Вам также может понравиться

- Revenue Accounting and Reporting (RAR) - Concept and ConfigurationДокумент33 страницыRevenue Accounting and Reporting (RAR) - Concept and ConfigurationAnand prakashОценок пока нет

- The Convergence of the GL Account and the Cost Element in Simple FinanceДокумент12 страницThe Convergence of the GL Account and the Cost Element in Simple Financejoseph davidОценок пока нет

- SAP FICO Analyst in Wilmington NC Resume Jonathan WaltersДокумент5 страницSAP FICO Analyst in Wilmington NC Resume Jonathan WaltersJonathanWaltersОценок пока нет

- Event Based Rev Rec in S4 HANA PDFДокумент7 страницEvent Based Rev Rec in S4 HANA PDFambujbajpai1Оценок пока нет

- Magic Quadrant For Utilities Customer Information SystemsДокумент14 страницMagic Quadrant For Utilities Customer Information SystemsMohammed SafwatОценок пока нет

- SAP MM Outline AgreementsДокумент9 страницSAP MM Outline AgreementsrakeshkОценок пока нет

- IFRS Contract Analysis EnablerДокумент7 страницIFRS Contract Analysis EnablerPau Line EscosioОценок пока нет

- Project Systems OverviewДокумент33 страницыProject Systems OverviewPОценок пока нет

- ASUG82379 - City of Mississauga's Journey To Paperless and Automated Accounts Payable Processes Using SAP ConcurДокумент36 страницASUG82379 - City of Mississauga's Journey To Paperless and Automated Accounts Payable Processes Using SAP ConcurAshish MathurОценок пока нет

- Recenue Recognition PDFДокумент33 страницыRecenue Recognition PDFVinay GoyalОценок пока нет

- NSSF ENABLED SAP ERP Implementation Business Blueprint: Project SystemsДокумент20 страницNSSF ENABLED SAP ERP Implementation Business Blueprint: Project SystemsChaitanya KshemkalyaniОценок пока нет

- Sap BudgetДокумент4 страницыSap BudgetRajuSPallapuОценок пока нет

- Revenue Recognition PDFДокумент6 страницRevenue Recognition PDFObilesu RekatlaОценок пока нет

- FICO Interview QuestionsДокумент177 страницFICO Interview QuestionsNagaratna ReddyОценок пока нет

- PS Paragon Process Design Document V 1Документ34 страницыPS Paragon Process Design Document V 1Sameed KhanОценок пока нет

- Revenue Recognition Software FunctionsДокумент4 страницыRevenue Recognition Software FunctionsSuresh NayakОценок пока нет

- Revenue RecognitionДокумент49 страницRevenue RecognitionKevin Smith0% (1)

- Accounts Payable: Global Process Management SystemДокумент89 страницAccounts Payable: Global Process Management SystemcybervistaОценок пока нет

- Sap Data MigrationДокумент4 страницыSap Data MigrationAnasse SabaniОценок пока нет

- PeopleSoft Account Reconciliation Setup and ProcessДокумент21 страницаPeopleSoft Account Reconciliation Setup and ProcessSrinivasu Chowdary BotlaОценок пока нет

- SAP S/4 HANA 2020 FICO For Complete Beginners: Gaurav Learning SolutionsДокумент10 страницSAP S/4 HANA 2020 FICO For Complete Beginners: Gaurav Learning SolutionsJayshree PatilОценок пока нет

- Sanad Wfrice Master List: SR No Object Id Object Object Purpose Tcode Object Sub CategoryДокумент12 страницSanad Wfrice Master List: SR No Object Id Object Object Purpose Tcode Object Sub CategoryAmr IsmailОценок пока нет

- StrtMan The Three TestsДокумент2 страницыStrtMan The Three TestsAnil Kumar SankuruОценок пока нет

- JD Sr. Solution Architect - v1.2Документ4 страницыJD Sr. Solution Architect - v1.2D PAULОценок пока нет

