Вам также может понравиться

- Survey of Popularity of Credit Cards Issued by Different BanksДокумент3 страницыSurvey of Popularity of Credit Cards Issued by Different Bankspritam0000100% (2)

- Chase B Statement-MarДокумент4 страницыChase B Statement-MarЮлия ПОценок пока нет

- FAR.3015 Cash and Cash EquivalentsДокумент3 страницыFAR.3015 Cash and Cash EquivalentsJoana Tatac100% (1)

- Key Man InsuranceДокумент15 страницKey Man InsuranceAdarsh Agarwal0% (1)

- Proforma Invoice To Poland PDFДокумент1 страницаProforma Invoice To Poland PDFTommy DwijayaОценок пока нет

- Key BankДокумент4 страницыKey BankKelley33% (3)

- IBC LatestДокумент189 страницIBC LatestType BlankОценок пока нет

- Innovations in Modern Banking and Innova PDFДокумент14 страницInnovations in Modern Banking and Innova PDFСергей ЗайцевОценок пока нет

- Retail and Wholesale Banking in IndiaДокумент12 страницRetail and Wholesale Banking in Indiau2indiaОценок пока нет

- Analysis of NPAДокумент31 страницаAnalysis of NPApremlal1989Оценок пока нет

- Management of Non-Performing Assets - A Brief OverviewДокумент35 страницManagement of Non-Performing Assets - A Brief OverviewDipesh JainОценок пока нет

- Impact of NPA On Dena BankДокумент49 страницImpact of NPA On Dena BankOnkar Ashok KeljiОценок пока нет

- NPA - Banks - FinalДокумент100 страницNPA - Banks - FinalkartikОценок пока нет

- Union Bank Functional Committee AmalgamationДокумент6 страницUnion Bank Functional Committee Amalgamationsom indoraОценок пока нет

- Lessons From NPA Crisis PDFДокумент6 страницLessons From NPA Crisis PDFANKUR PUROHITОценок пока нет

- Introduction To Credit RecoveryДокумент5 страницIntroduction To Credit RecoveryNadeem AnsariОценок пока нет

- NPA Final ReportДокумент60 страницNPA Final ReportVish Amit KandaОценок пока нет

- Study of NPA by Ajinkya (3) FinalДокумент70 страницStudy of NPA by Ajinkya (3) FinalAnjali ShuklaОценок пока нет

- Employer Employee PresentationДокумент30 страницEmployer Employee Presentation2307pradeepОценок пока нет

- Bank of Nova Scotia Brand AnalysisДокумент11 страницBank of Nova Scotia Brand AnalysisAshik Paul0% (1)

- Banking Project NewДокумент77 страницBanking Project NewMohit PaleshaОценок пока нет

- Customer Satisfaction and Retention Crucial for Bank SuccessДокумент74 страницыCustomer Satisfaction and Retention Crucial for Bank SuccessBinaya Kumar MaharanaОценок пока нет

- SWOT Analysis of Jusan BankДокумент8 страницSWOT Analysis of Jusan BankKasper JensenОценок пока нет

- Blackbook Project On Modernization in Banking System in India 163418955 1 PDFДокумент81 страницаBlackbook Project On Modernization in Banking System in India 163418955 1 PDFDr Sachin Chitnis M O UPHC AiroliОценок пока нет

- Defining Provisioning Coverage Ratio-VRK100-05Oct2011Документ2 страницыDefining Provisioning Coverage Ratio-VRK100-05Oct2011RamaKrishna Vadlamudi, CFAОценок пока нет

- IRAC Norms & NPA ManagementДокумент29 страницIRAC Norms & NPA ManagementSarvar PathanОценок пока нет

- Chapter On NPA - 13032020 PDFДокумент105 страницChapter On NPA - 13032020 PDFs s singhОценок пока нет

- NPA Provisioning: Asset Classification Provision Required: Advances Rs. in LacsДокумент3 страницыNPA Provisioning: Asset Classification Provision Required: Advances Rs. in LacsAikya GandhiОценок пока нет

- Bangladesh BankДокумент39 страницBangladesh BankAsadul HoqueОценок пока нет

- Milestones in Indian Banking IndustryДокумент11 страницMilestones in Indian Banking IndustryMONIKA RUBINОценок пока нет

- Nabil Bank Deposit MobilizationДокумент32 страницыNabil Bank Deposit MobilizationSurya SatoreОценок пока нет

- Internship Report on Integrated Security Services LimitedДокумент15 страницInternship Report on Integrated Security Services LimitedsufiОценок пока нет

- Determinants of Non-Performing LoansДокумент34 страницыDeterminants of Non-Performing LoansSelim KhanОценок пока нет

