Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- MPRA Paper 47159Документ27 страницMPRA Paper 47159Kumar KonarОценок пока нет

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- 4 4 37 438Документ3 страницы4 4 37 438Kumar KonarОценок пока нет

- Smart Classroom Solution BrochureДокумент4 страницыSmart Classroom Solution BrochureKumar KonarОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Cut Off Date10 02 2020Документ1 страницаCut Off Date10 02 2020Kumar KonarОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Amalgamantion and External ReconstructionДокумент67 страницAmalgamantion and External Reconstructionkhuranaamanpreet7gmailcomОценок пока нет

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- L&T Obj New PDFДокумент7 страницL&T Obj New PDFkaran pawarОценок пока нет

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- PattarnДокумент8 страницPattarnKumar KonarОценок пока нет

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- AshichДокумент25 страницAshichPragati BhogleОценок пока нет

- 24-26Документ3 страницы24-26Kumar KonarОценок пока нет

- Consumer Perception Towards Digital Payment ModeДокумент8 страницConsumer Perception Towards Digital Payment ModeSibiCk100% (1)

- 24-26Документ3 страницы24-26Kumar KonarОценок пока нет

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- 2 Comm. MGMT DOC Summer 2020Документ5 страниц2 Comm. MGMT DOC Summer 2020Mansi DhodiОценок пока нет

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- DEE588B1-92F9-4956-B1D9-B31974774A9BДокумент9 страницDEE588B1-92F9-4956-B1D9-B31974774A9BKumar KonarОценок пока нет

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Wcms 396165Документ9 страницWcms 396165Kumar KonarОценок пока нет

- 5 6122856109607747835Документ23 страницы5 6122856109607747835Kumar KonarОценок пока нет

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- 0Документ84 страницы0Kumar KonarОценок пока нет

- 2C003457 PDFДокумент25 страниц2C003457 PDFKumar KonarОценок пока нет

- 2C00345 PDFДокумент1 030 страниц2C00345 PDFPragati BhogleОценок пока нет

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- 2 Comm. MGMT DOC Summer 2020Документ5 страниц2 Comm. MGMT DOC Summer 2020Mansi DhodiОценок пока нет

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- 4 4 37 438Документ3 страницы4 4 37 438Kumar KonarОценок пока нет

- Accountancy Syllabus Maharashtra BoardДокумент8 страницAccountancy Syllabus Maharashtra BoardSangitaОценок пока нет

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Export FinanceДокумент69 страницExport FinanceKumar KonarОценок пока нет

- Boi DataДокумент1 страницаBoi DataKumar KonarОценок пока нет

- QB - Chapter 4 - Amlgamation PDFДокумент24 страницыQB - Chapter 4 - Amlgamation PDFKumar KonarОценок пока нет

- Management of InventoriesДокумент44 страницыManagement of InventoriesKumar KonarОценок пока нет

- 2C00455 PDFДокумент1 854 страницы2C00455 PDFKumar KonarОценок пока нет

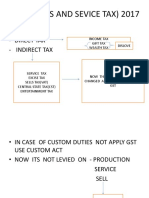

- GST (Goods and Sevice Tax) 2017Документ11 страницGST (Goods and Sevice Tax) 2017Kumar KonarОценок пока нет

- 2C003457 PDFДокумент25 страниц2C003457 PDFKumar KonarОценок пока нет

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Bad Effects of Festivals On The EnvironmentДокумент10 страницBad Effects of Festivals On The EnvironmentSahil Bohra85% (52)

- India As A Dumping GroundДокумент69 страницIndia As A Dumping GroundAmit88% (16)

- (For Office Use Only) : Instruction For Filling This FormДокумент6 страниц(For Office Use Only) : Instruction For Filling This Formspatel1972Оценок пока нет

- Timesheet: January, February, MarchДокумент4 страницыTimesheet: January, February, MarchkhuonggiaОценок пока нет

- 1.0 Executive Summary: TH THДокумент26 страниц1.0 Executive Summary: TH THBabamu Kalmoni JaatoОценок пока нет

- BAT 4M Chapt 1 All SolutionsДокумент78 страницBAT 4M Chapt 1 All Solutionstasfia_khaledОценок пока нет

- Acct Summ Fy11Документ419 страницAcct Summ Fy11Anousack KittilathОценок пока нет

- The Smart Car and Smart Logistics Case TOM FinalДокумент5 страницThe Smart Car and Smart Logistics Case TOM FinalRamarayo MotorОценок пока нет

- It Is Important To Understand The Difference Between Wages and SalariesДокумент41 страницаIt Is Important To Understand The Difference Between Wages and SalariesBaban SandhuОценок пока нет

- What Is Engineering InsuranceДокумент4 страницыWhat Is Engineering InsuranceParth Shastri100% (1)

- Kenneth Arrow EconДокумент4 страницыKenneth Arrow EconRay Patrick BascoОценок пока нет

