Вам также может понравиться

- Lecture 10 Options StrategiesДокумент28 страницLecture 10 Options Strategiessachin rolaОценок пока нет

- A Presentation On: Trading StrategiesДокумент26 страницA Presentation On: Trading StrategiessumitkjhamОценок пока нет

- Options Valuation GuideДокумент72 страницыOptions Valuation GuideZia AhmadОценок пока нет

- Futures Pricing Formula - 5paisa - 5pschool PDFДокумент9 страницFutures Pricing Formula - 5paisa - 5pschool PDFaasdadОценок пока нет

- F& o StrategiesДокумент22 страницыF& o StrategiesprachirosesОценок пока нет

- ArthaSutra - Day 1Документ7 страницArthaSutra - Day 1phoenixankurОценок пока нет

- Lecture Option and DerivativeДокумент15 страницLecture Option and Derivativeazkunaga_economistОценок пока нет

- Financial Products & ServicesДокумент72 страницыFinancial Products & ServicesMuhammad Shahzad KhurramОценок пока нет

- Basic Option StrategiesДокумент48 страницBasic Option StrategiesRahimullah QaziОценок пока нет

- Options U MastersДокумент30 страницOptions U MastersHernan DiazОценок пока нет

- Covered Call WritingДокумент11 страницCovered Call WritingChris ArmourОценок пока нет

- Options StrategiesДокумент18 страницOptions StrategiesShuting Teoh0% (1)

- Long StraddleДокумент13 страницLong Straddleraj0386100% (1)

- Risk Management Strategies Using Option ApplicationsДокумент15 страницRisk Management Strategies Using Option ApplicationsTejas JoshiОценок пока нет

- Long Stock Short Call strategyДокумент8 страницLong Stock Short Call strategyRachelJosefОценок пока нет

- Lecture8 OptionsTrading StrategiesДокумент21 страницаLecture8 OptionsTrading StrategiesRasesh ShahОценок пока нет

- Hedging StrategiesДокумент10 страницHedging StrategiesLakshman Kumar YalamatiОценок пока нет

- SM OtsmДокумент59 страницSM OtsmshraddhapОценок пока нет

- Covered CallДокумент4 страницыCovered CallpkkothariОценок пока нет

- The Covered CallДокумент8 страницThe Covered CallpilluОценок пока нет

- DerivativesДокумент81 страницаDerivativessreekala spОценок пока нет

- DerivativesДокумент44 страницыDerivativesKhyati KariaОценок пока нет

- T9 OptionsДокумент49 страницT9 Optionsnilanjan1969Оценок пока нет

- Welcome To The Presentation ON Option StrategiesДокумент13 страницWelcome To The Presentation ON Option StrategiesVarun BansalОценок пока нет

- Predicting Option Prices and Volatility With High Frequency Data Using Neural NetworkДокумент3 страницыPredicting Option Prices and Volatility With High Frequency Data Using Neural NetworkBOHR International Journal of Finance and Market Research (BIJFMR)Оценок пока нет

- Chapter 3-Hedging Strategies Using Futures-29.01.2014Документ26 страницChapter 3-Hedging Strategies Using Futures-29.01.2014abaig2011Оценок пока нет

- Hedging Strategies Using FuturesДокумент19 страницHedging Strategies Using FuturesMrunaal NaseryОценок пока нет

- A Simple Options Trading Strategy Based On Technical IndicatorsДокумент4 страницыA Simple Options Trading Strategy Based On Technical IndicatorsMnvd prasadОценок пока нет

- NISM Equity Derivatives Chapter - 5Документ68 страницNISM Equity Derivatives Chapter - 5AakashОценок пока нет

- Lecture 4-Hedging With FuturesДокумент36 страницLecture 4-Hedging With FuturesNIAZ ALI KHANОценок пока нет

- Moneyblock Option StrategiesДокумент15 страницMoneyblock Option Strategiespipgorilla100% (1)

