Вам также может понравиться

- 2008 Financial CrisisДокумент1 страница2008 Financial Crisisprabhat_j19Оценок пока нет

- 2008 Financial CrisisДокумент1 страница2008 Financial Crisisprabhat_j19Оценок пока нет

- 2008 Financial CrisisДокумент1 страница2008 Financial Crisisprabhat_j19Оценок пока нет

- Gen YДокумент12 страницGen Yprabhat_j19Оценок пока нет

- Gen YДокумент13 страницGen Yprabhat_j19Оценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5784)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- SyllabusДокумент5 страницSyllabusBalbeer SinghОценок пока нет

- 1 OM-IntroductionДокумент35 страниц1 OM-IntroductionA11Shridhar SuryawanshiОценок пока нет

- Cosst Accounting SourceДокумент134 страницыCosst Accounting SourceIsabel FlonascaОценок пока нет

- List of Process For BBP Preparation (PP, SD, MM and FI)Документ22 страницыList of Process For BBP Preparation (PP, SD, MM and FI)Debi GhoshОценок пока нет

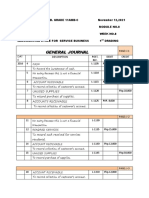

- Accounting Cycle for a Service BusinessДокумент5 страницAccounting Cycle for a Service BusinessKristel Mae PayotОценок пока нет

- Chapter-1-Regulatory FrameworkДокумент6 страницChapter-1-Regulatory FrameworkYean Soramy100% (1)

- Distribution in Rural Market.Документ4 страницыDistribution in Rural Market.Mitesh Kadakia100% (1)

- fileCHAPTER 1 Test QuestionsДокумент5 страницfileCHAPTER 1 Test QuestionsEsmeraldaОценок пока нет

- Engineering Economics (Model Paper)Документ4 страницыEngineering Economics (Model Paper)nitishgalaxyОценок пока нет

- Depriciation AccountingДокумент42 страницыDepriciation Accountingezek1elОценок пока нет

- Bản Sao Của DOWNYДокумент50 страницBản Sao Của DOWNYDuy AnhОценок пока нет

- MBA Case StudiesДокумент123 страницыMBA Case StudiesMariell Joy Cariño-TanОценок пока нет

- Reading 3 - Through What Channels Can You Get Teas Onto The European MarketДокумент9 страницReading 3 - Through What Channels Can You Get Teas Onto The European MarketTrần Lê Uyên ThiОценок пока нет

- TYBAF Project TopicsДокумент2 страницыTYBAF Project Topicsseema mundaleОценок пока нет

- 01 Conceptual Framework (Student)Документ23 страницы01 Conceptual Framework (Student)Christina DulayОценок пока нет

- Solutions To Chapter 2Документ9 страницSolutions To Chapter 2Alma Delos SantosОценок пока нет

- 1-The Nature and Importance of EntrepreneurshipДокумент10 страниц1-The Nature and Importance of EntrepreneurshipMuhammad AtharОценок пока нет

- Dawlance 1Документ11 страницDawlance 1SparksОценок пока нет

- Inventory Functions & ImportanceДокумент1 страницаInventory Functions & ImportanceRiad HossainОценок пока нет

- VOC To CTQ Conversion SampleДокумент5 страницVOC To CTQ Conversion SampleshivaprasadmvitОценок пока нет

- Key Point Slides - Ch9Документ10 страницKey Point Slides - Ch927Winanda Setyaning KridantikaОценок пока нет

- Class Guide - Sales Funnel Fundamentals PDFДокумент15 страницClass Guide - Sales Funnel Fundamentals PDFJayson Tabuen ChanchicoОценок пока нет

- Profile - Power Root MalaysiaДокумент2 страницыProfile - Power Root MalaysiaMuhamad SyafiqОценок пока нет

- Company Profil KAP Hendrawinata Eddy Sidharta & TanzilДокумент12 страницCompany Profil KAP Hendrawinata Eddy Sidharta & TanzilHusni YasinОценок пока нет

- Ingvysya 1Документ235 страницIngvysya 1Prathyusha KoguruОценок пока нет

- Ch08 PricingДокумент69 страницCh08 PricingDaniel KangОценок пока нет

- Overview of Ifrs Convergence Process in IndonesiaДокумент14 страницOverview of Ifrs Convergence Process in IndonesiaAngga PramadaОценок пока нет

- InfoQSample KanbanFromThe Inside Chapt4Документ41 страницаInfoQSample KanbanFromThe Inside Chapt4chansk4003Оценок пока нет

- Acctg201 Support Cost Department AllocationДокумент3 страницыAcctg201 Support Cost Department AllocationEab RondinaОценок пока нет

- REFERENCESДокумент2 страницыREFERENCESjessrylmae belza100% (1)