Вам также может понравиться

- Controlling Payroll Cost - Critical Disciplines for Club ProfitabilityОт EverandControlling Payroll Cost - Critical Disciplines for Club ProfitabilityОценок пока нет

- HomeWork MCS-Nurul Sari (1101002048) - Case 5.1 5.4Документ5 страницHomeWork MCS-Nurul Sari (1101002048) - Case 5.1 5.4Nurul SariОценок пока нет

- Galvor CompanyДокумент27 страницGalvor CompanyAbbasgodhrawalaОценок пока нет

- Chap009 131230191204 Phpapp01Документ41 страницаChap009 131230191204 Phpapp01AndrianMelmamBesyОценок пока нет

- Rendell CompanyДокумент3 страницыRendell CompanyTung Nguyen KhacОценок пока нет

- New Jersey Insurance CompanyДокумент13 страницNew Jersey Insurance CompanyParth V. PurohitОценок пока нет

- Jawaban GSLC 1Документ2 страницыJawaban GSLC 1Soniea DianiОценок пока нет

- New Jersey Insurance CompanyДокумент4 страницыNew Jersey Insurance CompanyParth V. PurohitОценок пока нет

- Materi Persentasi SIA (Semester 4)Документ3 страницыMateri Persentasi SIA (Semester 4)Rahmad Bari BarrudiОценок пока нет

- Texas Instruments and Hewlett-PackardДокумент20 страницTexas Instruments and Hewlett-PackardNaveen SinghОценок пока нет

- Case 4.4Документ4 страницыCase 4.4syafiraОценок пока нет

- Case 1A Behavioral AccountingДокумент16 страницCase 1A Behavioral Accountingrenna_magdalenaОценок пока нет

- Management Control System - Revenue & Expense CenterДокумент23 страницыManagement Control System - Revenue & Expense CenterCitra Dewi Wulansari0% (1)

- 13 1Документ5 страниц13 1AdinIhtisyamuddin100% (1)

- Enterprice Performance Management Case Study On: Wal-Mart Stores, IncДокумент3 страницыEnterprice Performance Management Case Study On: Wal-Mart Stores, IncChaitanya ZirkandeОценок пока нет

- Bsz263432882inh PDFДокумент4 страницыBsz263432882inh PDFMarsiniОценок пока нет

- Presented By: Ishan Aggarwal Manju Chandel Rajat SinglaДокумент26 страницPresented By: Ishan Aggarwal Manju Chandel Rajat Singlarajat_singla100% (3)

- Grand Jean CompanyДокумент6 страницGrand Jean CompanyAdi AdiadiОценок пока нет

- 3-3 Rendell Company Study CaseДокумент12 страниц3-3 Rendell Company Study CaseAdinIhtisyamuddinОценок пока нет

- Case - Ohio Rubber Works Inc PDFДокумент3 страницыCase - Ohio Rubber Works Inc PDFRaviSinghОценок пока нет

- ACCT 460: Principles of Auditing Assignment 1, Version CДокумент4 страницыACCT 460: Principles of Auditing Assignment 1, Version CNurul SyakirinОценок пока нет

- KASUS CUP CorporationДокумент7 страницKASUS CUP CorporationNia Azura SariОценок пока нет

- Contoh Eliminasi Lap - Keu KonsolidasiДокумент44 страницыContoh Eliminasi Lap - Keu KonsolidasiLuki DewayaniОценок пока нет

- Answers Chapter 4Документ4 страницыAnswers Chapter 4Maricel Inoc FallerОценок пока нет

- AKMY 6e ch01 - SMДокумент20 страницAKMY 6e ch01 - SMMuhammad Ahad Habib Ellahi100% (2)

- CVP AnalysisДокумент5 страницCVP AnalysisAnne BacolodОценок пока нет

- Fundamentals of Cost Management: True / False QuestionsДокумент238 страницFundamentals of Cost Management: True / False QuestionsElaine GimarinoОценок пока нет

- A. Laboratory Manager : : Exercise 1-11 The Managerial ProcessДокумент2 страницыA. Laboratory Manager : : Exercise 1-11 The Managerial ProcessNero VedsuОценок пока нет

