Вам также может понравиться

- Section 9Документ7 страницSection 9Achulendra Ji PushkarОценок пока нет

- Income Deemed To Accrue or Arise in India-Sec 9Документ16 страницIncome Deemed To Accrue or Arise in India-Sec 9drive8124Оценок пока нет

- 9Документ4 страницы9SPARSH KAPOORОценок пока нет

- Week 4-7Документ9 страницWeek 4-7Vijayant DalalОценок пока нет

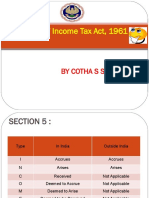

- Section 5 of Income Tax ActДокумент4 страницыSection 5 of Income Tax ActParth PandeyОценок пока нет

- Sec 9Документ39 страницSec 9Akanksha BohraОценок пока нет

- Definitions Residence and Tax LiabilityДокумент23 страницыDefinitions Residence and Tax LiabilityVicky DОценок пока нет

- The Direct Taxes CodeДокумент3 страницыThe Direct Taxes Codeanuj91Оценок пока нет

- Residential Status DC 2023-24Документ11 страницResidential Status DC 2023-24avinashhpv7785Оценок пока нет

- Basis of Charge Charge of Income-Tax. 4Документ11 страницBasis of Charge Charge of Income-Tax. 4poonamntpcОценок пока нет

- Income Tax ActДокумент12 страницIncome Tax ActSomnath GuptaОценок пока нет

- Residential StatusДокумент9 страницResidential Statussadhana20bbaОценок пока нет

- Unit 3Документ20 страницUnit 3Ram KrishnaОценок пока нет

- Section - 5Документ1 страницаSection - 5waqtkeebaatein12Оценок пока нет

- 01 Section 9Документ54 страницы01 Section 9ABHIJEETОценок пока нет

- Benefits Available To Non ResidentsДокумент16 страницBenefits Available To Non ResidentsArchita TiwariОценок пока нет

- Person (Section 2 (31) )Документ1 страницаPerson (Section 2 (31) )Tejas PandeyОценок пока нет

- Taxation Residential Status and Appeal ProvisionsДокумент47 страницTaxation Residential Status and Appeal ProvisionsSamata BohraОценок пока нет

- Model Answers Taxation 1. Residential Status of Assessee Under IT Act ?Документ44 страницыModel Answers Taxation 1. Residential Status of Assessee Under IT Act ?Tejasvini KhemajiОценок пока нет

- CHAPTER:-1 Definitions U/s - 2, Basis of Charge and Exclusions From Total IncomeДокумент12 страницCHAPTER:-1 Definitions U/s - 2, Basis of Charge and Exclusions From Total IncomeshyamiliОценок пока нет

- Section 64: Incomes Which Do Not Form Part of Total Income Incomes Not Included in Total Income. 10Документ33 страницыSection 64: Incomes Which Do Not Form Part of Total Income Incomes Not Included in Total Income. 10Mandar RaneОценок пока нет

- Tax NotesДокумент11 страницTax NotesVishal DeshwalОценок пока нет

- Direct Tax Summary NotesДокумент88 страницDirect Tax Summary NotesAlisha LukeОценок пока нет

- 2 Residential StatusДокумент30 страниц2 Residential StatusVEDANT SAINIОценок пока нет

- Model Answers Law of TaxationДокумент46 страницModel Answers Law of Taxationlavkush1234Оценок пока нет

- Sia - Itax-2018-19Документ17 страницSia - Itax-2018-19Abhay Pethani.Оценок пока нет

- Scope of Total Income and Residential StatusДокумент3 страницыScope of Total Income and Residential StatusSandeep SinghОценок пока нет

- Law of Taxation Law of Taxation Class Notes CompressДокумент48 страницLaw of Taxation Law of Taxation Class Notes CompressThrishul MaheshОценок пока нет

- Sec. 6Документ15 страницSec. 6Akanksha BohraОценок пока нет

- Residential Status Cma IndaДокумент10 страницResidential Status Cma IndaKiran ChristyОценок пока нет