- Agment Fiori Egi3Документ4 страницыAgment Fiori Egi3poonamОценок пока нет

- 00.10 CertifyBest PracticesNamingConventions 12-16Документ8 страниц00.10 CertifyBest PracticesNamingConventions 12-16Bhupathy MОценок пока нет

- C2R TrainingДокумент27 страницC2R TrainingPaul EspinozaОценок пока нет

- Using Benchmarking To Drive EA ProgressДокумент4 страницыUsing Benchmarking To Drive EA ProgressTrivial FaltuОценок пока нет

- Asset Under Construction For Down PaymentsДокумент13 страницAsset Under Construction For Down PaymentsgirijadeviОценок пока нет

- Agile Management in Activate Methodology-020321.1Документ92 страницыAgile Management in Activate Methodology-020321.1erp thungaОценок пока нет

- IFRS Info1Документ6 страницIFRS Info1harikrishnaОценок пока нет

- The New Benchmark For World Class Procure To Pay Process EfficiencyДокумент10 страницThe New Benchmark For World Class Procure To Pay Process EfficiencyZycusIncОценок пока нет

- Overview of Enhancements in SAP Revenue Accounting and Reporting 1.1Документ15 страницOverview of Enhancements in SAP Revenue Accounting and Reporting 1.1April Mosca-ReyesОценок пока нет

- 250open Text VIM For SAP SolutionsДокумент2 страницы250open Text VIM For SAP SolutionsTheo van BrederodeОценок пока нет

- JD Edwards Enterpriseone Buyer Workspace DatasheetДокумент102 страницыJD Edwards Enterpriseone Buyer Workspace DatasheetmuaadhОценок пока нет

- Project Aarohan - Post Go Live Support Document - July 23Документ39 страницProject Aarohan - Post Go Live Support Document - July 23PratikОценок пока нет

- Uninvoiced Receipt Accruals ReportДокумент5 страницUninvoiced Receipt Accruals ReportranvijayОценок пока нет

- Platform Configuration Guide: December 7, 2016 (Ultipro V12.1.2)Документ47 страницPlatform Configuration Guide: December 7, 2016 (Ultipro V12.1.2)MJОценок пока нет

- Budget Management System User ManualДокумент60 страницBudget Management System User ManualChelle P. TenorioОценок пока нет

- ERP Rollout and Merger - Demerger ProcessДокумент15 страницERP Rollout and Merger - Demerger ProcessDanesh ThangarajОценок пока нет

- General: Question NoДокумент8 страницGeneral: Question NoGhosh2Оценок пока нет

- Interest Swap Renewal RFRДокумент47 страницInterest Swap Renewal RFRJames Anderson Luna SilvaОценок пока нет

- Addon Integration ModuleДокумент19 страницAddon Integration ModuleRajib Bose100% (1)

- Asset Accounting (J62) - Process DiagramsДокумент8 страницAsset Accounting (J62) - Process DiagramsMohammed Nawaz ShariffОценок пока нет

- Experienced SAP Convergent Charging Consultant ResumeДокумент1 страницаExperienced SAP Convergent Charging Consultant ResumeHareesh DevireddyОценок пока нет

- Introduction To Tax Assist in VertexДокумент0 страницIntroduction To Tax Assist in Vertexanilr008Оценок пока нет

- SAP Project LifecycleДокумент2 страницыSAP Project LifecyclepoonamОценок пока нет

- BPM Industry Framework 5.0Документ27 страницBPM Industry Framework 5.0DaveОценок пока нет

- Fixed Assets Management PDFДокумент20 страницFixed Assets Management PDFDnukumОценок пока нет

- SAPHANA DocumentationДокумент15 страницSAPHANA DocumentationAnonymous DihBASZОценок пока нет