- Section - 5 Case-5.3Документ7 страницSection - 5 Case-5.3syafiraОценок пока нет

- Kode QДокумент11 страницKode QatikaОценок пока нет

- Waysideinnsincgroupm 110520054120 Phpapp02Документ7 страницWaysideinnsincgroupm 110520054120 Phpapp02raghunomix123Оценок пока нет

- Problem (Objective 20-5) Alyssa Ghose Is Auditing Payroll Accruals For A Manufacturing Company. The ClientДокумент2 страницыProblem (Objective 20-5) Alyssa Ghose Is Auditing Payroll Accruals For A Manufacturing Company. The ClientNana BananaОценок пока нет

- Jane Belinda Saranga - CASE 1-3 Xerox CorporationДокумент2 страницыJane Belinda Saranga - CASE 1-3 Xerox CorporationJane Belinda SarangaОценок пока нет

- Partnership Liquidation: Answers To Questions 1Документ28 страницPartnership Liquidation: Answers To Questions 1El Carl Sontellinosa0% (1)

- Jawaban Grand JeanДокумент7 страницJawaban Grand JeanSariIsmanengsihОценок пока нет

- Question and Answer - 60Документ31 страницаQuestion and Answer - 60acc-expertОценок пока нет

- Solution Manual Cornerstones of ManageriДокумент12 страницSolution Manual Cornerstones of ManageriZeenaОценок пока нет

- Universiti Utara Malaysia Othman Yeop Abdullah Graduate School of Business (Oyagsb) A201 2020/2021Документ2 страницыUniversiti Utara Malaysia Othman Yeop Abdullah Graduate School of Business (Oyagsb) A201 2020/2021fitriОценок пока нет

- Chapter 1-7 - Tugas Kelompok Kelas BДокумент3 страницыChapter 1-7 - Tugas Kelompok Kelas BJana WrightОценок пока нет

- Trasfer Pricing ExampleДокумент4 страницыTrasfer Pricing ExampleHashmi Sutariya100% (1)

- Texas Instrument and Hewlett-PackardДокумент3 страницыTexas Instrument and Hewlett-PackardMuhammad KamilОценок пока нет

- Expenditure Cycle Case - GARCIAДокумент2 страницыExpenditure Cycle Case - GARCIAARLENE GARCIAОценок пока нет

- ACG4803 - Chapter 5Документ108 страницACG4803 - Chapter 5Minh Nguyễn100% (2)

- Hilton Chapter 13 SolutionsДокумент71 страницаHilton Chapter 13 SolutionsSharkManLazersОценок пока нет

- ADM 4340M Winter 2015 Suggested Solution To Deferred Mid Term ExamДокумент28 страницADM 4340M Winter 2015 Suggested Solution To Deferred Mid Term ExamSKОценок пока нет

- Chapter 01 - Business CombinationsДокумент17 страницChapter 01 - Business CombinationsTina LundstromОценок пока нет

- Case Analysis of Abrams CompanyДокумент4 страницыCase Analysis of Abrams CompanyMilanPadariyaОценок пока нет

- Case 5-4 Abrams Company: 1.the ROI Behavior 2.transfer Pricing Disputes 3.operational Trouble ShoutingДокумент9 страницCase 5-4 Abrams Company: 1.the ROI Behavior 2.transfer Pricing Disputes 3.operational Trouble ShoutingBarudak BageurОценок пока нет

- Abrams Company Case SolutionДокумент4 страницыAbrams Company Case Solutionhssh8Оценок пока нет

- Abrams Company (Case 5-4)Документ12 страницAbrams Company (Case 5-4)Mhd HeickalОценок пока нет

- Case 5-4. Abrams Company Case OverviewДокумент3 страницыCase 5-4. Abrams Company Case OverviewMuhammad KamilОценок пока нет

- 10 Chapter 10Документ21 страница10 Chapter 10Ruben SucionoОценок пока нет

- Adams CorporationДокумент2 страницыAdams Corporationrocamorro67% (6)

