Вам также может понравиться

- Botakoz Kasumbekova European Resttlement in TJK 2011Документ18 страницBotakoz Kasumbekova European Resttlement in TJK 2011amudaryoОценок пока нет

- Call For Papers Nordic Conf March 182 2018pdfДокумент2 страницыCall For Papers Nordic Conf March 182 2018pdfamudaryoОценок пока нет

- Verhoeven Multiyear Budget and Fiscal Performance 2014Документ17 страницVerhoeven Multiyear Budget and Fiscal Performance 2014amudaryoОценок пока нет

- Taxotere NewДокумент3 страницыTaxotere NewamudaryoОценок пока нет

- Brexit and UK 2017Документ50 страницBrexit and UK 2017amudaryoОценок пока нет

- PowerPoint Tutorial - PowerPoint BasicsДокумент22 страницыPowerPoint Tutorial - PowerPoint Basicsdorje@blueyonder.co.ukОценок пока нет

- Suyarkulova Uzbek An Elementary Textbook 2012Документ3 страницыSuyarkulova Uzbek An Elementary Textbook 2012amudaryoОценок пока нет

- John Keats PoemsДокумент5 страницJohn Keats PoemsamudaryoОценок пока нет

- Deloitte Global Value Chain 2015Документ96 страницDeloitte Global Value Chain 2015amudaryoОценок пока нет

- Ban 2015 GovernanceДокумент17 страницBan 2015 GovernanceamudaryoОценок пока нет

- Do Balanced Budget Laws Matter in RecessionsДокумент1 страницаDo Balanced Budget Laws Matter in RecessionsamudaryoОценок пока нет

- Scholarforum Migrationcentral Asia and Mongolia 20160603Документ24 страницыScholarforum Migrationcentral Asia and Mongolia 20160603amudaryoОценок пока нет

- WS Minto PosterДокумент1 страницаWS Minto PosteramudaryoОценок пока нет

- Fritz Strengthening PFM 2014Документ55 страницFritz Strengthening PFM 2014amudaryoОценок пока нет

- PowerPoint Tutorial - PowerPoint BasicsДокумент22 страницыPowerPoint Tutorial - PowerPoint Basicsdorje@blueyonder.co.ukОценок пока нет

- Taxotere NewДокумент3 страницыTaxotere NewamudaryoОценок пока нет

- Outlook Tutorial - Outlook BasicsДокумент20 страницOutlook Tutorial - Outlook Basicsc_clipperОценок пока нет

- The World Bank Group - Tajikistan Partnership Program SnapshotДокумент31 страницаThe World Bank Group - Tajikistan Partnership Program SnapshotamudaryoОценок пока нет

- Taxotere NewДокумент3 страницыTaxotere NewamudaryoОценок пока нет

- Baltagi Financial Development and Openness 2009Документ12 страницBaltagi Financial Development and Openness 2009amudaryoОценок пока нет

- R-Cheat SheetДокумент4 страницыR-Cheat SheetPrasad Marathe100% (1)

- Botakoz Kasumbekova Understanding Stalinism 2017Документ19 страницBotakoz Kasumbekova Understanding Stalinism 2017amudaryoОценок пока нет

- Foreign Aid to Tajikistan 2002-2012Документ2 страницыForeign Aid to Tajikistan 2002-2012amudaryoОценок пока нет

- Kiingdom of CaubulДокумент461 страницаKiingdom of CaubulamudaryoОценок пока нет

- ODI Budget Credibility 2014Документ38 страницODI Budget Credibility 2014amudaryoОценок пока нет

- So, What Did You Do Last Night? The Economics of Infidelity: KYKLOS, Vol. 61 - 2008 - No. 3, 391-410Документ20 страницSo, What Did You Do Last Night? The Economics of Infidelity: KYKLOS, Vol. 61 - 2008 - No. 3, 391-410amudaryoОценок пока нет

- Japan-IMF ScholarshipДокумент32 страницыJapan-IMF ScholarshipamudaryoОценок пока нет

- DAC List Used For 2012 and 2013 FlowsДокумент1 страницаDAC List Used For 2012 and 2013 FlowsamudaryoОценок пока нет

- Tax Burden in ChinaДокумент27 страницTax Burden in ChinaamudaryoОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

