Вам также может понравиться

- Introduction To The Medical Billing ProcessДокумент34 страницыIntroduction To The Medical Billing ProcessSohailRaja100% (5)

- 35 Great SpeechesДокумент38 страниц35 Great Speechesaharish_iitk100% (2)

- Understanding Identity Through Philosophy and SocietyДокумент25 страницUnderstanding Identity Through Philosophy and Societyaharish_iitkОценок пока нет

- Identifying Personal ValuesДокумент4 страницыIdentifying Personal Valuesaharish_iitk100% (3)

- Acupressure Daily PracticesДокумент12 страницAcupressure Daily PracticesprasannakuberОценок пока нет

- Discover the Powerful Drivers of Human Behavior Through an Exploration of ValuesДокумент23 страницыDiscover the Powerful Drivers of Human Behavior Through an Exploration of Valuesaharish_iitk100% (2)

- Government of Jharkhand: Receipt of Online Payment of Stamp DДокумент4 страницыGovernment of Jharkhand: Receipt of Online Payment of Stamp DAniket RajОценок пока нет

- 17 of The World's Most Powerful Written Persuasion TechniquesДокумент10 страниц17 of The World's Most Powerful Written Persuasion Techniquesaharish_iitk100% (2)

- Renewal NoticeДокумент2 страницыRenewal NoticeJerry LamaОценок пока нет

- Underwriting Motor InsuranceДокумент8 страницUnderwriting Motor InsuranceNikhil SharmaОценок пока нет

- Home Loan - Certificate - 2022-23Документ1 страницаHome Loan - Certificate - 2022-23cont2chandu100% (1)

- Interest Certificate Nov06 205111Документ1 страницаInterest Certificate Nov06 205111Sambasivarao ChindamОценок пока нет

- Reg No: Dl8Cav0116: Registration Certificate For VehicleДокумент1 страницаReg No: Dl8Cav0116: Registration Certificate For Vehicleh4ckerОценок пока нет

- 1563614521775Документ1 страница1563614521775JatinderPalОценок пока нет

- PolicyДокумент1 страницаPolicyAlok SinghОценок пока нет

- Premium Receipt PDFДокумент1 страницаPremium Receipt PDFChidambaram VОценок пока нет

- Estate Deductions ExplainedДокумент22 страницыEstate Deductions ExplainedAngelika BalmeoОценок пока нет

- Munich Re IAR Policy Insured DetailsДокумент51 страницаMunich Re IAR Policy Insured DetailsbobyОценок пока нет

- Duplicate receipt for insurance renewalДокумент1 страницаDuplicate receipt for insurance renewalUTSAV DUBEYОценок пока нет

- Obama Hypnosis: A Theory by The RightДокумент67 страницObama Hypnosis: A Theory by The Rightpappalardo100% (2)

- Prashant (1) CompletedДокумент1 страницаPrashant (1) CompletedAsifshaikh7566Оценок пока нет

- Consolidated Premium Paid STMT 2020-2021 PDFДокумент1 страницаConsolidated Premium Paid STMT 2020-2021 PDFSHITESH KUMARОценок пока нет

- Mrunal Land ReformsДокумент79 страницMrunal Land Reformsaharish_iitk100% (1)

- Statement of Public Provident Fund Account: Ms - Neha Raghubar YadavДокумент2 страницыStatement of Public Provident Fund Account: Ms - Neha Raghubar YadavNeha100% (1)

- Premium Paid AcknowledgementДокумент1 страницаPremium Paid Acknowledgementharsh421Оценок пока нет

- PPF Statement YTD Dec'23Документ1 страницаPPF Statement YTD Dec'23sumanpal78Оценок пока нет

- Top 20000 Spoken WordsДокумент1 717 страницTop 20000 Spoken Wordsaharish_iitk100% (1)

- Tax Deduction for Health Insurance Premium and Medical ExpensesДокумент2 страницыTax Deduction for Health Insurance Premium and Medical ExpensesReeju KarunakaranОценок пока нет

- Policy Protection PlanДокумент36 страницPolicy Protection Plankrishna_1238Оценок пока нет

- Credit Card Bill Payments Rs 130.38 IndusIndДокумент1 страницаCredit Card Bill Payments Rs 130.38 IndusIndPriyanka VermaОценок пока нет

- HDFC Life Premium Receipts Nov 2022Документ1 страницаHDFC Life Premium Receipts Nov 2022kapsekunalОценок пока нет

- DHLF - Loan Sanction LetterДокумент2 страницыDHLF - Loan Sanction LetterRaju BhaiОценок пока нет

- 4 PDFДокумент4 страницы4 PDFsatish sharmaОценок пока нет

- Loan Settlement LetterДокумент2 страницыLoan Settlement LetterRITIK DESHBHRATARОценок пока нет

- Tax Invoice for Arasi Soaps Coconut Oil Bath SoapДокумент1 страницаTax Invoice for Arasi Soaps Coconut Oil Bath SoapSreedharОценок пока нет

- Annexure - 1: Mode of RepaymentДокумент2 страницыAnnexure - 1: Mode of RepaymentRohit chavanОценок пока нет