- What The Concept of Free Cash Flow?Документ36 страницWhat The Concept of Free Cash Flow?Sanket DangiОценок пока нет

- Emerson Electric - Week 3Документ3 страницыEmerson Electric - Week 3Sandro McTavishОценок пока нет

- Jariatu MGMT AssignДокумент10 страницJariatu MGMT AssignHenry Bobson SesayОценок пока нет

- Valuations 1Документ26 страницValuations 1nsnhemachenaОценок пока нет

- ACCT 504 MART Perfect EducationДокумент69 страницACCT 504 MART Perfect Educationdavidwarn1223Оценок пока нет

- CH 8Документ2 страницыCH 8Abbas Ali100% (6)

- PM Theory Notes by @BeingACCAДокумент18 страницPM Theory Notes by @BeingACCAmonjurhossain.accaОценок пока нет

- Reta Sharfina Tahar 1111002006 Case 10-1 Variance Analysis ProblemsДокумент2 страницыReta Sharfina Tahar 1111002006 Case 10-1 Variance Analysis ProblemsTiffany SmithОценок пока нет

- Summary of Starbucks' Management: Change and Innovation at StarbucksДокумент3 страницыSummary of Starbucks' Management: Change and Innovation at StarbucksTiffany SmithОценок пока нет

- Inventory AuditДокумент26 страницInventory AuditTiffany SmithОценок пока нет

- Syllabus: Course DescriptionДокумент7 страницSyllabus: Course DescriptionTiffany SmithОценок пока нет

- Teori AkuntansiДокумент6 страницTeori AkuntansiTiffany SmithОценок пока нет

- Expenditure Multipliers: The Keynesian Model : Key ConceptsДокумент15 страницExpenditure Multipliers: The Keynesian Model : Key ConceptsTiffany SmithОценок пока нет

- Ob C2A006136 PDFДокумент33 страницыOb C2A006136 PDFTiffany SmithОценок пока нет

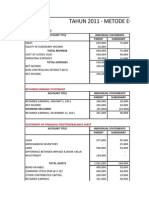

- Tahun 2011 - Metode Equity: Income StementДокумент8 страницTahun 2011 - Metode Equity: Income StementTiffany SmithОценок пока нет

- SBI Project ReportДокумент14 страницSBI Project ReportNick IvanОценок пока нет

- Maheshwari, S.N. Financial Management, Sultan & Sons Publications, New Delhi, 2006Документ6 страницMaheshwari, S.N. Financial Management, Sultan & Sons Publications, New Delhi, 2006tonyОценок пока нет

- Hilton Balanced Score Card2Документ3 страницыHilton Balanced Score Card2Yogesh PatelОценок пока нет

- Project Report On Gems and Jewelry IndustryДокумент61 страницаProject Report On Gems and Jewelry IndustryAmy Sharma53% (15)

- Important Banking TermsДокумент4 страницыImportant Banking TermsmedeepikaОценок пока нет

- Rise and Fall of Global Trust BankДокумент3 страницыRise and Fall of Global Trust BankmohitОценок пока нет

- Alligation RulesДокумент2 страницыAlligation RulesMd IntshamuddinОценок пока нет

- MRC Setup and Usage PDFДокумент73 страницыMRC Setup and Usage PDFarajesh07Оценок пока нет

- Advantages and Disadvantages MortgageДокумент6 страницAdvantages and Disadvantages MortgageNurAmyliyanaОценок пока нет

- EXIM BankДокумент79 страницEXIM BankMishkaCDedhia0% (2)

- Credit Risk Management. KsfeДокумент71 страницаCredit Risk Management. KsfeJith EG86% (7)

- Form S11 For Subscribers Having A Tier I Account Without A PRAN Card - SG T II A PDFДокумент5 страницForm S11 For Subscribers Having A Tier I Account Without A PRAN Card - SG T II A PDFSudhir ShastriОценок пока нет

- BPI v. IAC & ZshornackДокумент1 страницаBPI v. IAC & ZshornackRon DecinОценок пока нет

