Вам также может понравиться

- Sales Tax Case Email # 259-2019 STA NO.866 LB 2019Документ5 страницSales Tax Case Email # 259-2019 STA NO.866 LB 2019Farhan JanОценок пока нет

- Sales Tax Case Email # 242-2019 STA NO.768 LB 2018Документ3 страницыSales Tax Case Email # 242-2019 STA NO.768 LB 2018Farhan JanОценок пока нет

- Sales Tax Case Email # 253-2019 STA NO.557 LB 2019Документ2 страницыSales Tax Case Email # 253-2019 STA NO.557 LB 2019Farhan JanОценок пока нет

- 2008SRO549Документ5 страниц2008SRO549Aakash RoyОценок пока нет

- Grounds For Return of PlaintДокумент11 страницGrounds For Return of PlaintFarhan Jan50% (2)

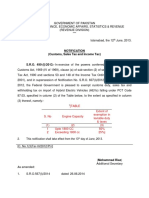

- Notification (Customs, Sales Tax and Income Tax)Документ1 страницаNotification (Customs, Sales Tax and Income Tax)Farhan JanОценок пока нет

- 6 Computerized SystemДокумент4 страницы6 Computerized SystemImran MemonОценок пока нет

- Sales Tax 2014-15 - Eight ScheduleДокумент8 страницSales Tax 2014-15 - Eight ScheduleAdnan AnjumОценок пока нет

- Begum Nusrat BhuttoДокумент4 страницыBegum Nusrat BhuttoFarhan JanОценок пока нет

- 5 Specific ProvisionsДокумент11 страниц5 Specific ProvisionsImran MemonОценок пока нет

- Sales Tax Notification Act 2012Документ2 страницыSales Tax Notification Act 2012Farhan JanОценок пока нет

- Tool Kit Salary 2015Документ11 страницTool Kit Salary 2015Farhan JanОценок пока нет

- Examples Salary 2015Документ44 страницыExamples Salary 2015Farhan JanОценок пока нет

- Abc Manufacturers Debit Note: Revised PriceДокумент2 страницыAbc Manufacturers Debit Note: Revised PriceFarhan JanОценок пока нет

- Sro 213Документ1 страницаSro 213Farhan JanОценок пока нет

- Sro 1076 of 2015Документ5 страницSro 1076 of 2015Farhan JanОценок пока нет

- Welcome To The Participants of The: Softax (Private) LimitedДокумент84 страницыWelcome To The Participants of The: Softax (Private) LimitedFarhan JanОценок пока нет

- Fate Outreach 17oct2011 (Islamabad)Документ8 страницFate Outreach 17oct2011 (Islamabad)Farhan JanОценок пока нет

- EOBI FS Operational Manual For EmployersДокумент128 страницEOBI FS Operational Manual For EmployersFarhan JanОценок пока нет

- Prospectus - CIMTДокумент9 страницProspectus - CIMTFarhan JanОценок пока нет

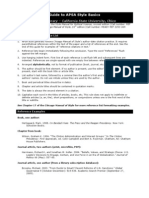

- APSA Citation GuideДокумент2 страницыAPSA Citation GuideDanie Lee 이강대Оценок пока нет

- Very Important Principles of LawДокумент7 страницVery Important Principles of LawFarhan JanОценок пока нет

- 10DS LL.B PII s2014Документ1 страница10DS LL.B PII s2014Farhan JanОценок пока нет

- ArrestДокумент2 страницыArrestFarhan JanОценок пока нет

- Cost Accounting Manual (2nd Edition)Документ177 страницCost Accounting Manual (2nd Edition)Bilal Farooq100% (1)

- Ashiana Iqbal Lahore PLDC Flat Application Form PDFДокумент2 страницыAshiana Iqbal Lahore PLDC Flat Application Form PDFUsman AhmadОценок пока нет

- What Is Forgery: Foe Example: B, Picks Up A Cheque On A Banker Signed by D, Payable To Bearer, But Without Any Sum HavingДокумент1 страницаWhat Is Forgery: Foe Example: B, Picks Up A Cheque On A Banker Signed by D, Payable To Bearer, But Without Any Sum HavingFarhan JanОценок пока нет

- Court Certificate LahoreДокумент1 страницаCourt Certificate LahoreFurqan AnwarОценок пока нет

