Вам также может понравиться

- Preventing Bail Out of BanksДокумент1 страницаPreventing Bail Out of BanksRavi GuptaОценок пока нет

- 2 ISC Syllabus RegulationsДокумент12 страниц2 ISC Syllabus RegulationsShubham DhingraОценок пока нет

- Capital Adequacy RatioДокумент2 страницыCapital Adequacy RatioRavi GuptaОценок пока нет

- 121 How To Build A TM ClubДокумент33 страницы121 How To Build A TM ClubRavi GuptaОценок пока нет

- Wireless Notes Unit 3Документ10 страницWireless Notes Unit 3Ravi Gupta50% (2)

- Complete Guide to MS in US UniversitiesДокумент11 страницComplete Guide to MS in US UniversitiesManu RavindraОценок пока нет

- Uttaranchal Obc ListДокумент3 страницыUttaranchal Obc ListRavi GuptaОценок пока нет

- Strumming 1Документ1 страницаStrumming 1Ravi GuptaОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- The General Ledger and Financial Reporting CycleДокумент12 страницThe General Ledger and Financial Reporting CycleNHОценок пока нет

- Jurnal Tesis Muhamad Rifki SeptiadiДокумент14 страницJurnal Tesis Muhamad Rifki Septiadirifki muhamadОценок пока нет

- Reporting and Analyzing Receivables EntriesДокумент4 страницыReporting and Analyzing Receivables Entriesmohammad khataybehОценок пока нет

- Trading in Financial Markets: Lecture 2aДокумент34 страницыTrading in Financial Markets: Lecture 2aPhương KiềuОценок пока нет

- Important Yt LinksДокумент3 страницыImportant Yt Linksrosesingh00610Оценок пока нет

- 96th RMFI Questions AnalysisДокумент4 страницы96th RMFI Questions Analysischayon mondolОценок пока нет

- Internship in Banking SIP ReportДокумент101 страницаInternship in Banking SIP ReportDaniel PedrosaОценок пока нет

- Overage Vessel Approval FormДокумент2 страницыOverage Vessel Approval Formgp_shortnsweetОценок пока нет

- Introduction To Securities and InvestmentДокумент26 страницIntroduction To Securities and InvestmentJerome GaliciaОценок пока нет

- Advanced Accounting Chapter 06 2021Документ117 страницAdvanced Accounting Chapter 06 2021Uzzaam HaiderОценок пока нет

- Cash FlowsДокумент10 страницCash FlowsNuha RehnumaОценок пока нет

- Accounting MTP Question Series I 1676966561047406Документ9 страницAccounting MTP Question Series I 1676966561047406Tushar MittalОценок пока нет

- Acctg 14 - Midterm Lesson Part3Документ21 страницаAcctg 14 - Midterm Lesson Part3NANОценок пока нет

- Trackage Scheme Tickets 118777Документ4 страницыTrackage Scheme Tickets 118777Rodianne Ellul BuhagiarОценок пока нет

- Functions of Banking Sectors in Bangladesh.Документ2 страницыFunctions of Banking Sectors in Bangladesh.Omar FarukОценок пока нет

- Cash Management - Overview Slide For TTT - 15.0 - PTJ Ao (Cmsi v1.0)Документ63 страницыCash Management - Overview Slide For TTT - 15.0 - PTJ Ao (Cmsi v1.0)Siti Habsah Abdullah100% (1)

- Cashier Check TemplateДокумент1 страницаCashier Check TemplateNicholas GarrisonОценок пока нет

- Islamic Pawnshop FinalДокумент14 страницIslamic Pawnshop FinalSaadat ShaikhОценок пока нет

- Citi Regulatory Mindmap Hedge Funds NorthAmerica Nov 2012Документ1 страницаCiti Regulatory Mindmap Hedge Funds NorthAmerica Nov 2012adee_adityaОценок пока нет

- Accounts and Finance For BankersДокумент5 страницAccounts and Finance For BankersneevcoachingОценок пока нет

- 8 Column Worksheet TemplateДокумент12 страниц8 Column Worksheet TemplateJefferson ManingdingОценок пока нет

- Non Performing AssetsДокумент60 страницNon Performing AssetsChitra Suresh AchariiОценок пока нет

- FA Lesson 1 Checking AccountДокумент5 страницFA Lesson 1 Checking Accountludy louisОценок пока нет

- Assets Liabilities & Net Worth: Check 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 28,127Документ7 страницAssets Liabilities & Net Worth: Check 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 28,127Sofía MargaritaОценок пока нет

- Cgssi One Pager About Eligibilty Checks PDFДокумент1 страницаCgssi One Pager About Eligibilty Checks PDFaefewОценок пока нет

- Final Project Neft Rtgs PDFДокумент82 страницыFinal Project Neft Rtgs PDFMehul Patel58% (12)

- Banking Sector Performance AnalysisДокумент73 страницыBanking Sector Performance AnalysisNaveen Kumar GuptaОценок пока нет

- ACT15 Intermediate Accounting 1 Pre-Final Quiz ReviewДокумент9 страницACT15 Intermediate Accounting 1 Pre-Final Quiz ReviewJan MarcosОценок пока нет

- Problems Compound InterestДокумент5 страницProblems Compound InterestZariah GtОценок пока нет

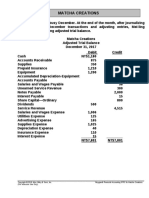

- MC4 Matcha Creations: (For Instructor Use Only)Документ2 страницыMC4 Matcha Creations: (For Instructor Use Only)Reza eka PutraОценок пока нет