Вам также может понравиться

- Health Care Financing - 8Документ13 страницHealth Care Financing - 8copy smart50% (2)

- Health Financing: Dr. Jamelah R. Usman-PasagiДокумент27 страницHealth Financing: Dr. Jamelah R. Usman-PasagiGada AbdulcaderОценок пока нет

- Health Financing Module PDFДокумент34 страницыHealth Financing Module PDFRaihansyah HasibuanОценок пока нет

- Health Financing FunctionsДокумент4 страницыHealth Financing FunctionsFredy GunawanОценок пока нет

- Health Economics - Lecture Ch01Документ16 страницHealth Economics - Lecture Ch01Katherine SauerОценок пока нет

- Health Economics - Lecture Ch12Документ61 страницаHealth Economics - Lecture Ch12Katherine SauerОценок пока нет

- Health Sector in Pakistan by Aamir Mughal and Pakistan Medical AssociationДокумент81 страницаHealth Sector in Pakistan by Aamir Mughal and Pakistan Medical AssociationAamir Mughal100% (1)

- 1.introduction To Health Education & Promotion (1) .Документ44 страницы1.introduction To Health Education & Promotion (1) .Nebiyu NegaОценок пока нет

- Health Economics - Lecture Ch13Документ39 страницHealth Economics - Lecture Ch13Katherine SauerОценок пока нет

- Equity in HealthcareДокумент17 страницEquity in HealthcareApsopela SandiveraОценок пока нет

- 8 Risk Management in Contemporary Pharmacy PracticeДокумент36 страниц8 Risk Management in Contemporary Pharmacy PracticeLollyОценок пока нет

- Health Policy: Assistant Professor Punjab University College of PharmacyДокумент21 страницаHealth Policy: Assistant Professor Punjab University College of PharmacyUsama AmjadОценок пока нет

- POSHAN Abhiyaan PDFДокумент2 страницыPOSHAN Abhiyaan PDFVishal Pal Vishal PalОценок пока нет

- Overview of Healthcare System in Ghana 2Документ19 страницOverview of Healthcare System in Ghana 2Batsa AndrewsОценок пока нет

- Health Administration NewДокумент10 страницHealth Administration NewjessyОценок пока нет

- Health Care Service and Its RelationДокумент10 страницHealth Care Service and Its RelationRomeo Rivera0% (1)

- Healthcare in IndiaДокумент40 страницHealthcare in Indiamanisha paikaray100% (1)

- Health Financing Overview-1Документ15 страницHealth Financing Overview-1Lydia ladislausОценок пока нет

- Bangladesh National Health Policy-2011Документ19 страницBangladesh National Health Policy-2011Fairouz Khan100% (1)

- Health Sector Reform PDFДокумент54 страницыHealth Sector Reform PDFCherry Mae L. VillanuevaОценок пока нет

- Health Systems Strengthening - The University of MelbourneДокумент14 страницHealth Systems Strengthening - The University of MelbourneEstefanía MariñoОценок пока нет

- A Study To Assess The Quality of Life of Patients With Osteoarthritis in A Selected Hospital, Coimbatore, With A View To Develop An Informational BookletДокумент5 страницA Study To Assess The Quality of Life of Patients With Osteoarthritis in A Selected Hospital, Coimbatore, With A View To Develop An Informational BookletInternational Journal of Innovative Science and Research TechnologyОценок пока нет

- Models of Health PromotionДокумент6 страницModels of Health PromotionReyta NoorОценок пока нет

- Implementation of Labor Laws and PoliciesДокумент46 страницImplementation of Labor Laws and PoliciesAwantika Jain100% (1)

- health care system of swedenبДокумент34 страницыhealth care system of swedenبAhmedAljebouli0% (1)

- IFM PortfolioДокумент20 страницIFM PortfolioPARTH KHANNAОценок пока нет

- Medico-Legal Cases in IndiaДокумент2 страницыMedico-Legal Cases in Indiaaishwarya shetty100% (1)

- Health Systems 2009 20aug AДокумент74 страницыHealth Systems 2009 20aug ANational Child Health Resource Centre (NCHRC)Оценок пока нет

- Determinants of HealthДокумент30 страницDeterminants of HealthRuchi YadavОценок пока нет

- SHA301 Health Economics and Health FinancingДокумент3 страницыSHA301 Health Economics and Health FinancingThomas MaseseОценок пока нет