- Synthetic Options ExplainedДокумент6 страницSynthetic Options ExplainedSamuelPerezОценок пока нет

- Covered Call Strategies P1 PDFДокумент10 страницCovered Call Strategies P1 PDFThành Tâm DươngОценок пока нет

- On The Volatility of Volatility: Electronic Address: Hsu@duende - Uoregon.edu Electronic Address: Bmurray1@uoregon - EduДокумент15 страницOn The Volatility of Volatility: Electronic Address: Hsu@duende - Uoregon.edu Electronic Address: Bmurray1@uoregon - EduKelvin LeungОценок пока нет

- Assignment On: Marter'S of Business Economics (MBE)Документ19 страницAssignment On: Marter'S of Business Economics (MBE)88chauhanОценок пока нет

- Binomial Tree Option Pricing ModelДокумент22 страницыBinomial Tree Option Pricing ModelXavier Francis S. LutaloОценок пока нет

- OptionsДокумент44 страницыOptionskamdica100% (1)

- Learn the Basics of Buying Put OptionsДокумент11 страницLearn the Basics of Buying Put OptionsRajan kumar singhОценок пока нет

- Options Strategies Explained in DetailДокумент22 страницыOptions Strategies Explained in DetailMahesh GujarОценок пока нет

- Black-Scholes Excel Formulas and How To Create A Simple Option Pricing Spreadsheet - MacroptionДокумент8 страницBlack-Scholes Excel Formulas and How To Create A Simple Option Pricing Spreadsheet - MacroptionDickson phiriОценок пока нет

- Theory of Volatility TradingДокумент22 страницыTheory of Volatility TradingJulien AlleraОценок пока нет

- Volatility Information Trading in The Option MarketДокумент33 страницыVolatility Information Trading in The Option MarketTiffany HollandОценок пока нет

- Index Futures PricingДокумент21 страницаIndex Futures PricingVaidyanathan RavichandranОценок пока нет

- SDFSDFДокумент51 страницаSDFSDFranaprathap_rpОценок пока нет

- Option GreeksДокумент2 страницыOption GreeksajjupОценок пока нет

- Black-Scholes Option PricingДокумент11 страницBlack-Scholes Option PricingtraderescortОценок пока нет

- Strategy Guide: Bull Call SpreadДокумент14 страницStrategy Guide: Bull Call SpreadworkОценок пока нет

- Options Basics Tutorial: Best Brokers For Options TradingДокумент33 страницыOptions Basics Tutorial: Best Brokers For Options TradingasadrekarimiОценок пока нет

- Covered Calls and Their Unintended Reversal BetДокумент11 страницCovered Calls and Their Unintended Reversal BetDeep Value Insight100% (1)

- Calculate call option value using two-state stock price modelДокумент16 страницCalculate call option value using two-state stock price modelMarissa MarissaОценок пока нет

- Topic 4 Risk ReturnДокумент48 страницTopic 4 Risk ReturnBulan Bintang MatahariОценок пока нет

- Chapter 3.2 Futures HedgingДокумент19 страницChapter 3.2 Futures HedginglelouchОценок пока нет

- Butterfly Spread OptionДокумент8 страницButterfly Spread OptionVivek Singh RanaОценок пока нет

- Bear Put Spread: Montréal ExchangeДокумент2 страницыBear Put Spread: Montréal ExchangepkkothariОценок пока нет

- Chapter 9 Options Markets MechanicsДокумент35 страницChapter 9 Options Markets MechanicsAllen GrceОценок пока нет

- Intro To OptionsДокумент22 страницыIntro To OptionsFatima MosawiОценок пока нет

- Risky InvestmentДокумент35 страницRisky InvestmentbellohalesОценок пока нет

- CH 30092017 1Документ1 страницаCH 30092017 1MohitОценок пока нет

- Requirement A.: Year Cash Flows 0 - $ 8,210.00 1 $ 6,220.00 2 $ 20,400.00Документ1 страницаRequirement A.: Year Cash Flows 0 - $ 8,210.00 1 $ 6,220.00 2 $ 20,400.00MohitОценок пока нет