- Synopsis AdvertisingДокумент10 страницSynopsis AdvertisingbhatiaharryjassiОценок пока нет

- Solution Manual For Mcgraw-Hill Connect Resources For Whittington, Principles of Auditing and Other Assurance Services, 19EДокумент36 страницSolution Manual For Mcgraw-Hill Connect Resources For Whittington, Principles of Auditing and Other Assurance Services, 19Ebenjaminmckinney3l5cv100% (19)

- What Is Process CostingДокумент12 страницWhat Is Process CostingPAUL TIMMYОценок пока нет

- May Blac 2018 QP With AnswersДокумент22 страницыMay Blac 2018 QP With AnswersArchana BagadhiОценок пока нет

- Liberalization Privatization GlobalizationДокумент10 страницLiberalization Privatization GlobalizationShashikant BhandariОценок пока нет

- Differrence Between Primary and Secondary CostДокумент3 страницыDifferrence Between Primary and Secondary CostKauam Santos100% (1)

- E-Logistics and E-Supply Chain Management: Applications For Evolving BusinessДокумент21 страницаE-Logistics and E-Supply Chain Management: Applications For Evolving BusinessRUCHI RATANОценок пока нет

- HMT Watches Revival of A Failed BrandДокумент22 страницыHMT Watches Revival of A Failed BrandDarsh JainОценок пока нет

- Mou System: SPS Solanki AGM (CP)Документ82 страницыMou System: SPS Solanki AGM (CP)SamОценок пока нет

- Lecture 8 PDFДокумент114 страницLecture 8 PDFanonОценок пока нет

- Special Journal 1Документ59 страницSpecial Journal 1Praygod ManaseОценок пока нет

- SAP Archiving StrategyДокумент36 страницSAP Archiving StrategyHariharan ChoodamaniОценок пока нет

- QBCC - Insurance Premium Matrix - Effective 01jul18Документ11 страницQBCC - Insurance Premium Matrix - Effective 01jul18Joel LutgardaОценок пока нет

- Law On Sales Course OutlineДокумент10 страницLaw On Sales Course Outlinekikhay11Оценок пока нет

- Marketing Mix PDFДокумент2 страницыMarketing Mix PDFDulanji Imethya YapaОценок пока нет

- Dove Real Beauty Sketches Case Studies DciNDDNДокумент3 страницыDove Real Beauty Sketches Case Studies DciNDDNRatih HadiantiniОценок пока нет

- Madacasse FallstudieДокумент27 страницMadacasse FallstudiemaxmuellerОценок пока нет

- European Cybersecurity Implementation Overview Res Eng 0814Документ26 страницEuropean Cybersecurity Implementation Overview Res Eng 0814Gabriel ScaunasОценок пока нет

- Smile CardДокумент2 страницыSmile CardSahajPuriОценок пока нет

- Required Exercises Solutions Chapter 13Документ4 страницыRequired Exercises Solutions Chapter 13Le TanОценок пока нет

- Abhishek Kumar: Jindal Poly Films LTDДокумент3 страницыAbhishek Kumar: Jindal Poly Films LTDAarav AroraОценок пока нет

- Sully: The Untold Story Behind the Miracle on the HudsonОт EverandSully: The Untold Story Behind the Miracle on the HudsonРейтинг: 4 из 5 звезд4/5 (103)

- Faster: How a Jewish Driver, an American Heiress, and a Legendary Car Beat Hitler's BestОт EverandFaster: How a Jewish Driver, an American Heiress, and a Legendary Car Beat Hitler's BestРейтинг: 4 из 5 звезд4/5 (28)

- Hero Found: The Greatest POW Escape of the Vietnam WarОт EverandHero Found: The Greatest POW Escape of the Vietnam WarРейтинг: 4 из 5 звезд4/5 (19)

- The End of Craving: Recovering the Lost Wisdom of Eating WellОт EverandThe End of Craving: Recovering the Lost Wisdom of Eating WellРейтинг: 4.5 из 5 звезд4.5/5 (81)

- The Beekeeper's Lament: How One Man and Half a Billion Honey Bees Help Feed AmericaОт EverandThe Beekeeper's Lament: How One Man and Half a Billion Honey Bees Help Feed AmericaОценок пока нет

- ChatGPT Money Machine 2024 - The Ultimate Chatbot Cheat Sheet to Go From Clueless Noob to Prompt Prodigy Fast! Complete AI Beginner’s Course to Catch the GPT Gold Rush Before It Leaves You BehindОт EverandChatGPT Money Machine 2024 - The Ultimate Chatbot Cheat Sheet to Go From Clueless Noob to Prompt Prodigy Fast! Complete AI Beginner’s Course to Catch the GPT Gold Rush Before It Leaves You BehindОценок пока нет

- The Fabric of Civilization: How Textiles Made the WorldОт EverandThe Fabric of Civilization: How Textiles Made the WorldРейтинг: 4.5 из 5 звезд4.5/5 (58)