Вам также может понравиться

- 7 Finalnew Sugg June09Документ17 страниц7 Finalnew Sugg June09mknatoo1963Оценок пока нет

- Accounting-Financial Statements of Companies-1653399167327513Документ37 страницAccounting-Financial Statements of Companies-1653399167327513Badhrinath ShanmugamОценок пока нет

- (L) Chapter 13 Accounts For Limited CompanyДокумент13 страниц(L) Chapter 13 Accounts For Limited CompanyCHZE CHZI CHUAHОценок пока нет

- PGBP-2Документ10 страницPGBP-2Srinivas T. RajuОценок пока нет

- TAXATION: Improperly Accumulated Earnings Tax (IAET) 2020 Improperly Accumulated Earnings Tax (IAET)Документ7 страницTAXATION: Improperly Accumulated Earnings Tax (IAET) 2020 Improperly Accumulated Earnings Tax (IAET)YashОценок пока нет

- Vadilal Industries LimitedДокумент29 страницVadilal Industries LimitedSubhash YadavОценок пока нет

- Chapter 8: Leverage and CVP Analysis: 2001 Dec 2bДокумент4 страницыChapter 8: Leverage and CVP Analysis: 2001 Dec 2bShubham ParabОценок пока нет

- Financial Management 1Документ36 страницFinancial Management 1nirmljnОценок пока нет

- Management Control SystemДокумент11 страницManagement Control SystemomkarsawantОценок пока нет

- Valuation FundamentalДокумент4 страницыValuation FundamentalpranavОценок пока нет

- F6PKN 2012 Dec A PDFДокумент13 страницF6PKN 2012 Dec A PDFabby bendarasОценок пока нет

- Financial Statements, Cash Flow and TaxesДокумент44 страницыFinancial Statements, Cash Flow and TaxesAli JumaniОценок пока нет

- Question Bank: Errorless Taxation by Ca Pranav Chandak at Pranav Chandak Academy, PuneДокумент8 страницQuestion Bank: Errorless Taxation by Ca Pranav Chandak at Pranav Chandak Academy, PuneSimran MeherОценок пока нет

- BBPW3103 - Topic02 - EnglishДокумент67 страницBBPW3103 - Topic02 - EnglishclairynaОценок пока нет

- Prepration of Financial StatementsДокумент35 страницPrepration of Financial StatementsMercy GamingОценок пока нет

- Accounting For Intra Group TransactionsДокумент44 страницыAccounting For Intra Group Transactionsanalystbank100% (5)

- Mock E Exam Pap ERДокумент19 страницMock E Exam Pap ERtim_rattanaОценок пока нет

- © The Institute of Chartered Accountants of IndiaДокумент56 страниц© The Institute of Chartered Accountants of IndiaTejaОценок пока нет

- Financial Statements, Cash Flow, and TaxesДокумент44 страницыFinancial Statements, Cash Flow, and TaxesreОценок пока нет

- FM&EconomicsQUESTIONPAPER MAY21Документ6 страницFM&EconomicsQUESTIONPAPER MAY21Harish Palani PalaniОценок пока нет

- Directors' Report: Larsen & Toubro Infotech LimitedДокумент33 страницыDirectors' Report: Larsen & Toubro Infotech LimitedNirmal Rintu RaviОценок пока нет

- Paye 2023Документ22 страницыPaye 2023v8ysqzd9pbОценок пока нет

- Ind As 34Документ3 страницыInd As 34qwertyОценок пока нет

- Annual Report 18-19Документ338 страницAnnual Report 18-19sairaj bhatkarОценок пока нет

- Contents of An Interim Financial Report: Unit OverviewДокумент5 страницContents of An Interim Financial Report: Unit OverviewRITZ BROWNОценок пока нет

- The Profit and Loss Appropriation AccountДокумент4 страницыThe Profit and Loss Appropriation AccountSarthak GuptaОценок пока нет

- UBS Capital BudgetingДокумент19 страницUBS Capital BudgetingRajas MahajanОценок пока нет

- 6 201506Q3Документ19 страниц6 201506Q3Hannah GohОценок пока нет

- Deffered Tax - QuestionДокумент8 страницDeffered Tax - Questionanuragsamanta1208Оценок пока нет

- NSE Financial Modeling Exam Questions and Solution - 2Документ55 страницNSE Financial Modeling Exam Questions and Solution - 2rahulnationalite83% (6)