- Principle of TaxationДокумент7 страницPrinciple of TaxationAnas YawarОценок пока нет

- Day4 Residential Status and Incidence of Tax (9 Oct)Документ12 страницDay4 Residential Status and Incidence of Tax (9 Oct)1986anuОценок пока нет

- It Act Sec 10Документ39 страницIt Act Sec 10Ramod SayedОценок пока нет

- Q1) (A) Person - Section 2Документ5 страницQ1) (A) Person - Section 2Minal GandhiОценок пока нет

- Residence in IndiaДокумент7 страницResidence in IndiaSuryaОценок пока нет

- Incomes Which Do Not Form Part of Total Income: Section 64Документ91 страницаIncomes Which Do Not Form Part of Total Income: Section 64d-fbuser-65596417Оценок пока нет

- Residential Status and its Impact on Tax LiabilityДокумент25 страницResidential Status and its Impact on Tax LiabilityPJ 123Оценок пока нет

- Relevant Provisions of Income-Tax Act, 1961: Section 6Документ4 страницыRelevant Provisions of Income-Tax Act, 1961: Section 6ABC 123Оценок пока нет

- Residential Status and Incidence of Tax - Study MaterialДокумент6 страницResidential Status and Incidence of Tax - Study MaterialEmeline SoroОценок пока нет

- Residential Status and Scope of Total Income - AY 2023 - 24Документ12 страницResidential Status and Scope of Total Income - AY 2023 - 24Rajan SundararajanОценок пока нет

- TaxationДокумент15 страницTaxationharshithaaba8Оценок пока нет

- Chapter-2 Residential StatusДокумент5 страницChapter-2 Residential StatusBrinda RОценок пока нет

- Income Deemed To Arise in IndiaДокумент7 страницIncome Deemed To Arise in IndiaDebaОценок пока нет

- Residential Status and Tax IncidenceДокумент46 страницResidential Status and Tax IncidenceÄbhíñävJäíñОценок пока нет

- UNIT 1 - CT - Part 1Документ39 страницUNIT 1 - CT - Part 1Amogh AroraОценок пока нет

- ch-11 Taxation of NRIsДокумент25 страницch-11 Taxation of NRIsdean.socОценок пока нет

- Excemptions Under Section 10Документ52 страницыExcemptions Under Section 10anuragmamgainОценок пока нет

- Corporate Tax Planning Unit-2 E-Text Module 5 & 6: Residential Status & Taxation of Companies Scope of Total Incidence of Tax (Section 5)Документ10 страницCorporate Tax Planning Unit-2 E-Text Module 5 & 6: Residential Status & Taxation of Companies Scope of Total Incidence of Tax (Section 5)imamОценок пока нет

- Residential Status and Scope of Total IncomeДокумент5 страницResidential Status and Scope of Total IncomeMnk BhkОценок пока нет

- Permanent Esta researchДокумент24 страницыPermanent Esta researchNeha PandeyОценок пока нет

- CTP MergedДокумент146 страницCTP MergedRadhika ShingankuliОценок пока нет

- Residential Status: A Project On Residential Status in India and The Effects of Tax On It. Made By: Somrita PalДокумент17 страницResidential Status: A Project On Residential Status in India and The Effects of Tax On It. Made By: Somrita Palsousam2387Оценок пока нет

- Direct Tax Code SummaryДокумент6 страницDirect Tax Code SummaryShalini MahawarОценок пока нет

- 1328866787Chp 2 - Residence and Scope of Total IncomeДокумент5 страниц1328866787Chp 2 - Residence and Scope of Total IncomeMohiОценок пока нет

- Study Note - 13: Incomes Which Do Not Form Part of Total IncomeДокумент37 страницStudy Note - 13: Incomes Which Do Not Form Part of Total Incomes4sahithОценок пока нет

- Marketing GRP 3Документ75 страницMarketing GRP 3Shivlal YadavОценок пока нет

- Residential Status: Vaibhav BanjanДокумент14 страницResidential Status: Vaibhav Banjandeepika gawasОценок пока нет