- Centerpoint Energy'S S/4Hana Central Finance Poc As A First Step To Financial InnovationДокумент26 страницCenterpoint Energy'S S/4Hana Central Finance Poc As A First Step To Financial Innovationmeister_ericОценок пока нет

- System Administrator at Our Organization, Based in HyderabadДокумент3 страницыSystem Administrator at Our Organization, Based in Hyderabadyogesh chowdary100% (1)

- New General Ledger: Important AdvantagesДокумент3 страницыNew General Ledger: Important AdvantagesBiranchi MishraОценок пока нет

- Sap Jva in Ecc 6, If You Implement Sap s/4 Hana For The Faster Results.. Get To Sap s4 HanaДокумент1 страницаSap Jva in Ecc 6, If You Implement Sap s/4 Hana For The Faster Results.. Get To Sap s4 HanakhanmdОценок пока нет

- Differences Between Source to Pay and Procure to PayДокумент6 страницDifferences Between Source to Pay and Procure to PayHima KОценок пока нет

- Real Time Treasury Episode2Документ21 страницаReal Time Treasury Episode2HACОценок пока нет

- Interview Questions - SAP RAR (60 Questions)Документ18 страницInterview Questions - SAP RAR (60 Questions)pammi veeranji ReddyОценок пока нет

- Baan Ivb and Ivc: EDI User GuideДокумент262 страницыBaan Ivb and Ivc: EDI User GuiderprasanthnairОценок пока нет

- PDFДокумент17 страницPDFchristoperedwinОценок пока нет

- MAJ Sep 2012 0752 PDFДокумент20 страницMAJ Sep 2012 0752 PDFchristoperedwinОценок пока нет

- Pb9mat PTM-9 PDFДокумент35 страницPb9mat PTM-9 PDFchristoperedwinОценок пока нет

- Pb7mat PTM-7 PDFДокумент46 страницPb7mat PTM-7 PDFchristoperedwinОценок пока нет

- Chapter 7 Illustrative Solutions PDFДокумент12 страницChapter 7 Illustrative Solutions PDFchristoperedwin50% (2)

- Expenditure CycleДокумент42 страницыExpenditure Cycleerny2412Оценок пока нет

- Audit Fee 3Документ10 страницAudit Fee 3christoperedwinОценок пока нет

- Audit of Cash BalancesДокумент37 страницAudit of Cash BalancesGrace Angelie C. Asio-SalihОценок пока нет

- Auditing Warehouses and Inventories PDFДокумент36 страницAuditing Warehouses and Inventories PDFomarizaidОценок пока нет

- Audit of The Payroll and Personnel Cycle: Auditing 12/eДокумент31 страницаAudit of The Payroll and Personnel Cycle: Auditing 12/eTeddy HaryadiОценок пока нет

- Pb3mat PTM-3 PDFДокумент35 страницPb3mat PTM-3 PDFchristoperedwinОценок пока нет

- Pb4mat PTM-4 PDFДокумент44 страницыPb4mat PTM-4 PDFchristoperedwinОценок пока нет

- Arens12e 15Документ43 страницыArens12e 15Muthia Khairani IIОценок пока нет

- Pb1mat PTM-1 PDFДокумент39 страницPb1mat PTM-1 PDFchristoperedwinОценок пока нет

- Revenue Recognition Accounting TheoryДокумент4 страницыRevenue Recognition Accounting TheorychristoperedwinОценок пока нет

- Managerial Accounting: 8 Edition BY Hansen & MowenДокумент37 страницManagerial Accounting: 8 Edition BY Hansen & MowenFirlanaSubektiОценок пока нет

- Translation of Financial Statements of Foreign AffiliatesДокумент37 страницTranslation of Financial Statements of Foreign AffiliateschristoperedwinОценок пока нет

- PB1MAT Pert.1-4Документ48 страницPB1MAT Pert.1-4christoperedwinОценок пока нет

- PB1MAT Pert.1-4Документ48 страницPB1MAT Pert.1-4christoperedwinОценок пока нет

- Sample MBA Thesis - TWOДокумент72 страницыSample MBA Thesis - TWONury Aponte Aguilar100% (2)