- Working Capital Study at SuzlonДокумент52 страницыWorking Capital Study at SuzlonJauhar Raza100% (4)

- De Grauwe Keynes' Saving ParadoxДокумент20 страницDe Grauwe Keynes' Saving ParadoxecrcauОценок пока нет

- Modeling and Agency ContractДокумент3 страницыModeling and Agency ContractMysweethearts40% (5)

- HUL SuccessДокумент2 страницыHUL SuccessUjjval YadavОценок пока нет

- MBA Project Report On Financial AnalysisДокумент73 страницыMBA Project Report On Financial AnalysisShainaDhiman79% (24)

- Financial Inclusion and Information TechnologyДокумент8 страницFinancial Inclusion and Information TechnologydhawanmayurОценок пока нет

- Resume Template 2: Rofessional XperienceДокумент2 страницыResume Template 2: Rofessional XperienceVivek SinghОценок пока нет

- Business Plan NanostarДокумент38 страницBusiness Plan Nanostardhruvgupta1990Оценок пока нет

- AFAB Depreciation Run ExecutionДокумент18 страницAFAB Depreciation Run ExecutionraghuОценок пока нет

- Business Finance PDFДокумент372 страницыBusiness Finance PDFNguyen Binh Minh100% (1)

- Forward MarketДокумент18 страницForward MarketsachinremaОценок пока нет

- A Comparative Analysis of Life InsuranceДокумент41 страницаA Comparative Analysis of Life InsuranceDibyaRanjanBeheraОценок пока нет

- Met Smart GoldДокумент10 страницMet Smart GoldyatinthoratscrbОценок пока нет

- Acroynms Capital MarketsДокумент37 страницAcroynms Capital MarketsAnuj Sharma100% (1)

- Nishat Mills (Afm Report)Документ23 страницыNishat Mills (Afm Report)kk5522100% (1)

- Additional Case-Lets For Practice-April 17-RaoДокумент13 страницAdditional Case-Lets For Practice-April 17-RaoSankalp BhagatОценок пока нет

- Semi Auto TradingДокумент3 страницыSemi Auto TradingkonosubaОценок пока нет

- The Coaching Habit: Say Less, Ask More & Change the Way You Lead ForeverОт EverandThe Coaching Habit: Say Less, Ask More & Change the Way You Lead ForeverРейтинг: 4.5 из 5 звезд4.5/5 (186)

- Transformed: Moving to the Product Operating ModelОт EverandTransformed: Moving to the Product Operating ModelРейтинг: 4.5 из 5 звезд4.5/5 (2)

- The First Minute: How to start conversations that get resultsОт EverandThe First Minute: How to start conversations that get resultsРейтинг: 4.5 из 5 звезд4.5/5 (57)

- Unlocking Potential: 7 Coaching Skills That Transform Individuals, Teams, & OrganizationsОт EverandUnlocking Potential: 7 Coaching Skills That Transform Individuals, Teams, & OrganizationsРейтинг: 4.5 из 5 звезд4.5/5 (28)

- How to Lead: Wisdom from the World's Greatest CEOs, Founders, and Game ChangersОт EverandHow to Lead: Wisdom from the World's Greatest CEOs, Founders, and Game ChangersРейтинг: 4.5 из 5 звезд4.5/5 (95)

- High Road Leadership: Bringing People Together in a World That DividesОт EverandHigh Road Leadership: Bringing People Together in a World That DividesОценок пока нет

- How to Talk to Anyone at Work: 72 Little Tricks for Big Success Communicating on the JobОт EverandHow to Talk to Anyone at Work: 72 Little Tricks for Big Success Communicating on the JobРейтинг: 4.5 из 5 звезд4.5/5 (37)

- Billion Dollar Lessons: What You Can Learn from the Most Inexcusable Business Failures of the Last Twenty-five YearsОт EverandBillion Dollar Lessons: What You Can Learn from the Most Inexcusable Business Failures of the Last Twenty-five YearsРейтинг: 4.5 из 5 звезд4.5/5 (52)