- Residential status determination for individualsДокумент14 страницResidential status determination for individualsdhananjay7Оценок пока нет

- Residential Status and Tax IncidenceДокумент3 страницыResidential Status and Tax Incidenceambarishan mrОценок пока нет

- July 2218Документ17 страницJuly 2218Nisseem KrishnaОценок пока нет

- July 2418Документ28 страницJuly 2418Nisseem KrishnaОценок пока нет

- AssignmentsДокумент2 страницыAssignmentsNisseem KrishnaОценок пока нет

- Final GK Power Capsule For Rbi Assistant Mains 2017 by Gopal Sir and TeamДокумент66 страницFinal GK Power Capsule For Rbi Assistant Mains 2017 by Gopal Sir and TeamJagannath JagguОценок пока нет

- Nelp and HelpДокумент14 страницNelp and HelpNisseem KrishnaОценок пока нет

- Max Weber On The Rationalization of Law - Dianne Galea - AcademiaДокумент4 страницыMax Weber On The Rationalization of Law - Dianne Galea - AcademiaNisseem KrishnaОценок пока нет

- Debate For Women and Criminal LawДокумент2 страницыDebate For Women and Criminal LawNisseem KrishnaОценок пока нет

- Ccea Approves Selling 51% Stake in HPCL To OngcДокумент1 страницаCcea Approves Selling 51% Stake in HPCL To OngcNisseem KrishnaОценок пока нет

- Legal System in Mughal IndiaДокумент26 страницLegal System in Mughal IndiaNisseem Krishna100% (1)

- Parmalat ScandalДокумент10 страницParmalat ScandalNisseem KrishnaОценок пока нет

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 05 - Chapter 1 PDFДокумент18 страниц05 - Chapter 1 PDFNisseem KrishnaОценок пока нет

- 22feb2010 - L and T Launches Its Asset Management OperationsДокумент4 страницы22feb2010 - L and T Launches Its Asset Management OperationsNisseem KrishnaОценок пока нет

- 7580 22057 1 PBДокумент8 страниц7580 22057 1 PBNisseem KrishnaОценок пока нет

- Digital Image Processing: Minakshi KumarДокумент22 страницыDigital Image Processing: Minakshi KumarNikhil SoniОценок пока нет

- Eyewitness TestimonyДокумент13 страницEyewitness TestimonynisseemkОценок пока нет

- Important Constitutional ProvisionsДокумент8 страницImportant Constitutional ProvisionsNisseem KrishnaОценок пока нет

- History Class10 TN Board PDFДокумент109 страницHistory Class10 TN Board PDFMayank PandeyОценок пока нет

- Digital Image Processing: Minakshi KumarДокумент22 страницыDigital Image Processing: Minakshi KumarNikhil SoniОценок пока нет

- SSC CGL 2014 Cut OffДокумент2 страницыSSC CGL 2014 Cut OffRaghu RamОценок пока нет

- 05 Chapter 2Документ0 страниц05 Chapter 2Abhishek MalhotraОценок пока нет

- Sikh Gurrdwara Act1925Документ138 страницSikh Gurrdwara Act1925Andrea GreeneОценок пока нет

- Nava Bharat-2013-2014Документ180 страницNava Bharat-2013-2014SUKHSAGAR1969Оценок пока нет

- Cir Vs Metro Star SuperamaДокумент2 страницыCir Vs Metro Star SuperamaDonna TreceñeОценок пока нет

- Machine Learning and Credit Ratings Prediction in The Age of Fourth IndustrialДокумент13 страницMachine Learning and Credit Ratings Prediction in The Age of Fourth IndustrialJorge Luis SorianoОценок пока нет

- Solutions To Exercises and Problems - Budgeting: GivenДокумент8 страницSolutions To Exercises and Problems - Budgeting: GivenTiến AnhОценок пока нет