- Module 6 - Income Tax On Corporations - Part 2Документ5 страницModule 6 - Income Tax On Corporations - Part 2Never Letting GoОценок пока нет

- Problems On Leverage AnalysisДокумент4 страницыProblems On Leverage AnalysisMandar SangleОценок пока нет

- 02 Financing Decisions - Leverages - Practice SheetДокумент22 страницы02 Financing Decisions - Leverages - Practice SheetPatrick LoboОценок пока нет

- Dividend and Managerial Remuneration Adjustments-1Документ3 страницыDividend and Managerial Remuneration Adjustments-1Shwetta GogawaleОценок пока нет

- 01 LeveragesДокумент11 страниц01 LeveragesZerefОценок пока нет

- 10-Practical Questions of Individuals (78-113)Документ38 страниц10-Practical Questions of Individuals (78-113)Sajid Saith0% (1)

- Ajooni BiotechДокумент21 страницаAjooni BiotechSunny RaoОценок пока нет

- AssignmentДокумент3 страницыAssignmentChourasia HarishОценок пока нет

- Unconsolidated Condensed Interim Financial Statements of Allied Bank LimitedДокумент44 страницыUnconsolidated Condensed Interim Financial Statements of Allied Bank LimitedenkashmiriОценок пока нет

- Exercise Questions On NT and MCITДокумент2 страницыExercise Questions On NT and MCITDamdam AlunanОценок пока нет

- Unit - II - Analysis of Financial StatementsДокумент54 страницыUnit - II - Analysis of Financial StatementsPRERNA PANDEY100% (1)

- Unit - II - Analysis of Financial StatementsДокумент54 страницыUnit - II - Analysis of Financial StatementsPRERNA PANDEYОценок пока нет

- Tax Filling For Unit Trust DividendsДокумент4 страницыTax Filling For Unit Trust DividendsYew Toh TatОценок пока нет

- TAX-701U (Income Tax - Corporations) With UpdatesДокумент11 страницTAX-701U (Income Tax - Corporations) With UpdatesBernadette Panican100% (3)

- Financial Accounting & Analysis Sep 2020Документ15 страницFinancial Accounting & Analysis Sep 2020AkshatОценок пока нет

- AAB CN - Interim Report (2010 - Q1) - FinancialsДокумент19 страницAAB CN - Interim Report (2010 - Q1) - Financialselombardi1Оценок пока нет

- Financial Results & Limited Review Report For Dec 31, 2015 (Result)Документ4 страницыFinancial Results & Limited Review Report For Dec 31, 2015 (Result)Shyam SunderОценок пока нет

- Question paper-TYBMS-SSF-Oct10Документ2 страницыQuestion paper-TYBMS-SSF-Oct10Sneha Parab100% (1)

- F5 Division Roi RiДокумент16 страницF5 Division Roi RiMazni Hanisah100% (1)

- Financial PlanДокумент7 страницFinancial PlanGeryca CarranzaОценок пока нет

- FCES - Damanhour 3 Year - 2 Term: Management AccountingДокумент11 страницFCES - Damanhour 3 Year - 2 Term: Management Accountingahmedgalalali497Оценок пока нет

- Accounting GR 12 Exemplar Ans Book 2008 EnglishДокумент20 страницAccounting GR 12 Exemplar Ans Book 2008 EnglishAudrey RobinsonОценок пока нет

- Leverages: Raksha Khetan-23 Saumitra Kumar-26 Saqib Azam Qadri-42Документ21 страницаLeverages: Raksha Khetan-23 Saumitra Kumar-26 Saqib Azam Qadri-42sampdalvi07Оценок пока нет

- Acct1511 Final VersionДокумент33 страницыAcct1511 Final VersioncarolinetsangОценок пока нет

- Accgr12ssipsessions12 15tn2013book31Документ55 страницAccgr12ssipsessions12 15tn2013book31siyabongaОценок пока нет

- Ebit-Eps Analysis: Operating EarningsДокумент27 страницEbit-Eps Analysis: Operating EarningsKaran MorbiaОценок пока нет

- Tax XXXXДокумент60 страницTax XXXXGerald Bowe ResuelloОценок пока нет

- Dabur (Uk) Limited: Annual Report For The Financial Year Ended 31St March, 2009Документ13 страницDabur (Uk) Limited: Annual Report For The Financial Year Ended 31St March, 2009rishabhrockОценок пока нет

