Вам также может понравиться

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- BSF 4Документ17 страницBSF 4api-158285296Оценок пока нет

- Online Banking System of DBBL: 4.1 DBBL W N Ict I FДокумент15 страницOnline Banking System of DBBL: 4.1 DBBL W N Ict I FMrinmoyi ChowdhuryОценок пока нет

- Winter Park Hotel Case Analysis: Nirmit Doshi 15 Sadaf Khan 26 Himanshu Jha 25 Mohit Vyas 60 Saloni Sharma 56Документ7 страницWinter Park Hotel Case Analysis: Nirmit Doshi 15 Sadaf Khan 26 Himanshu Jha 25 Mohit Vyas 60 Saloni Sharma 56Azenith Margarette CayetanoОценок пока нет

- Terms and Conditions For N26 Mastercard" From N26 Bank GMBH For Private and Business Mastercard Debit CardsДокумент12 страницTerms and Conditions For N26 Mastercard" From N26 Bank GMBH For Private and Business Mastercard Debit CardsCrow CrowОценок пока нет

- EC604 - Embedded Systems - Course MaterialsДокумент375 страницEC604 - Embedded Systems - Course MaterialsManu ManuОценок пока нет

- ITE 3106 - Lesson 03 - Application ArchitecturesДокумент14 страницITE 3106 - Lesson 03 - Application ArchitecturesJeewaka JayanathОценок пока нет

- Emerging Modes of Business - Part 3: ObjectivesДокумент11 страницEmerging Modes of Business - Part 3: ObjectivesSanta GlenmarkОценок пока нет

- HHH1Документ24 страницыHHH1Sitan Kumar SahooОценок пока нет

- VEGA Series Operation and Maintenance Manual PDFДокумент120 страницVEGA Series Operation and Maintenance Manual PDFNelson Enrique Orjuela TorresОценок пока нет

- The Karur Vysya Bank LimitedДокумент11 страницThe Karur Vysya Bank LimitedmithradharunОценок пока нет

- Southern Cable - Detailed ProceduresДокумент41 страницаSouthern Cable - Detailed ProceduresfaizalОценок пока нет

- Internship Report On Prabhu Bank, Nepal by Siddhant Kumar Chaudhary.Документ36 страницInternship Report On Prabhu Bank, Nepal by Siddhant Kumar Chaudhary.Siddhant Chaudhary56% (18)

- Dealer Price List - January 2018 PDFДокумент6 страницDealer Price List - January 2018 PDFEdmond אדמונד KachaleОценок пока нет

- Base 24Документ58 страницBase 24machindrakapade555Оценок пока нет

- Bank StatemntДокумент1 страницаBank StatemntEnixam ZulevtОценок пока нет

- Abu Bakkar Sani Askkari ExpДокумент234 страницыAbu Bakkar Sani Askkari Expmalik omerОценок пока нет

- Casa StrategyДокумент2 страницыCasa StrategyS.s.SubramanianОценок пока нет

- Literature Survey (1) Smart Atm Security System Using FPR, GSM, GpsДокумент2 страницыLiterature Survey (1) Smart Atm Security System Using FPR, GSM, GpsRAMADEVI KESANAОценок пока нет

- DD MM Y Y Y Y N Y: Current AccountДокумент2 страницыDD MM Y Y Y Y N Y: Current AccountjithgrucoОценок пока нет

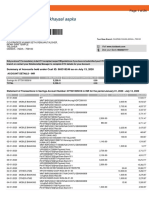

- Account Statement From 1 Apr 2021 To 28 Feb 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент2 страницыAccount Statement From 1 Apr 2021 To 28 Feb 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceAPPLE MARINEОценок пока нет

- MX8700 1Документ2 страницыMX8700 1MariyappanSubhash100% (1)

- Money and Banking TerminologyДокумент3 страницыMoney and Banking TerminologythamiztОценок пока нет

- Test Case For AtmДокумент2 страницыTest Case For AtmpriyanshuОценок пока нет

- Birhan Final Thesis PaperДокумент109 страницBirhan Final Thesis PaperyibeltalОценок пока нет

- Cis2303-Systems Analysis and Design: CLO2: Create Behavioral Models To Document System RequirementsДокумент44 страницыCis2303-Systems Analysis and Design: CLO2: Create Behavioral Models To Document System RequirementsRimsha NisarОценок пока нет

- Happay Card 8935Документ4 страницыHappay Card 8935KОценок пока нет

- NBP Bank ChargesДокумент28 страницNBP Bank Chargesayub_balticОценок пока нет

- Atm Report LatestДокумент11 страницAtm Report LatesttarvinrajОценок пока нет

- Internship Report On "Credit Cards of South East Bank LTD.": Submitted ToДокумент26 страницInternship Report On "Credit Cards of South East Bank LTD.": Submitted ToTushar ShahiОценок пока нет

- Atm With JavaДокумент24 страницыAtm With Javakirti_gupta100% (1)