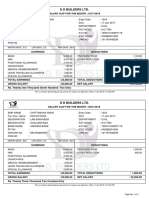

- Pay - Slip Oct. & Nov. 19Документ1 страницаPay - Slip Oct. & Nov. 19Atul Kumar MishraОценок пока нет

- KctochiДокумент5 страницKctochitradingpithistoryОценок пока нет

- Distress For Rent ActДокумент20 страницDistress For Rent Actjaffar s mОценок пока нет

- Original PDF Global Problems and The Culture of Capitalism Books A La Carte 7th EditionДокумент61 страницаOriginal PDF Global Problems and The Culture of Capitalism Books A La Carte 7th Editioncarla.campbell348100% (41)

- Crop Insurance - BrazilДокумент3 страницыCrop Insurance - Brazilanandekka84Оценок пока нет

- PPLCДокумент5 страницPPLCarjun SinghОценок пока нет

- The End of Japanese-Style ManagementДокумент24 страницыThe End of Japanese-Style ManagementThanh Tung NguyenОценок пока нет

- Indian Railways Project ReportДокумент27 страницIndian Railways Project Reportvabsy4533% (3)

- CV Medi Aprianda S, S.TДокумент2 страницыCV Medi Aprianda S, S.TMedi Aprianda SiregarОценок пока нет

- Disrupting MobilityДокумент346 страницDisrupting MobilityMickey100% (1)

- Ramos ReportДокумент9 страницRamos ReportOnaysha YuОценок пока нет

- Data 73Документ4 страницыData 73Abhijit BarmanОценок пока нет

- VAT Declaration FormДокумент2 страницыVAT Declaration FormWedaje Alemayehu67% (3)

- ACC 690 Final Project Guidelines and RubricДокумент4 страницыACC 690 Final Project Guidelines and RubricSalman KhalidОценок пока нет

- Infra Projects Total 148Документ564 страницыInfra Projects Total 148chintuuuОценок пока нет

- Service Operations As A Secret WeaponДокумент6 страницService Operations As A Secret Weaponclaudio alanizОценок пока нет

- Case Study 2 (Indigo) PDFДокумент3 страницыCase Study 2 (Indigo) PDFDebasish SahooОценок пока нет

- RD Sharma Cbse Class 11 Business Studies Sample Paper 2014 1Документ3 страницыRD Sharma Cbse Class 11 Business Studies Sample Paper 2014 1praveensharma61Оценок пока нет

- MEC 1st Year 2020-21 EnglishДокумент16 страницMEC 1st Year 2020-21 EnglishKumar UditОценок пока нет

- Bajaj Chetak PLCДокумент13 страницBajaj Chetak PLCVinay Tripathi0% (1)

- Russia and Lithuania Economic RelationsДокумент40 страницRussia and Lithuania Economic RelationsYi Zhu-tangОценок пока нет

- Blkpay YyyymmddДокумент4 страницыBlkpay YyyymmddRamesh PatelОценок пока нет

- Bitcoin Dicebot Script WorkingДокумент3 страницыBitcoin Dicebot Script WorkingMaruel MeyerОценок пока нет

- Difference Between EPF GPF & PPFДокумент3 страницыDifference Between EPF GPF & PPFSrikanth VsrОценок пока нет

- Smart Beta: A Follow-Up to Traditional Beta MeasuresДокумент15 страницSmart Beta: A Follow-Up to Traditional Beta Measuresdrussell524Оценок пока нет

- D) Indirect Taxes and SubsidiesДокумент7 страницD) Indirect Taxes and SubsidiesnatlyhОценок пока нет

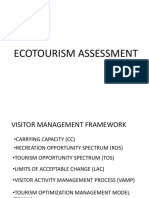

- Ecotourism Visitor Management Framework AssessmentДокумент15 страницEcotourism Visitor Management Framework AssessmentFranco JocsonОценок пока нет

- StopfordДокумент41 страницаStopfordFarid OmariОценок пока нет

- ACT EAST POLICY & ASEAN by Soumyabrata DharДокумент6 страницACT EAST POLICY & ASEAN by Soumyabrata DharSoumyabrata DharОценок пока нет

- Presented By:-: Sutripti DattaДокумент44 страницыPresented By:-: Sutripti DattaSutripti BardhanОценок пока нет