- Ashish Sadh 46Документ5 страницAshish Sadh 46shashankОценок пока нет

- 7 DesignДокумент9 страниц7 DesignshashankОценок пока нет

- Interview QuestionsДокумент14 страницInterview QuestionsPreetha SeenuОценок пока нет

- Final PlacementReport-2016 PDFДокумент5 страницFinal PlacementReport-2016 PDFSukanta JanaОценок пока нет

- Assignment of Container Trucks of A Road Transport Company With Consideration of The Load Balancing ProblemДокумент14 страницAssignment of Container Trucks of A Road Transport Company With Consideration of The Load Balancing ProblemshashankОценок пока нет

- Getting The Pricing Right: Sumanta Basu Iim CalcuttaДокумент4 страницыGetting The Pricing Right: Sumanta Basu Iim CalcuttashashankОценок пока нет

- Feedback Form SanduДокумент5 страницFeedback Form SandushashankОценок пока нет

- Assignment of Container Trucks of A Road Transport Company With Consideration of The Load Balancing ProblemДокумент14 страницAssignment of Container Trucks of A Road Transport Company With Consideration of The Load Balancing ProblemshashankОценок пока нет

- Role of The Diciplinary CommitteeДокумент1 страницаRole of The Diciplinary CommitteeshashankОценок пока нет

- CA 6mar 22junДокумент2 страницыCA 6mar 22junshashankОценок пока нет

- Revenue Management at Harrah's Entertainment, Inc.: Transactions On EducationДокумент2 страницыRevenue Management at Harrah's Entertainment, Inc.: Transactions On EducationshashankОценок пока нет

- 870 3149 1 PBДокумент18 страниц870 3149 1 PBHannet Raja PreethaОценок пока нет

- Interview QuestionsДокумент14 страницInterview QuestionsPreetha SeenuОценок пока нет

- Multi Heineken q3Документ2 страницыMulti Heineken q3shashankОценок пока нет

- SMHC Taking Human Capital Seriously ReportДокумент22 страницыSMHC Taking Human Capital Seriously ReportshashankОценок пока нет

- Monthly GK Casule JuneДокумент19 страницMonthly GK Casule JuneshashankОценок пока нет

- Flip TopДокумент9 страницFlip TopshashankОценок пока нет

- CA 17feb 5marДокумент13 страницCA 17feb 5marshashankОценок пока нет

- Unit6 TeamProject TeamD FINAL 1334152599Документ21 страницаUnit6 TeamProject TeamD FINAL 1334152599shashankОценок пока нет

- Analysi S: Business Intellige NCEДокумент2 страницыAnalysi S: Business Intellige NCEshashankОценок пока нет

- SMHC Taking Human Capital Seriously ReportДокумент22 страницыSMHC Taking Human Capital Seriously ReportshashankОценок пока нет

- Market Research Questionnaire (Responses)Документ10 страницMarket Research Questionnaire (Responses)shashankОценок пока нет

- Consumer Based Brand EquityДокумент12 страницConsumer Based Brand EquityTonmoy BanerjeeОценок пока нет

- RJR Nabisco HBS Case SolutionДокумент13 страницRJR Nabisco HBS Case SolutionRattan Preet Singh25% (4)

- Sample Project ReportДокумент30 страницSample Project ReportPreeti VermaОценок пока нет

- Zaraitfinal Edit1 120826055208 Phpapp01Документ20 страницZaraitfinal Edit1 120826055208 Phpapp01Anuj SharmaОценок пока нет

- Zaraitfinal Edit1 120826055208 Phpapp01Документ20 страницZaraitfinal Edit1 120826055208 Phpapp01Anuj SharmaОценок пока нет

- Moore Medical CorporationДокумент6 страницMoore Medical Corporationbanerjeetania1989100% (1)

- CRMДокумент1 страницаCRMshashankОценок пока нет

- Register Offshore Company in Isle of Man in Tax HeavenДокумент5 страницRegister Offshore Company in Isle of Man in Tax HeavenZenron Consulting100% (1)

- A059 Banking LawДокумент11 страницA059 Banking LawRajeev TekwaniОценок пока нет

- Proforma Invoice: No-61, Om Sakthi Nagar, Madagadipet, Gstin/Uin: 34ABBFM1856E1ZK State Name: Puducherry, Code: 34Документ1 страницаProforma Invoice: No-61, Om Sakthi Nagar, Madagadipet, Gstin/Uin: 34ABBFM1856E1ZK State Name: Puducherry, Code: 34surajdoraОценок пока нет