- NC-III Bookkeeping Reviewer NC-III Bookkeeping ReviewerДокумент34 страницыNC-III Bookkeeping Reviewer NC-III Bookkeeping ReviewerSheila Mae Lira100% (2)

- RCBC vs Alfa RTW Manufacturing Corp Bank Loan Dispute DecisionДокумент6 страницRCBC vs Alfa RTW Manufacturing Corp Bank Loan Dispute DecisionAlecsandra ChuОценок пока нет

- CRC-ACE REVIEW SCHOOL PA1 SECOND PRE-BOARD EXAMSДокумент6 страницCRC-ACE REVIEW SCHOOL PA1 SECOND PRE-BOARD EXAMSRovern Keith Oro CuencaОценок пока нет

- No. 13 EMHДокумент33 страницыNo. 13 EMHayazОценок пока нет

- Consistent Compounders: An Investment Strategy by Marcellus Investment ManagersДокумент27 страницConsistent Compounders: An Investment Strategy by Marcellus Investment Managersvra_pОценок пока нет

- Formation of Partnership: Valuation of Assets and Liabilities ContributedДокумент12 страницFormation of Partnership: Valuation of Assets and Liabilities ContributedThe Brain Dump PHОценок пока нет

- Square To Launch Baby Diapers To Meet Growing DemandДокумент2 страницыSquare To Launch Baby Diapers To Meet Growing DemandSa'ad Abd Ar RafieОценок пока нет

- ანგარიშგება PDFДокумент39 страницანგარიშგება PDFSandro ChanturidzeОценок пока нет

- Vip No.8 - MeslДокумент4 страницыVip No.8 - Meslkj gandaОценок пока нет

- Cash Flow and Financial PlanningДокумент64 страницыCash Flow and Financial PlanningKARL PASCUAОценок пока нет

- A Project Report On Microfinance in IndiaДокумент73 страницыA Project Report On Microfinance in IndiaAjinkya ManeОценок пока нет

- Britannia IndsДокумент16 страницBritannia IndsbysqqqdxОценок пока нет

- Practice Quiz - Review of Working CapitalДокумент9 страницPractice Quiz - Review of Working Capitalcharisse nuevaОценок пока нет

- The MBA DecisionДокумент7 страницThe MBA DecisionFiry YuanditaОценок пока нет

- SAP Global Implementation Conceptual-Design-Of-Finance and ControllingДокумент172 страницыSAP Global Implementation Conceptual-Design-Of-Finance and Controllingprakhar31Оценок пока нет

- SAS® Financial Management 5.5 Formula GuideДокумент202 страницыSAS® Financial Management 5.5 Formula Guidejohannadiaz87Оценок пока нет

- TaxДокумент18 страницTaxPatrickBeronaОценок пока нет

- Flyleaf BooksДокумент32 страницыFlyleaf BooksAzhar MajothiОценок пока нет

- Comair AnnualReportДокумент76 страницComair AnnualReportJanus CoetzeeОценок пока нет

- Role of Derivatives in Economic Growth and DevelopmentДокумент22 страницыRole of Derivatives in Economic Growth and DevelopmentKanika AnejaОценок пока нет

- BASO Presentation PDFДокумент25 страницBASO Presentation PDFGEOEXPLOREMINPERU MINERÍA Y GEOLOGIAОценок пока нет

- QUIZДокумент15 страницQUIZCarlo ConsuegraОценок пока нет

- 1st PB-TAДокумент12 страниц1st PB-TAGlenn Patrick de LeonОценок пока нет

- FRM 2015 Part 1 Practice ExamДокумент47 страницFRM 2015 Part 1 Practice ExamVitor SalgadoОценок пока нет

- Lembar Jawaban 1 UPK (Kevin J)Документ12 страницLembar Jawaban 1 UPK (Kevin J)kevin jonathanОценок пока нет

- Kirsty Nathoo - Startup Finance Pitfalls and How To Avoid ThemДокумент33 страницыKirsty Nathoo - Startup Finance Pitfalls and How To Avoid ThemMurali MohanОценок пока нет