- Health Financing ModelsДокумент7 страницHealth Financing ModelsPrashant Nathani100% (1)

- Health ModelДокумент41 страницаHealth ModelMayom Mabuong100% (3)

- Ayushman Bharat YojanaДокумент28 страницAyushman Bharat YojanaParth VasaveОценок пока нет

- My PresentationДокумент14 страницMy PresentationnamithaОценок пока нет

- 1.2 Health Care Delivery SystemДокумент53 страницы1.2 Health Care Delivery Systemsefal mansuri100% (1)

- Ethiopia's Community-Based Health Insurance: A Step On The Road To Universal Health CoverageДокумент12 страницEthiopia's Community-Based Health Insurance: A Step On The Road To Universal Health CoverageTsegayeОценок пока нет

- CMN 463 Lecture 2 Insurance Medicare and MedicaidДокумент18 страницCMN 463 Lecture 2 Insurance Medicare and MedicaidCarlos GuiterizОценок пока нет

- Financialmanagementpresentation 170131104519 PDFДокумент29 страницFinancialmanagementpresentation 170131104519 PDFwarda santiagoОценок пока нет

- Directing & CoordinationДокумент15 страницDirecting & CoordinationAnkesh Shrivastava100% (1)

- Comparison Between Life Insurance and General InsuranceДокумент22 страницыComparison Between Life Insurance and General InsuranceBALLB BATCH-1Оценок пока нет

- 3.1 Concept of Health EconomicsДокумент4 страницы3.1 Concept of Health EconomicsmitalptОценок пока нет

- Economics of Health CareДокумент17 страницEconomics of Health CareJason Young0% (1)

- ESICДокумент34 страницыESICAanchal Mehta100% (1)

- IntroductionДокумент7 страницIntroductionMadhu Bishnoi100% (1)

- Health PolicyДокумент19 страницHealth PolicyBismah Saeed100% (1)

- Ghana's Health Care SystemДокумент14 страницGhana's Health Care SystemTheophilus BaidooОценок пока нет

- Introduction To Administrative TheoryДокумент10 страницIntroduction To Administrative Theorymuna moono100% (1)

- Health Reforms in IndiaДокумент37 страницHealth Reforms in Indiavarshasharma05Оценок пока нет

- Health Economics: Ms. Ancy Chacko Iind Year M.SC Nursing Govt. College of Nursing AlappuzhaДокумент101 страницаHealth Economics: Ms. Ancy Chacko Iind Year M.SC Nursing Govt. College of Nursing Alappuzhajyoti kunduОценок пока нет

- Healthcare Financing in IndiAДокумент86 страницHealthcare Financing in IndiAGeet Sheil67% (3)

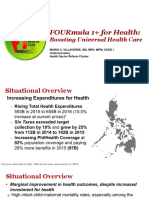

- 4 FOURmula 1 For Health Boosting Universal Health Care by DR Beverly HoДокумент12 страниц4 FOURmula 1 For Health Boosting Universal Health Care by DR Beverly HoJanella DandanОценок пока нет

- Thailand'S Universal Health Coverage: Dr. Thaworn Sakunphanit MD., FRCPT, Ba (Econ), Msc. (Social Policy Financing)Документ17 страницThailand'S Universal Health Coverage: Dr. Thaworn Sakunphanit MD., FRCPT, Ba (Econ), Msc. (Social Policy Financing)IManОценок пока нет

- Employees State Insurance SchemeДокумент8 страницEmployees State Insurance SchemeKrishnaveni MurugeshОценок пока нет

- Budget, Budgetting Process, Classification of Budget, Budget in Health Care SystemsДокумент9 страницBudget, Budgetting Process, Classification of Budget, Budget in Health Care SystemsSimran JosanОценок пока нет

- PHC Concept & PrinciplesДокумент68 страницPHC Concept & PrinciplesDayò BáyòОценок пока нет

- Litrature Review of Rural Healthcare Management in IndiaДокумент42 страницыLitrature Review of Rural Healthcare Management in Indiasri_cbm67% (6)

- Central-Pollution-Control-Board-UPSC NotesДокумент3 страницыCentral-Pollution-Control-Board-UPSC Notesmrigank shekharОценок пока нет

- Health ExpenditureДокумент28 страницHealth ExpenditureToche Doce100% (2)

- Ayushman Bharat Detailed ExplanationДокумент3 страницыAyushman Bharat Detailed ExplanationnirmalОценок пока нет

