover Unreported Income for Cash BusinessesДокумент15 страницDiscover Unreported Income for Cash BusinesseskiracimaoОценок пока нет

- Crash CourseДокумент83 страницыCrash CourseJuan Edward LeonОценок пока нет

- Credit Analyst Resume Samples - Velvet Jobs1Документ140 страницCredit Analyst Resume Samples - Velvet Jobs1poseiОценок пока нет

- Off Shore CompaniesДокумент9 страницOff Shore Companieskainat safdarОценок пока нет

- PNC First-Time Homebuyer's GuideДокумент7 страницPNC First-Time Homebuyer's GuideKent Richardson100% (1)

- IDC Direct Lender HandbookДокумент17 страницIDC Direct Lender HandbookDirectorОценок пока нет

- The Ultimate Guide: For SuccessfullyДокумент27 страницThe Ultimate Guide: For SuccessfullyCarolОценок пока нет

- Mortgage App Form 1003Документ5 страницMortgage App Form 1003api-305651288Оценок пока нет

- Icsc 2012Документ117 страницIcsc 2012Pareeksha ScribdОценок пока нет

- Divas Book Club BylawsДокумент4 страницыDivas Book Club Bylawsapi-243468771Оценок пока нет

- Redemption of Reward Points Towards Card Outstanding & Air MilesДокумент3 страницыRedemption of Reward Points Towards Card Outstanding & Air MilesNagasankethОценок пока нет

- Depreciation EbookДокумент24 страницыDepreciation EbookAdrianОценок пока нет

- Treasury Operations In Turkey and Contemporary Sovereign Treasury ManagementОт EverandTreasury Operations In Turkey and Contemporary Sovereign Treasury ManagementОценок пока нет

- Event Ticket SalesДокумент15 страницEvent Ticket SalesAnakinОценок пока нет

- Money and Monetary Policy Spring 2003Документ47 страницMoney and Monetary Policy Spring 2003moneyedkenya100% (1)

- Avex Loan ProcessingДокумент12 страницAvex Loan ProcessingSandy KondaОценок пока нет

- Domain Names Beginners Guide 06dec10 enДокумент18 страницDomain Names Beginners Guide 06dec10 enanujvasistha28Оценок пока нет

- Esb Sqlint 2Документ52 страницыEsb Sqlint 2Anoop TejeswiОценок пока нет

- Domain Names Beginners Guide 06dec10 enДокумент18 страницDomain Names Beginners Guide 06dec10 enanujvasistha28Оценок пока нет

- Esb Sqlint 2Документ52 страницыEsb Sqlint 2Anoop TejeswiОценок пока нет

- China Banking Corp vs QBRO Fishing Enterprises Supreme Court RulingДокумент2 страницыChina Banking Corp vs QBRO Fishing Enterprises Supreme Court RulingRey Almon Tolentino AlibuyogОценок пока нет

- COMPLAINT Victor JohnsonДокумент38 страницCOMPLAINT Victor JohnsonBernie KimmerleОценок пока нет

- Role of Mortgage Finance Institutions in NigeriaДокумент68 страницRole of Mortgage Finance Institutions in NigeriaCrystalОценок пока нет

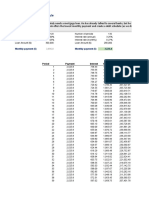

- 3.2 70. Exercise Loan Schedule SolvedДокумент6 страниц3.2 70. Exercise Loan Schedule SolvedAniket KarnОценок пока нет

- Ramos V Court of AppealsДокумент2 страницыRamos V Court of AppealsBeya Marie F. AmaroОценок пока нет

- Osceola-Possible Fraud ForeclosuresДокумент15 страницOsceola-Possible Fraud ForeclosuresRicharnellia-RichieRichBattiest-Collins100% (1)

- Example of Bank Witness List With 62 NamesДокумент6 страницExample of Bank Witness List With 62 NamesForeclosure FraudОценок пока нет

- CFPB Foreclosure Avoidance ProceduresДокумент2 страницыCFPB Foreclosure Avoidance ProceduresunapantherОценок пока нет

- SSO 1plusДокумент1 страницаSSO 1plusashuОценок пока нет

- Sample-Loan Commitment LetterДокумент3 страницыSample-Loan Commitment LetterJustice Williams100% (1)

- Assignment of Deed of TrustДокумент2 страницыAssignment of Deed of TrustChariseB2012Оценок пока нет

- House Hearing, 113TH Congress - Examining The Proper Role of The Federal Housing Administration in Our Mortgage Insurance MarketДокумент206 страницHouse Hearing, 113TH Congress - Examining The Proper Role of The Federal Housing Administration in Our Mortgage Insurance MarketScribd Government DocsОценок пока нет

- Branch Advance MasterДокумент294 страницыBranch Advance MasterSurajit DoraОценок пока нет

- TMK Ms-Excel Example 01: 43594050.Xls OmegasoapsДокумент18 страницTMK Ms-Excel Example 01: 43594050.Xls OmegasoapsmohkristОценок пока нет

- Caltex Vs IacДокумент2 страницыCaltex Vs Iacmar corОценок пока нет

- Agreement For Pawning A Car in Mid-InstallmentsДокумент2 страницыAgreement For Pawning A Car in Mid-InstallmentsCath TesoroОценок пока нет

- Assignment BALLB 5th Sem PDFДокумент2 страницыAssignment BALLB 5th Sem PDFPRABHAKAR KUMARОценок пока нет

- Keri Selman Robo-Signer ExtraordinaireДокумент3 страницыKeri Selman Robo-Signer ExtraordinaireForeclosure FraudОценок пока нет

- Icici Bank Home Finance Limited - Kandepu Subhash ChandraboseДокумент3 страницыIcici Bank Home Finance Limited - Kandepu Subhash ChandraboseBhanu GОценок пока нет

- Foreclosure Fraud For DummiesДокумент15 страницForeclosure Fraud For DummiesPhilОценок пока нет

- Credit Samplex For Finals SerranoДокумент1 страницаCredit Samplex For Finals SerranoShanelle NapolesОценок пока нет

- 07-Oct. ..... (Nilam...Документ3 страницы07-Oct. ..... (Nilam...krishna vermaОценок пока нет

- Real Estate Acronyms Guide for ProfessionalsДокумент2 страницыReal Estate Acronyms Guide for Professionalselkeb89Оценок пока нет

- FRAДокумент8 страницFRArajashreekini13Оценок пока нет

- Organizational Structure – Lending & Liabilities at a Leading BankДокумент3 страницыOrganizational Structure – Lending & Liabilities at a Leading BankMohit KumarОценок пока нет

- Finding Fraud in The Loan DocumentsДокумент3 страницыFinding Fraud in The Loan Documentsrodclassteam100% (1)

- The District Cooperative Central Bank LTD., Medak H.O. SangareddyДокумент2 страницыThe District Cooperative Central Bank LTD., Medak H.O. SangareddyPonnam VenkateshamОценок пока нет

- Loan Amortization Schedule ExplainedДокумент8 страницLoan Amortization Schedule ExplainedamarantineОценок пока нет

- Barbour vs. FinkeДокумент9 страницBarbour vs. FinkeMariella Grace AllanicОценок пока нет

- Deed of Substituted Security - BOS - HalifaxДокумент2 страницыDeed of Substituted Security - BOS - HalifaxDamian MikaОценок пока нет