- Case Study NPAДокумент3 страницыCase Study NPAGulshan KumarОценок пока нет

- Reliance Retail LimitedДокумент4 страницыReliance Retail LimitedmoulithyaОценок пока нет

- Factoring Vs ForfeitingДокумент27 страницFactoring Vs ForfeitingShruti AshokОценок пока нет

- BFN 407 - DocxДокумент187 страницBFN 407 - DocxTimi Marquis100% (1)

- Credit ManagementДокумент4 страницыCredit ManagementYuuna HoshinoОценок пока нет

- A Study ON Liquidity Analysis of Nic Asia Bank Limited: A Project Work ReportДокумент41 страницаA Study ON Liquidity Analysis of Nic Asia Bank Limited: A Project Work ReportPradip Kumar ShahОценок пока нет

- Introduction to NPAs in BankingДокумент46 страницIntroduction to NPAs in BankingPiyushVarmaОценок пока нет

- Dhaval File 123Документ72 страницыDhaval File 123Rahul NishadОценок пока нет

- NBFCs Explained: What is an NBFC and Key Differences from BanksДокумент49 страницNBFCs Explained: What is an NBFC and Key Differences from BanksMalavika MadhuОценок пока нет

- Master Cir Lead Bank SchemeДокумент79 страницMaster Cir Lead Bank Schemekgaurav001Оценок пока нет

- Financial Performance of Private Sector Banks in India - An EvaluationДокумент14 страницFinancial Performance of Private Sector Banks in India - An Evaluationswapna29Оценок пока нет

- Credit Recovery CharacteristicsДокумент2 страницыCredit Recovery CharacteristicsNCVPSОценок пока нет

- BCOM 1ST YR Commercial Bank - Unit IДокумент12 страницBCOM 1ST YR Commercial Bank - Unit IUrvi KaleОценок пока нет

- Avinash ProjectДокумент58 страницAvinash ProjectSonali Pawar100% (1)

- Research MethodologyДокумент6 страницResearch Methodologyshrikrushna javanjal100% (1)

- IT in Banking SectorДокумент21 страницаIT in Banking SectorShivesh AggarwalОценок пока нет

- Subject: Financial Management: Yes Bank CrisisДокумент9 страницSubject: Financial Management: Yes Bank Crisisaryan sharmaОценок пока нет

- Unit 2, Business CommunicationДокумент33 страницыUnit 2, Business Communicationcoder ninjaОценок пока нет

- Bank ManagementДокумент36 страницBank ManagementMohammed ShaffanОценок пока нет

- What Is A Bank AccountДокумент6 страницWhat Is A Bank AccountJan Sheer ShahОценок пока нет

- A Comparative Study of Growth Analysis oДокумент3 страницыA Comparative Study of Growth Analysis oKirti GorivaleОценок пока нет

- Complete ProjectДокумент72 страницыComplete ProjectKevin JacobОценок пока нет

- (Amit Kumar) Foreign Banks in IndiaДокумент27 страниц(Amit Kumar) Foreign Banks in IndiaPrachi PandeyОценок пока нет

- Project Report Union BankДокумент201 страницаProject Report Union BankVikas SinghОценок пока нет

- 5 Major Sources of Rural Credit in IndiaДокумент5 страниц5 Major Sources of Rural Credit in IndiaParimita Sarma0% (1)

- "Study On Loan and Credit Facility at SDCC Bank, Rourkela ": Summer Internship Project Report OnДокумент81 страница"Study On Loan and Credit Facility at SDCC Bank, Rourkela ": Summer Internship Project Report OnASIT EKKAОценок пока нет

- Project On UCO Bank FinalДокумент43 страницыProject On UCO Bank Finalvnktsh50% (2)

- Introduction to Research on Non-Performing Assets in Indian BankingДокумент12 страницIntroduction to Research on Non-Performing Assets in Indian BankingkkvОценок пока нет

- Krishna GosaviДокумент16 страницKrishna Gosavikrishna gosaviОценок пока нет

- Impact of Npa On Profitability:Empirical Study of Private Sector Banks in IndiaДокумент63 страницыImpact of Npa On Profitability:Empirical Study of Private Sector Banks in IndiaTarun MirgОценок пока нет

- Krishna Gosavi 1 NPAДокумент34 страницыKrishna Gosavi 1 NPAJayesh ChaudhariОценок пока нет

- Uti BankДокумент86 страницUti BankMohit kolliОценок пока нет

- Summary of Telangana Movement - MagazineДокумент22 страницыSummary of Telangana Movement - MagazineSrinivas NawabОценок пока нет

- CurrentAffairs MagazineДокумент16 страницCurrentAffairs MagazineSrinivas NawabОценок пока нет

