Вам также может понравиться

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- UNHCR - Concept Paper - PelayoДокумент6 страницUNHCR - Concept Paper - PelayoJrPelayoОценок пока нет

- Classify Property TypesДокумент66 страницClassify Property TypesJrPelayoОценок пока нет

- Contributing To Global Efforts: Canada's New Approach To Global Climate Action Is Built OnДокумент3 страницыContributing To Global Efforts: Canada's New Approach To Global Climate Action Is Built OnJrPelayoОценок пока нет

- Property Presentation NotesДокумент4 страницыProperty Presentation NotesJrPelayoОценок пока нет

- First Problem SpilДокумент1 страницаFirst Problem SpilJrPelayoОценок пока нет

- #50 Agyao vs. CSC - TingДокумент2 страницы#50 Agyao vs. CSC - TingJrPelayoОценок пока нет

- Respondents Argument: The Contract Agreement and The Loan AgreementДокумент5 страницRespondents Argument: The Contract Agreement and The Loan AgreementJrPelayoОценок пока нет

- CanadaДокумент1 страницаCanadaJrPelayoОценок пока нет

- Respondents Argument: The Contract Agreement and The Loan AgreementДокумент5 страницRespondents Argument: The Contract Agreement and The Loan AgreementJrPelayoОценок пока нет

- #3 Allado V Diokno - PelayoДокумент4 страницы#3 Allado V Diokno - PelayoJrPelayoОценок пока нет

- People Vs Escordial - Pelayo FactsДокумент3 страницыPeople Vs Escordial - Pelayo FactsJrPelayoОценок пока нет

- Goan V Yatco - LazatinДокумент2 страницыGoan V Yatco - LazatinAnonymous fnlSh4KHIgОценок пока нет

- First Problem SpilДокумент1 страницаFirst Problem SpilJrPelayoОценок пока нет

- International Court of Justice Barcelona TractionДокумент3 страницыInternational Court of Justice Barcelona TractionJrPelayoОценок пока нет

- #15 PEPSI-COLA V City of Butuan - PelayoДокумент2 страницы#15 PEPSI-COLA V City of Butuan - PelayoJrPelayoОценок пока нет

- For Other Uses, See - "Aves" and "Avifauna" Redirect Here. For Other Uses, See andДокумент8 страницFor Other Uses, See - "Aves" and "Avifauna" Redirect Here. For Other Uses, See andJrPelayoОценок пока нет

- Zhang JikeДокумент3 страницыZhang JikeJrPelayoОценок пока нет

- #5 Silkair v. Cir (2008) - PelayoДокумент2 страницы#5 Silkair v. Cir (2008) - PelayoJrPelayoОценок пока нет

- HammertimeДокумент3 страницыHammertimeJrPelayoОценок пока нет

- For Other Uses, See - "Aves" and "Avifauna" Redirect Here. For Other Uses, See andДокумент8 страницFor Other Uses, See - "Aves" and "Avifauna" Redirect Here. For Other Uses, See andJrPelayoОценок пока нет

- StarfishДокумент3 страницыStarfishJrPelayoОценок пока нет

- Cutthroat: Murderers and MoreДокумент3 страницыCutthroat: Murderers and MoreJrPelayoОценок пока нет

- CitrusДокумент5 страницCitrusJrPelayoОценок пока нет

- LagerДокумент2 страницыLagerJrPelayoОценок пока нет

- Sales Codal (Nov. 7)Документ6 страницSales Codal (Nov. 7)JrPelayoОценок пока нет

- WreckДокумент2 страницыWreckJrPelayoОценок пока нет

- Firecracker: For Other Uses, SeeДокумент4 страницыFirecracker: For Other Uses, SeeJrPelayoОценок пока нет

- TanyaДокумент1 страницаTanyaJrPelayoОценок пока нет

- Spell and define the word "justДокумент1 страницаSpell and define the word "justJrPelayoОценок пока нет

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

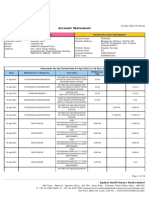

- Account Statement: Customer Information Branch/Account InformationДокумент12 страницAccount Statement: Customer Information Branch/Account InformationRohit kumarОценок пока нет

- RTB Taxation II Course Outline 2016-2017Документ21 страницаRTB Taxation II Course Outline 2016-2017Victor LimОценок пока нет