- NATIONAL HEALTH POLICY GHДокумент12 страницNATIONAL HEALTH POLICY GHAbigail Awortwe AndohОценок пока нет

- Chapter 2 Maternal AnatomyДокумент9 страницChapter 2 Maternal AnatomyRem Alfelor100% (2)

- Chap 8 Prenatal CareДокумент9 страницChap 8 Prenatal CareRem AlfelorОценок пока нет

- OB Williams Chap 2 Maternal PhysiologyДокумент9 страницOB Williams Chap 2 Maternal PhysiologyRem Alfelor100% (2)

- OB Williams Chap 2 Maternal AnatomyДокумент7 страницOB Williams Chap 2 Maternal AnatomyRem Alfelor0% (1)

- Chapter 4 Maternal PhysiologyДокумент12 страницChapter 4 Maternal PhysiologyRem AlfelorОценок пока нет

- POST-TEST Mock Written Diplomate ExaminationДокумент62 страницыPOST-TEST Mock Written Diplomate ExaminationRem AlfelorОценок пока нет

- Gyne 3rd LEДокумент4 страницыGyne 3rd LERem AlfelorОценок пока нет

- Gyne 5 Long ExamДокумент3 страницыGyne 5 Long ExamRem Alfelor100% (1)

- Chapter 3 Congenital Genitourinary AbnormalitiesДокумент4 страницыChapter 3 Congenital Genitourinary AbnormalitiesRem AlfelorОценок пока нет

- Gyne 1st Long Exam 2009 ANSДокумент3 страницыGyne 1st Long Exam 2009 ANSRem AlfelorОценок пока нет

- Gyne Prelims 2009Документ10 страницGyne Prelims 2009Rem AlfelorОценок пока нет

- HP CardДокумент3 страницыHP CardRem AlfelorОценок пока нет

- Gyne 6th Long Exam ANSДокумент4 страницыGyne 6th Long Exam ANSRem AlfelorОценок пока нет

- Surgery 6th TCVSДокумент3 страницыSurgery 6th TCVSRem AlfelorОценок пока нет

- Pedia MidtermДокумент6 страницPedia MidtermRem AlfelorОценок пока нет

- Case 04 - Prenatal CareДокумент3 страницыCase 04 - Prenatal CareRem AlfelorОценок пока нет

- Reviewer - LE4Документ3 страницыReviewer - LE4Rem AlfelorОценок пока нет

- PEDIA Nephroquiz2015Документ4 страницыPEDIA Nephroquiz2015Rem AlfelorОценок пока нет

- Retinoblastoma QuizДокумент1 страницаRetinoblastoma QuizRem AlfelorОценок пока нет

- Im Nephro ExamДокумент4 страницыIm Nephro ExamRem AlfelorОценок пока нет

- Williams 24th Ed Chap 40 HypertensionДокумент12 страницWilliams 24th Ed Chap 40 HypertensionRem AlfelorОценок пока нет

- Psychiatric History and Mental Status ExaminationДокумент6 страницPsychiatric History and Mental Status ExaminationRem AlfelorОценок пока нет

- Alcohol Induced SchizophreniaДокумент3 страницыAlcohol Induced SchizophreniaRem AlfelorОценок пока нет

- Case 01 - Maternal PhysiologyДокумент5 страницCase 01 - Maternal PhysiologyRem AlfelorОценок пока нет

- Pedia QuizthyroidДокумент2 страницыPedia QuizthyroidRem AlfelorОценок пока нет

- Floors Census PDFДокумент2 страницыFloors Census PDFRem AlfelorОценок пока нет

- Pcap 2012Документ1 страницаPcap 2012Rem AlfelorОценок пока нет

- Community Medicine Cavite ReportДокумент46 страницCommunity Medicine Cavite ReportRem AlfelorОценок пока нет

- Rhabdomyosarcoma Pedia Case ReportДокумент36 страницRhabdomyosarcoma Pedia Case ReportRem AlfelorОценок пока нет

- Clinicopathological Conference 2Документ23 страницыClinicopathological Conference 2Rem AlfelorОценок пока нет

- Mudbound: Virgil Williams and Dee ReesДокумент125 страницMudbound: Virgil Williams and Dee Reesmohan kumarОценок пока нет

- Lozada Vs MendozaДокумент4 страницыLozada Vs MendozaHarold EstacioОценок пока нет