- Cash Flows From Operating ActivitiesДокумент1 страницаCash Flows From Operating ActivitiesMohitОценок пока нет

- CH 11082017 5Документ2 страницыCH 11082017 5MohitОценок пока нет

- CH 22062017 1Документ9 страницCH 22062017 1MohitОценок пока нет

- CH 18072017 1Документ1 страницаCH 18072017 1MohitОценок пока нет

- CH 11072017 1Документ2 страницыCH 11072017 1MohitОценок пока нет

- Item Discount Factor Workings PVДокумент2 страницыItem Discount Factor Workings PVMohitОценок пока нет

- CH 09082017 1Документ4 страницыCH 09082017 1MohitОценок пока нет

- CH 03072017 1Документ1 страницаCH 03072017 1MohitОценок пока нет

- Requirement (A) : Post Tax Operating Cash Flows (A) 165.75Документ3 страницыRequirement (A) : Post Tax Operating Cash Flows (A) 165.75MohitОценок пока нет

- CH 19062017 5Документ1 страницаCH 19062017 5MohitОценок пока нет

- CH 11072017 1Документ2 страницыCH 11072017 1MohitОценок пока нет

- CH 08072017 1Документ1 страницаCH 08072017 1MohitОценок пока нет

- CH 18072017 1Документ1 страницаCH 18072017 1MohitОценок пока нет

- Statement of Problem With The Trial Balance Still Balance? What Is The Amount of Difference? Which Trial Balance Column Have The Larger Total?Документ1 страницаStatement of Problem With The Trial Balance Still Balance? What Is The Amount of Difference? Which Trial Balance Column Have The Larger Total?MohitОценок пока нет

- CH 22042017 2Документ10 страницCH 22042017 2MohitОценок пока нет

- Requirement (A) : Post Tax Operating Cash Flows (A) 165.75Документ3 страницыRequirement (A) : Post Tax Operating Cash Flows (A) 165.75MohitОценок пока нет

- Alternative A Alternative B Alternative CДокумент9 страницAlternative A Alternative B Alternative CMohitОценок пока нет

- CH 25032017 3Документ1 страницаCH 25032017 3MohitОценок пока нет

- CH 26032017 7Документ2 страницыCH 26032017 7MohitОценок пока нет

- Financial analysis and NPV calculation of a company over 5 yearsДокумент3 страницыFinancial analysis and NPV calculation of a company over 5 yearsMohitОценок пока нет

- CH 01022017 6Документ3 страницыCH 01022017 6MohitОценок пока нет

- CH 04042017 3Документ1 страницаCH 04042017 3MohitОценок пока нет

- Calculating variable overhead, fixed overhead, estimated costs, work in process, and material costsДокумент1 страницаCalculating variable overhead, fixed overhead, estimated costs, work in process, and material costsMohitОценок пока нет

- CH 05032017 7Документ1 страницаCH 05032017 7MohitОценок пока нет

- CH 06032017 2Документ1 страницаCH 06032017 2MohitОценок пока нет

- CH 06032017 11Документ1 страницаCH 06032017 11MohitОценок пока нет

- ElmwoodДокумент3 страницыElmwoodMohitОценок пока нет

- CH 30012017 6 1Документ2 страницыCH 30012017 6 1MohitОценок пока нет

- Loyal VC - Brief and Invite DetailsДокумент1 страницаLoyal VC - Brief and Invite DetailsmchroОценок пока нет

- Ratio Analysis 3Документ4 страницыRatio Analysis 3Vinay ChhedaОценок пока нет

- ABC L3 Past Paper Series 3 2013Документ7 страницABC L3 Past Paper Series 3 2013b3nzyОценок пока нет

- Use IGST credit for payment of IGSTДокумент10 страницUse IGST credit for payment of IGSTD Y Patil Institute of MCA and MBAОценок пока нет