- Science Capsule 2015 PDFДокумент19 страницScience Capsule 2015 PDFEr Puneet GoyalОценок пока нет

- Dyuthi T1824Документ338 страницDyuthi T1824Ahmed AlyaniОценок пока нет

- MRV - CRM - Gas Turbine Based CoGeneration - MRV - CRM - GTG - 09Документ64 страницыMRV - CRM - Gas Turbine Based CoGeneration - MRV - CRM - GTG - 09Akshit RaychaОценок пока нет

- AbstractДокумент1 страницаAbstractSrinivas NawabОценок пока нет

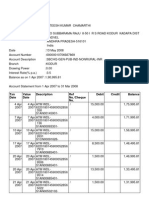

- TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент10 страницTXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancesatishapexОценок пока нет

- PDFДокумент4 страницыPDFAmit vohraОценок пока нет

- Syed Sajjad HaiderДокумент3 страницыSyed Sajjad HaiderMuntaha SyedОценок пока нет

- Indian Money MarketДокумент2 страницыIndian Money MarketSandeep KulkarniОценок пока нет

- ChallanДокумент1 страницаChallanMuhammad AhmadОценок пока нет

- Comercial Bank: Functions of Comercial Banks Primary Functions 1. Accept DepositsДокумент3 страницыComercial Bank: Functions of Comercial Banks Primary Functions 1. Accept DepositstashfeenОценок пока нет

- Research Project On ATM SystemДокумент8 страницResearch Project On ATM Systemgenuinespot100% (1)

- Libor Transition A Practical Guide PDFДокумент31 страницаLibor Transition A Practical Guide PDFmartaОценок пока нет

- Solutions To Questions - Chapter 20 The Secondary Mortgage Market: Cmos and Derivative Securities Question 20-1Документ17 страницSolutions To Questions - Chapter 20 The Secondary Mortgage Market: Cmos and Derivative Securities Question 20-1--bolabolaОценок пока нет

- MODT Format - Borrower (Final) - Home Loan, BT, LAPДокумент4 страницыMODT Format - Borrower (Final) - Home Loan, BT, LAPXerox PointОценок пока нет

- Candidate's Copy IDBI Bank Cash PayДокумент1 страницаCandidate's Copy IDBI Bank Cash Payapurv429Оценок пока нет

- TVM Complete TemplateДокумент17 страницTVM Complete TemplateAlok RajОценок пока нет

- Ewu Mba Fall 2021 Final ExamДокумент2 страницыEwu Mba Fall 2021 Final ExamChowdhury Mobarrat Haider AdnanОценок пока нет

- Summer Placement Presentation InsightsДокумент23 страницыSummer Placement Presentation Insightsmannycase13Оценок пока нет

- Fpayh Fpayhx FpaypДокумент448 страницFpayh Fpayhx FpaypSundarKrishnaОценок пока нет

- Acquisition of Merrill Lynch by Bank of AmericaДокумент26 страницAcquisition of Merrill Lynch by Bank of AmericaNancy AggarwalОценок пока нет

- Assignment # 2: Course Title: Introduction To Mathematics Question No 01Документ2 страницыAssignment # 2: Course Title: Introduction To Mathematics Question No 01Quratulain Shafique QureshiОценок пока нет

- Split Payment Cervantes, Edlene B. 01-04-11Документ1 страницаSplit Payment Cervantes, Edlene B. 01-04-11Ervin Joseph Bato CervantesОценок пока нет

- Accenture Ripple Reisebank Video TranscriptДокумент2 страницыAccenture Ripple Reisebank Video TranscriptJeffrey BahnsenОценок пока нет

- The Supplemental Prospectus of An Actual Offering by Royal BankДокумент2 страницыThe Supplemental Prospectus of An Actual Offering by Royal BankAmit PandeyОценок пока нет

- ECCCRIS Registration and Credit ReportДокумент1 страницаECCCRIS Registration and Credit ReportMohamad HilmiОценок пока нет

- BPRD Circular No. 15 June 21, 1998: All Banks, Dear SirsДокумент40 страницBPRD Circular No. 15 June 21, 1998: All Banks, Dear SirsKyo 666Оценок пока нет

- LK UNIT 3 Memproses Transaksi KeuanganДокумент3 страницыLK UNIT 3 Memproses Transaksi KeuanganYudya Dhanny Syah Permana Arvai100% (1)

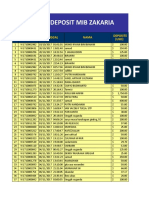

- DEPOSIT LISTДокумент284 страницыDEPOSIT LISTIbrahim100% (1)

- Payment Information Account Summary: July 9, 2020Документ3 страницыPayment Information Account Summary: July 9, 2020Mark Williams0% (1)