Вам также может понравиться

- Types of Stamps and Some Concepts of Stamp DutyДокумент5 страницTypes of Stamps and Some Concepts of Stamp DutyNikhil Kasat100% (3)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Income Declaration Scheme Rules, 2016: Form 1Документ9 страницIncome Declaration Scheme Rules, 2016: Form 1Nikhil KasatОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- CA Result AnalysisДокумент1 страницаCA Result AnalysisNikhil KasatОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Black Money BillДокумент30 страницBlack Money BillNikhil KasatОценок пока нет

- Hedging With Financial DerivativesДокумент30 страницHedging With Financial DerivativesNikhil KasatОценок пока нет

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Some Confusing & Debatable CSR Issues: Learning Series Vol.-I Issue - 2 2015-16Документ21 страницаSome Confusing & Debatable CSR Issues: Learning Series Vol.-I Issue - 2 2015-16Nikhil KasatОценок пока нет

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- August Month CompliancesДокумент1 страницаAugust Month CompliancesNikhil KasatОценок пока нет

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

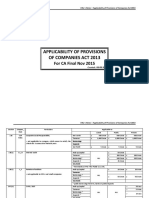

- ApplicabiliTY of ProvisionsДокумент3 страницыApplicabiliTY of ProvisionsNikhil KasatОценок пока нет

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Fees Calculation For Increase in Authorised Share Capital Form SH 7, Only For GujaratДокумент10 страницFees Calculation For Increase in Authorised Share Capital Form SH 7, Only For GujaratNikhil KasatОценок пока нет

- CA Final Writing Professional Ethics AnswersДокумент2 страницыCA Final Writing Professional Ethics AnswersNikhil KasatОценок пока нет

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Agricultural Income: Agricultural Income: - As Per Sec 10 (1) Agricultural Income Earned by TheДокумент9 страницAgricultural Income: Agricultural Income: - As Per Sec 10 (1) Agricultural Income Earned by TheNikhil KasatОценок пока нет

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Curriculum VitaeДокумент13 страницCurriculum VitaeNikhil KasatОценок пока нет

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Privileges To Small CompaniesДокумент2 страницыPrivileges To Small CompaniesNikhil KasatОценок пока нет

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Cusoms Valuation MaterialДокумент8 страницCusoms Valuation MaterialNikhil KasatОценок пока нет

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- Defamation Under Common LawДокумент6 страницDefamation Under Common LawNikhil KasatОценок пока нет

- SN Vertical Due Dates Particular Consequence of Non ComplianceДокумент1 страницаSN Vertical Due Dates Particular Consequence of Non ComplianceNikhil KasatОценок пока нет

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- MoU UH TemplateДокумент3 страницыMoU UH TemplateMorgan Ashley100% (1)

- Cefppc NoteДокумент8 страницCefppc NoteMinhaj AlamОценок пока нет

- 2013 Paper F1 QandA Sample Download v1Документ34 страницы2013 Paper F1 QandA Sample Download v1Georges NdumbeОценок пока нет

- BAF/1/20/011/TZ: The State University of ZanzibarДокумент12 страницBAF/1/20/011/TZ: The State University of Zanzibartembo groupОценок пока нет

- Regulatory Framework For Business TransactionsДокумент36 страницRegulatory Framework For Business TransactionsKriztleKateMontealtoGelogo100% (7)

- Course Syllabus in Accounting For Refresher 2Документ8 страницCourse Syllabus in Accounting For Refresher 2Sharon AnchetaОценок пока нет

- KYC Documents For EntitiesДокумент2 страницыKYC Documents For EntitiesParikshit YadavОценок пока нет

- Republic Act 8424 The Tax Reform Act of 1997 TAX ON INDIVIDUALS SEC. 24. Income Tax Rates.Документ23 страницыRepublic Act 8424 The Tax Reform Act of 1997 TAX ON INDIVIDUALS SEC. 24. Income Tax Rates.Dominic EmbodoОценок пока нет

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Corpo Notes PJAДокумент249 страницCorpo Notes PJAKeziah Eden TuazonОценок пока нет

- Indian Partnership Act, 1932Документ12 страницIndian Partnership Act, 1932Bharath.S 16-17-G8Оценок пока нет

- National Open University of Nigeria: BUS 105 Element To Management 1Документ124 страницыNational Open University of Nigeria: BUS 105 Element To Management 1The SubОценок пока нет

- TGI Good PlanningДокумент5 страницTGI Good Planningasdf789456123Оценок пока нет

- Chapter 1 OperationsДокумент9 страницChapter 1 Operationsrietzhel22100% (1)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Soichi vs. GozonДокумент15 страницSoichi vs. GozonKenn SeunghoОценок пока нет

- 399 538Документ140 страниц399 538abhi701Оценок пока нет

- P69 - Ros & Aguete V PNB LaoagДокумент4 страницыP69 - Ros & Aguete V PNB LaoagDomski Fatima CandolitaОценок пока нет

- Presidential Decree No. 902-A: March 11, 1976Документ7 страницPresidential Decree No. 902-A: March 11, 1976Christine Gel MadrilejoОценок пока нет

- CH 2 AssignmentДокумент1 страницаCH 2 AssignmentSachpreet KaurОценок пока нет

- Relative Resource ManagerДокумент38 страницRelative Resource ManagerDulana Jayaratne0% (1)

- Philippine Law School Commercial Law Review Class Professor: Judge Silvino T. Pampilo Jr. Submitted By: Pat P. MonteДокумент3 страницыPhilippine Law School Commercial Law Review Class Professor: Judge Silvino T. Pampilo Jr. Submitted By: Pat P. MontepogsОценок пока нет

- SCC VA Biz GuideДокумент82 страницыSCC VA Biz Guidenestor3101Оценок пока нет

- Project Veritas Tax Exemption ApplicationДокумент22 страницыProject Veritas Tax Exemption ApplicationLachlan MarkayОценок пока нет

- Partnership Dissolution AgreementДокумент2 страницыPartnership Dissolution AgreementLegal Forms89% (19)

- 10 Scra CasesДокумент2 страницы10 Scra CaseskennerОценок пока нет

- CLG Past YearДокумент4 страницыCLG Past YearBeeJu LyeОценок пока нет

- DAC 6 PresentationДокумент56 страницDAC 6 Presentationbacha436Оценок пока нет

- Note 1 Joint AccountsДокумент3 страницыNote 1 Joint AccountsJudith AlisuagОценок пока нет

- Test Bank For Taxation For Decision Makers, 2016 Edition by Shirley Dennis Escoffier, Karen Fortin 9781119089087Документ29 страницTest Bank For Taxation For Decision Makers, 2016 Edition by Shirley Dennis Escoffier, Karen Fortin 9781119089087NitinОценок пока нет

- Atty. Gaviola Corpo Midterms Notes 501Документ89 страницAtty. Gaviola Corpo Midterms Notes 501KaiserОценок пока нет

- Law On Business Organizations 2021Документ58 страницLaw On Business Organizations 2021BJ SoilОценок пока нет