- Gainesboro Machine Tools Corporation: Other Cases in Which Dividend Policy Is An Important IssueДокумент22 страницыGainesboro Machine Tools Corporation: Other Cases in Which Dividend Policy Is An Important IssueUshnaОценок пока нет

- Chapter 3 ReceivablesДокумент22 страницыChapter 3 ReceivablesCale Robert RascoОценок пока нет

- Financial Statement Analysis TechniquesДокумент8 страницFinancial Statement Analysis TechniquesJomar VillenaОценок пока нет

- Security Analysis and Portfolio Management Questions and AnswersДокумент15 страницSecurity Analysis and Portfolio Management Questions and AnswersPashminaDoshiОценок пока нет

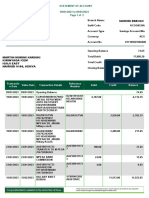

- Martin Murimi KariukiДокумент2 страницыMartin Murimi KariukiKameneja LeeОценок пока нет

- Capital StructureДокумент41 страницаCapital StructurethejojoseОценок пока нет

- Receipt 1 PDFДокумент3 страницыReceipt 1 PDFsomenathbasakОценок пока нет

- Pledging of ReceivablesДокумент2 страницыPledging of ReceivablesPrince Alexis GarciaОценок пока нет

- Petroflo Trading Company: Cash Payment VoucherДокумент10 страницPetroflo Trading Company: Cash Payment Vouchermuhammad ihtishamОценок пока нет

- 3 - 0607 - Making Capital Investment Decisions. Risk Analysis, Real OptionsДокумент3 страницы3 - 0607 - Making Capital Investment Decisions. Risk Analysis, Real OptionsPham Ngoc VanОценок пока нет

- Equicapita Signs Agreement With ATB Corporate Financial Services For Acquisition FacilityДокумент2 страницыEquicapita Signs Agreement With ATB Corporate Financial Services For Acquisition FacilityEquicapita Income TrustОценок пока нет

- Detailed Solutions To Problem 5Документ3 страницыDetailed Solutions To Problem 5Maria AngelicaОценок пока нет

- Measure and Manage Credit and Counterparty RiskДокумент1 страницаMeasure and Manage Credit and Counterparty RiskjupeeОценок пока нет

- Hill Country CaseДокумент5 страницHill Country CaseDeepansh Kakkar100% (1)

- IDBI Bank: This Article Has Multiple Issues. Please HelpДокумент15 страницIDBI Bank: This Article Has Multiple Issues. Please HelpmayurivinothОценок пока нет

- TMA Divergence Indicator Script For Trading ViewДокумент5 страницTMA Divergence Indicator Script For Trading ViewKrish Karaniya50% (2)

- Corporate and Retail BankingДокумент13 страницCorporate and Retail Bankingbipin kumarОценок пока нет

- Balance SheetДокумент28 страницBalance SheetrimaОценок пока нет

- Ias 16Документ31 страницаIas 16Reever RiverОценок пока нет

- Tally AssignmentДокумент3 страницыTally AssignmentSoumya LatheyОценок пока нет

- C Statment - Ivan Maleakhi - Des 2020Документ4 страницыC Statment - Ivan Maleakhi - Des 2020Budi ArtantoОценок пока нет

- Cash Flow QuestionsДокумент6 страницCash Flow QuestionsnapsdОценок пока нет

- Accounting September Memo 2016Документ18 страницAccounting September Memo 2016Jester LabanОценок пока нет

- Course OutlineДокумент8 страницCourse OutlineLaxman KeshavОценок пока нет

- BSN Giro Account Statement for Alister MaribenДокумент4 страницыBSN Giro Account Statement for Alister MaribenAlister MaribenОценок пока нет

- Zimbabwe's Transitional Stabilisation Programme Reforms AgendaДокумент74 страницыZimbabwe's Transitional Stabilisation Programme Reforms AgendaAaron KuudzeremaОценок пока нет