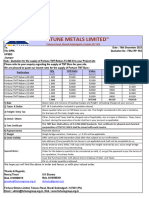

- "Fortune Metals Limited": Talwara Road, Mandi Gobindgarh, Punjab-147 301Документ1 страница"Fortune Metals Limited": Talwara Road, Mandi Gobindgarh, Punjab-147 301S K SharmaОценок пока нет

- Chapter 05 Final Income Taxation TableДокумент4 страницыChapter 05 Final Income Taxation TablejannyОценок пока нет

- Siva Prakash A/L Gunaseelan No 23 Jalan Seri Mersing 37 Kawasan 2 Taman Seri Andalas, 41200, KLANG, SELДокумент2 страницыSiva Prakash A/L Gunaseelan No 23 Jalan Seri Mersing 37 Kawasan 2 Taman Seri Andalas, 41200, KLANG, SELJaya PrathapОценок пока нет

- Morata Eaf 1stsemДокумент1 страницаMorata Eaf 1stsemLarry Rañoa LuuberioОценок пока нет

- Solutions To Problems: Pe On Estate TaxДокумент11 страницSolutions To Problems: Pe On Estate TaxErica NicolasuraОценок пока нет

- Hotel BillДокумент1 страницаHotel BillFahim MarwatОценок пока нет

- LO: 1, Bloom: AP, Difficulty: Simple, Time: 5-7, AACSB: Analytic, AICPA BB: Critical Thinking, AICPA FC: Reporting, AICPA PC: Problem SolvingДокумент2 страницыLO: 1, Bloom: AP, Difficulty: Simple, Time: 5-7, AACSB: Analytic, AICPA BB: Critical Thinking, AICPA FC: Reporting, AICPA PC: Problem Solving7seas498 7seas498Оценок пока нет

- Salary Slip NovДокумент1 страницаSalary Slip NovRahul RajawatОценок пока нет

- In-Del-Rpo: C-Dtp-AdiДокумент5 страницIn-Del-Rpo: C-Dtp-AdiShobhit SinghОценок пока нет

- DBM Compensation Policy Guidelines No. 98-1 (Page 1 of 2)Документ1 страницаDBM Compensation Policy Guidelines No. 98-1 (Page 1 of 2)Rej Francisco100% (1)

- Gross Estate IntroductionДокумент2 страницыGross Estate IntroductionJustz LimОценок пока нет

- Saviour Vridhi Price List 05-03-2023Документ1 страницаSaviour Vridhi Price List 05-03-2023gauravОценок пока нет

- Exercise # 5Документ1 страницаExercise # 5Mara Shaira SiegaОценок пока нет

- Taxation Pilot QuestionsxДокумент14 страницTaxation Pilot QuestionsxEmmanuel ObafemmyОценок пока нет

- Tax in Canada For NewcomersДокумент16 страницTax in Canada For NewcomersSamОценок пока нет

- Quiz - FINAL EXAMINATIONДокумент22 страницыQuiz - FINAL EXAMINATIONAisah ReemОценок пока нет

- Tax Compilation 2Документ85 страницTax Compilation 2Michelle Valdez AlvaroОценок пока нет

- Document PDFДокумент2 страницыDocument PDFFelicia PeralezОценок пока нет

- Books ListДокумент21 страницаBooks ListitsgutsyОценок пока нет

- In A NutshellДокумент3 страницыIn A NutshellJane TuazonОценок пока нет

- 12 Month Cash-FlowДокумент1 страница12 Month Cash-FlowSthembiso DladlaОценок пока нет

- Corporate Taxpayer Source of Income Tax Base Tax Rate Effectivity DateДокумент6 страницCorporate Taxpayer Source of Income Tax Base Tax Rate Effectivity DateZaaavnn VannnnnОценок пока нет

- MotionДокумент1 страницаMotionRuben GarciaОценок пока нет

- 46927-Folio BaymontДокумент1 страница46927-Folio BaymontOctavio ChableОценок пока нет

- Final Tax ReviewerДокумент35 страницFinal Tax Revieweryza100% (1)

- No Article Code Article Decsription Article Group Qty Amount Qty Return Return Amount Qty Nett Amount NettoДокумент1 страницаNo Article Code Article Decsription Article Group Qty Amount Qty Return Return Amount Qty Nett Amount Nettomabaranjay1987Оценок пока нет

- FEES LIST 2021-2022: Monthly OptionДокумент5 страницFEES LIST 2021-2022: Monthly OptionCristina IlasciucОценок пока нет