- Good to Great by Jim Collins - Book Summary: Why Some Companies Make the Leap...And Others Don'tОт EverandGood to Great by Jim Collins - Book Summary: Why Some Companies Make the Leap...And Others Don'tРейтинг: 4.5 из 5 звезд4.5/5 (63)

- Leadership Skills that Inspire Incredible ResultsОт EverandLeadership Skills that Inspire Incredible ResultsРейтинг: 4.5 из 5 звезд4.5/5 (11)

- Scaling Up: How a Few Companies Make It...and Why the Rest Don't, Rockefeller Habits 2.0От EverandScaling Up: How a Few Companies Make It...and Why the Rest Don't, Rockefeller Habits 2.0Рейтинг: 5 из 5 звезд5/5 (2)

- Spark: How to Lead Yourself and Others to Greater SuccessОт EverandSpark: How to Lead Yourself and Others to Greater SuccessРейтинг: 4.5 из 5 звезд4.5/5 (132)

- The Power of People Skills: How to Eliminate 90% of Your HR Problems and Dramatically Increase Team and Company Morale and PerformanceОт EverandThe Power of People Skills: How to Eliminate 90% of Your HR Problems and Dramatically Increase Team and Company Morale and PerformanceРейтинг: 5 из 5 звезд5/5 (22)

- The 7 Habits of Highly Effective People: 30th Anniversary EditionОт EverandThe 7 Habits of Highly Effective People: 30th Anniversary EditionРейтинг: 5 из 5 звезд5/5 (337)

- The Introverted Leader: Building on Your Quiet StrengthОт EverandThe Introverted Leader: Building on Your Quiet StrengthРейтинг: 4.5 из 5 звезд4.5/5 (35)

- 7 Principles of Transformational Leadership: Create a Mindset of Passion, Innovation, and GrowthОт Everand7 Principles of Transformational Leadership: Create a Mindset of Passion, Innovation, and GrowthРейтинг: 5 из 5 звезд5/5 (52)

- The Friction Project: How Smart Leaders Make the Right Things Easier and the Wrong Things HarderОт EverandThe Friction Project: How Smart Leaders Make the Right Things Easier and the Wrong Things HarderОценок пока нет

- Superminds: The Surprising Power of People and Computers Thinking TogetherОт EverandSuperminds: The Surprising Power of People and Computers Thinking TogetherРейтинг: 3.5 из 5 звезд3.5/5 (7)

- 300+ PMP Practice Questions Aligned with PMBOK 7, Agile Methods, and Key Process Groups - 2024: First EditionОт Everand300+ PMP Practice Questions Aligned with PMBOK 7, Agile Methods, and Key Process Groups - 2024: First EditionРейтинг: 5 из 5 звезд5/5 (1)

- The Manager's Path: A Guide for Tech Leaders Navigating Growth and ChangeОт EverandThe Manager's Path: A Guide for Tech Leaders Navigating Growth and ChangeРейтинг: 4.5 из 5 звезд4.5/5 (99)

- Think Like Amazon: 50 1/2 Ideas to Become a Digital LeaderОт EverandThink Like Amazon: 50 1/2 Ideas to Become a Digital LeaderРейтинг: 4.5 из 5 звезд4.5/5 (60)

- Only the Paranoid Survive: How to Exploit the Crisis Points That Challenge Every CompanyОт EverandOnly the Paranoid Survive: How to Exploit the Crisis Points That Challenge Every CompanyРейтинг: 3.5 из 5 звезд3.5/5 (123)

- Summary: Choose Your Enemies Wisely: Business Planning for the Audacious Few: Key Takeaways, Summary and AnalysisОт EverandSummary: Choose Your Enemies Wisely: Business Planning for the Audacious Few: Key Takeaways, Summary and AnalysisРейтинг: 4.5 из 5 звезд4.5/5 (3)

- Management Mess to Leadership Success: 30 Challenges to Become the Leader You Would FollowОт EverandManagement Mess to Leadership Success: 30 Challenges to Become the Leader You Would FollowРейтинг: 4.5 из 5 звезд4.5/5 (27)