- The Legacy of Pizza Hut Began in 1958Документ10 страницThe Legacy of Pizza Hut Began in 1958psnwktjОценок пока нет

- Marketing Strategies of KFCДокумент27 страницMarketing Strategies of KFCspspsp23Оценок пока нет

- Corporate Level StrategyДокумент16 страницCorporate Level StrategyJeni ZhangОценок пока нет

- FAR Assignment 1Документ3 страницыFAR Assignment 1Abegail Marababol50% (12)

- Aeon SWOT AnalysisДокумент5 страницAeon SWOT AnalysisTip Taptwo50% (2)

- GDIC Performance EvaluationДокумент17 страницGDIC Performance EvaluationZinnia khanОценок пока нет

- Southwest Case StudyДокумент4 страницыSouthwest Case StudyDOUGLASSОценок пока нет

- Saln 2012 Blank FormДокумент3 страницыSaln 2012 Blank FormGel KorlanОценок пока нет

- Intermediate Accounting I IntroductionДокумент6 страницIntermediate Accounting I IntroductionJoovs JoovhoОценок пока нет

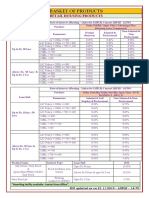

- BASKET OF RETAIL PRODUCTS RATESДокумент3 страницыBASKET OF RETAIL PRODUCTS RATESVirendra K VermaОценок пока нет

- Feedback Form Congress 2014Документ4 страницыFeedback Form Congress 2014Siju BoseОценок пока нет

- Mercedes BenzДокумент16 страницMercedes BenzRahul Bansal100% (1)

- Overview of Family Business Relevant IssuesДокумент175 страницOverview of Family Business Relevant IssuesStudioCentroVeneto s.a.s.Оценок пока нет

- SA220Документ22 страницыSA220Laura D'souza0% (1)

- Philippine Products Company Vs Primateria IncДокумент2 страницыPhilippine Products Company Vs Primateria IncMark Joseph Altura YontingОценок пока нет

- Filipinas Port ServicesДокумент8 страницFilipinas Port ServicesLiezl Oreilly VillanuevaОценок пока нет

- MC Chapter 4Документ2 страницыMC Chapter 4Charmaine Magdangal100% (1)

- Kraft and CadburyДокумент2 страницыKraft and CadburyRezaHakimОценок пока нет

- FM Global - Pipe Friction Loss FactorДокумент64 страницыFM Global - Pipe Friction Loss Factoryunying21100% (1)

- Sapsuccessfactors Coursecontent V5Документ43 страницыSapsuccessfactors Coursecontent V5deepsajjan0% (1)

- Stock MarketДокумент697 страницStock MarketSachin SharmaОценок пока нет

- Deal Report Feb 14 - Apr 14Документ26 страницDeal Report Feb 14 - Apr 14BonviОценок пока нет

- 21032019172516Документ3 страницы21032019172516Azharul IslamОценок пока нет

- Subic Bay Trading Company ProfileДокумент4 страницыSubic Bay Trading Company ProfileNaomi Gimenez BisnarОценок пока нет

- CSR 7-11Документ16 страницCSR 7-11Genepearl Divinagracia100% (1)

- BSN Micro/i Application FormДокумент5 страницBSN Micro/i Application FormVivo Vuvo17% (6)

- GauriДокумент12 страницGauriRahul MittalОценок пока нет

- CIR Vs MarubeniДокумент2 страницыCIR Vs MarubeniJocelyn MagbanuaОценок пока нет

- CASE DIGEST Michael C. Guy vs. Atty. Glenn C. Gacot (Partnership)Документ4 страницыCASE DIGEST Michael C. Guy vs. Atty. Glenn C. Gacot (Partnership)Bo Dist100% (1)