- In Practice Blood Transfusion in Dogs and Cats1Документ7 страницIn Practice Blood Transfusion in Dogs and Cats1何元Оценок пока нет

- Write A Program in C To Check Whether A Entered Number Is Positive, Negative or ZeroДокумент10 страницWrite A Program in C To Check Whether A Entered Number Is Positive, Negative or ZeroSabin kandelОценок пока нет

- Assignment 1: Microeconomics - Group 10Документ13 страницAssignment 1: Microeconomics - Group 10Hải LêОценок пока нет

- D3Документ2 страницыD3zyaОценок пока нет

- Apartheid in South AfricaДокумент24 страницыApartheid in South Africaapi-300093410100% (1)

- The Behaviour and Ecology of The Zebrafish, Danio RerioДокумент22 страницыThe Behaviour and Ecology of The Zebrafish, Danio RerioNayara Santina VieiraОценок пока нет

- Molecular Biology - WikipediaДокумент9 страницMolecular Biology - WikipediaLizbethОценок пока нет

- Assertiveness FinlandДокумент2 страницыAssertiveness FinlandDivyanshi ThakurОценок пока нет

- FAR REview. DinkieДокумент10 страницFAR REview. DinkieJollibee JollibeeeОценок пока нет

- Draft DAO SAPA Provisional AgreementДокумент6 страницDraft DAO SAPA Provisional AgreementStaff of Gov Victor J YuОценок пока нет

- Official Memo: From: To: CCДокумент4 страницыOfficial Memo: From: To: CCrobiОценок пока нет

- WWW - Nswkendo IaidoДокумент1 страницаWWW - Nswkendo IaidoAshley AndersonОценок пока нет

- Nielsen Esports Playbook For Brands 2019Документ28 страницNielsen Esports Playbook For Brands 2019Jean-Louis ManzonОценок пока нет

- Exeter: Durance-Class Tramp Freighter Medium Transport Average, Turn 2 Signal Basic Pulse BlueДокумент3 страницыExeter: Durance-Class Tramp Freighter Medium Transport Average, Turn 2 Signal Basic Pulse BlueMike MitchellОценок пока нет

- Periodic Table & PeriodicityДокумент22 страницыPeriodic Table & PeriodicityMike hunkОценок пока нет

- Al-Baraa Ibn Malik Al-AnsariДокумент3 страницыAl-Baraa Ibn Malik Al-AnsariRahbarTvОценок пока нет

- Promises From The BibleДокумент16 страницPromises From The BiblePaul Barksdale100% (1)

- KCET MOCK TEST PHY Mock 2Документ8 страницKCET MOCK TEST PHY Mock 2VikashОценок пока нет

- Disciplinary Literacy Strategies To Support Transactions in Elementary Social StudiesДокумент11 страницDisciplinary Literacy Strategies To Support Transactions in Elementary Social Studiesmissjoseph0803Оценок пока нет

- BIM 360-Training Manual - MEP ConsultantДокумент23 страницыBIM 360-Training Manual - MEP ConsultantAakaara 3DОценок пока нет

- Historical Background of Land Ownership in The PhilippinesДокумент2 страницыHistorical Background of Land Ownership in The Philippinesjohn100% (1)

- CHP 11: Setting Goals and Managing The Sales Force's PerformanceДокумент2 страницыCHP 11: Setting Goals and Managing The Sales Force's PerformanceHEM BANSALОценок пока нет

- Crochet World October 2011Документ68 страницCrochet World October 2011Lydia Lakatos100% (15)

- Khenpo Tsultrim Gyamtso Rinpoche - Meditation On EmptinessДокумент206 страницKhenpo Tsultrim Gyamtso Rinpoche - Meditation On Emptinessdorje@blueyonder.co.uk100% (1)

- WILDLIFEДокумент35 страницWILDLIFEnayab gulОценок пока нет

- A Win-Win Water Management Approach in The PhilippinesДокумент29 страницA Win-Win Water Management Approach in The PhilippinesgbalizaОценок пока нет

- John Wick 4 HD Free r6hjДокумент16 страницJohn Wick 4 HD Free r6hjafdal mahendraОценок пока нет

- Pr1 m4 Identifying The Inquiry and Stating The ProblemДокумент61 страницаPr1 m4 Identifying The Inquiry and Stating The ProblemaachecheutautautaОценок пока нет