- Social ScienceДокумент5 страницSocial Sciencejudith DiazОценок пока нет

- Reception For Ted CruzДокумент2 страницыReception For Ted CruzSunlight FoundationОценок пока нет

- Scientific Drilling International Scientific Drilling International 03.345.208.7-411.000 Taman Tekno BSD Sektor Xi K.2/12 Setu - Tangerang SeДокумент1 страницаScientific Drilling International Scientific Drilling International 03.345.208.7-411.000 Taman Tekno BSD Sektor Xi K.2/12 Setu - Tangerang SePinggir KaliОценок пока нет

- Tax Invoice: Gstin PAN Drug Licence NoДокумент1 страницаTax Invoice: Gstin PAN Drug Licence Nochunawalahanif997Оценок пока нет

- Tax Planning With Regard To Capital GainsДокумент25 страницTax Planning With Regard To Capital GainsKamraan QuadriОценок пока нет

- DR 15 NДокумент8 страницDR 15 Napi-114866560Оценок пока нет

- TAX FILING DEADLINEДокумент11 страницTAX FILING DEADLINENg GraceОценок пока нет

- Collector of Int Revenue vs. University of The Visayas, 1 SCRA 669, Feb 28, 1961Документ9 страницCollector of Int Revenue vs. University of The Visayas, 1 SCRA 669, Feb 28, 1961BrunxAlabastroОценок пока нет

- ACCДокумент16 страницACCFarah AlyaОценок пока нет

- Utility Bill Payment ReminderДокумент2 страницыUtility Bill Payment ReminderJhoan VelasquezОценок пока нет

- Journal Entry.Документ45 страницJournal Entry.CHARAK RAYОценок пока нет

- Plate No: B241AX: Official ReceiptДокумент1 страницаPlate No: B241AX: Official ReceiptUminga, Kristine C.Оценок пока нет

- 2021 Turbo Tax ReturnДокумент10 страниц2021 Turbo Tax ReturnIvette Hoffman75% (4)

- Ola Share 1016517059Документ3 страницыOla Share 1016517059jayasundarОценок пока нет

- Enroll Now: Undergraduate Enrollment Steps and Schedule AY 2020-21 Term 2Документ9 страницEnroll Now: Undergraduate Enrollment Steps and Schedule AY 2020-21 Term 2john doeОценок пока нет

- Form 12B - Previous Employment Income DetailsДокумент2 страницыForm 12B - Previous Employment Income DetailsSachin5586Оценок пока нет

- Accrued Expenses ExplainedДокумент14 страницAccrued Expenses ExplainedDebbie Grace Latiban LinazaОценок пока нет

- Offer Letter Sales RepresentativeДокумент5 страницOffer Letter Sales RepresentativeIqbal SkОценок пока нет

- Questionaire On e Payment SystemsДокумент8 страницQuestionaire On e Payment SystemsAyush VermaОценок пока нет

- Return On Invested Capital: Disaggregation of Profit MarginДокумент8 страницReturn On Invested Capital: Disaggregation of Profit MarginmohihsanОценок пока нет

- Acct Statement - XX4542 - 11012023Документ3 страницыAcct Statement - XX4542 - 11012023Prachi JoshiОценок пока нет

- Pakistan Custom Department MCQs For Appraising - Valuation Officer in BoRДокумент5 страницPakistan Custom Department MCQs For Appraising - Valuation Officer in BoRShoaib AhmedОценок пока нет

- TDS Rate With Section FY 2019-2020Документ22 страницыTDS Rate With Section FY 2019-2020Iftekhar SaikatОценок пока нет

- Tax Invoice Dwaraka N: Billing Period Invoice Date Amount Payable Due Date Amount After Due DateДокумент2 страницыTax Invoice Dwaraka N: Billing Period Invoice Date Amount Payable Due Date Amount After Due DateDwaraka PillaiОценок пока нет

- Axis Bank Ace Credit Card TncsДокумент4 страницыAxis Bank Ace Credit Card TncsAjinkya JadhavОценок пока нет

- Bills of ExchangeДокумент13 страницBills of Exchangesrushti mahaleОценок пока нет

- FRM Epay Echallan PrintДокумент1 страницаFRM Epay Echallan PrintSanket PatelОценок пока нет