- Circumtances of Dishonor or Bogus Cheques ProsecutionsДокумент2 страницыCircumtances of Dishonor or Bogus Cheques ProsecutionsFarhan JanОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Whitepaper ITES Industry PotentialДокумент6 страницWhitepaper ITES Industry PotentialsamuraiharryОценок пока нет

- Microbial Diseases of The Different Organ System and Epidem.Документ36 страницMicrobial Diseases of The Different Organ System and Epidem.Ysabelle GutierrezОценок пока нет

- Laporan Keuangan TRIN Per Juni 2023-FinalДокумент123 страницыLaporan Keuangan TRIN Per Juni 2023-FinalAdit RamdhaniОценок пока нет

- Material Safety Data Sheet: - AdsealДокумент12 страницMaterial Safety Data Sheet: - Adsealwuhan lalalaОценок пока нет

- Introduction To Pharmacology by ZebДокумент31 страницаIntroduction To Pharmacology by ZebSanam MalikОценок пока нет

- CSR Report On Tata SteelДокумент72 страницыCSR Report On Tata SteelJagadish Sahu100% (1)

- NDT HandBook Volume 10 (NDT Overview)Документ600 страницNDT HandBook Volume 10 (NDT Overview)mahesh95% (19)

- Ajsl DecisionMakingModel4RoRoДокумент11 страницAjsl DecisionMakingModel4RoRolesta putriОценок пока нет

- Thesis Topics in Medicine in Delhi UniversityДокумент8 страницThesis Topics in Medicine in Delhi UniversityBecky Goins100% (2)

- MFD16I003 FinalДокумент16 страницMFD16I003 FinalAditya KumarОценок пока нет

- Saes T 883Документ13 страницSaes T 883luke luckyОценок пока нет

- A Short History of Denim: (C) Lynn Downey, Levi Strauss & Co. HistorianДокумент11 страницA Short History of Denim: (C) Lynn Downey, Levi Strauss & Co. HistorianBoier Sesh PataОценок пока нет

- Corporate Valuation WhartonДокумент6 страницCorporate Valuation Whartonebrahimnejad64Оценок пока нет

- Enhancing Guest Experience and Operational Efficiency in Hotels Through Robotic Technology-A Comprehensive Review.Документ8 страницEnhancing Guest Experience and Operational Efficiency in Hotels Through Robotic Technology-A Comprehensive Review.Chandigarh PhilosophersОценок пока нет

- What Is An EcosystemДокумент42 страницыWhat Is An Ecosystemjoniel05Оценок пока нет

- British Birds 10 LondДокумент376 страницBritish Birds 10 Londcassy98Оценок пока нет

- Travelstart Ticket (ZA10477979) PDFДокумент2 страницыTravelstart Ticket (ZA10477979) PDFMatthew PretoriusОценок пока нет

- Topic 6 Nested For LoopsДокумент21 страницаTopic 6 Nested For Loopsthbull02Оценок пока нет

- Modular ResumeДокумент1 страницаModular ResumeedisontОценок пока нет

- RIBA PoWUpdate 131009 ProbynMiersДокумент28 страницRIBA PoWUpdate 131009 ProbynMiersYellowLightОценок пока нет

- 2018 H2 JC1 MSM Differential Equations (Solutions)Документ31 страница2018 H2 JC1 MSM Differential Equations (Solutions)VincentОценок пока нет

- Blank FacebookДокумент2 страницыBlank Facebookapi-355481535Оценок пока нет

- Acc 106 Account ReceivablesДокумент40 страницAcc 106 Account ReceivablesAmirah NordinОценок пока нет

- Wire Rope TesterДокумент4 страницыWire Rope TesterclzagaОценок пока нет

- Space Saving, Tight AccessibilityДокумент4 страницыSpace Saving, Tight AccessibilityTran HuyОценок пока нет

- AREMA Shoring GuidelinesДокумент25 страницAREMA Shoring GuidelinesKCHESTER367% (3)

- EstoqueДокумент56 страницEstoqueGustavo OliveiraОценок пока нет

- Robbie Hemingway - Text God VIP EbookДокумент56 страницRobbie Hemingway - Text God VIP EbookKylee0% (1)

- APRStt Implementation Notes PDFДокумент36 страницAPRStt Implementation Notes PDFCT2IWWОценок пока нет

- Knitting in Satellite AntennaДокумент4 страницыKnitting in Satellite AntennaBhaswati PandaОценок пока нет