- True Credits loan approval letter summarizedДокумент17 страницTrue Credits loan approval letter summarizedSrinivasu Chintala100% (1)

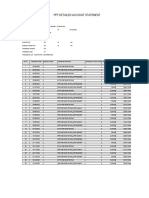

- Cholamandalam Loan Account StatementДокумент17 страницCholamandalam Loan Account StatementTrilochan Banchhor50% (2)

- Certificate of Registration-Form 23Документ1 страницаCertificate of Registration-Form 23Joy GudivadaОценок пока нет

- CERTIFICATE For Claiming Deduction Under Section 24 (B) & 80C (2) (Xviii) of INCOME TAX ACT, 1961Документ1 страницаCERTIFICATE For Claiming Deduction Under Section 24 (B) & 80C (2) (Xviii) of INCOME TAX ACT, 1961Raman SharmaОценок пока нет

- Sanction Letter For ICICI Bank Car Loan Application of MITESHBHAI SARATANBHAI BHARVAD - NC002047354Документ1 страницаSanction Letter For ICICI Bank Car Loan Application of MITESHBHAI SARATANBHAI BHARVAD - NC002047354Sanjay SolankiОценок пока нет

- HDFC ERGO General Insurance Company LimitedДокумент4 страницыHDFC ERGO General Insurance Company LimitedTESTERPERSONОценок пока нет

- Welcome LetterДокумент4 страницыWelcome LetterChetan ChoudharyОценок пока нет

- Sanction LetterДокумент5 страницSanction LetterIssac EbbuОценок пока нет

- E Sign DocДокумент26 страницE Sign DocShaik ShabanaОценок пока нет

- SBI FormДокумент16 страницSBI Formapi-373588783% (6)

- Loan Cum Hypothecation Agreement: L&T Finance Limited (Erstwhile Known As Family Credit LTD.)Документ19 страницLoan Cum Hypothecation Agreement: L&T Finance Limited (Erstwhile Known As Family Credit LTD.)niranjan krishnaОценок пока нет

- Registration Certificate of Vehicle: Issuing Authority: Madhubani, BiharДокумент1 страницаRegistration Certificate of Vehicle: Issuing Authority: Madhubani, Bihartabrez alamОценок пока нет

- Life Motors: Shantanu BLDG, Shop No8/9, Pawar Nagar, Thane (West), Thane:400601Документ2 страницыLife Motors: Shantanu BLDG, Shop No8/9, Pawar Nagar, Thane (West), Thane:400601abhishek pandeyОценок пока нет

- ICICI Health InsuranceДокумент1 страницаICICI Health Insurancecanjiatp76260% (1)

- Loan Details: TWO - Wheeler Sandhya Automotives, KURNOOLДокумент1 страницаLoan Details: TWO - Wheeler Sandhya Automotives, KURNOOLmohammed rafiОценок пока нет

- HDFC Loan Approval for Consumer Durable PurchaseДокумент1 страницаHDFC Loan Approval for Consumer Durable PurchaseSâñjây Bîñd0% (1)

- 10789103Документ7 страниц10789103Sachit MalikОценок пока нет

- No Objection Certificate PDFДокумент1 страницаNo Objection Certificate PDFPankaj ChouhanОценок пока нет

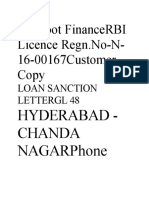

- Muthoot Finance Loan Sanction LetterДокумент30 страницMuthoot Finance Loan Sanction LetterTHE PHILOSOPHER MADDYОценок пока нет

- Interest Certificate: Shivam Garg and Ramkrishna GargДокумент1 страницаInterest Certificate: Shivam Garg and Ramkrishna GargShivamОценок пока нет

- PMJBY Scheme Provides Rs. 2 Lakh Life Cover for Rs. 330/YearДокумент2 страницыPMJBY Scheme Provides Rs. 2 Lakh Life Cover for Rs. 330/YearrbuvanesОценок пока нет

- Preventive Health Check Up Receipt PDFДокумент41 страницаPreventive Health Check Up Receipt PDFsan mohОценок пока нет

- For HDFC ERGO General Insurance Company LTDДокумент2 страницыFor HDFC ERGO General Insurance Company LTDNAVEEN H EОценок пока нет

- 80D CertificateДокумент2 страницы80D CertificateSiva KadaliОценок пока нет

- E 7403445Документ2 страницыE 7403445Prince CharliОценок пока нет

- Elss STMT HBM295 2022 - 2023Документ1 страницаElss STMT HBM295 2022 - 2023Sidharth SОценок пока нет

- 4030CD30258077 Noc PDFДокумент1 страница4030CD30258077 Noc PDFAnu ChandruОценок пока нет

- Health InsuranceДокумент7 страницHealth InsuranceRadhika Rampal100% (1)

- Mitc PDFДокумент3 страницыMitc PDFShreeОценок пока нет

- Leave and License Agreement: Particulars Amount Paid GRN/Transaction Id DateДокумент6 страницLeave and License Agreement: Particulars Amount Paid GRN/Transaction Id DateAnonymous eCmTYonQ84Оценок пока нет

- Self - 16sep22 - ELSS StatementДокумент1 страницаSelf - 16sep22 - ELSS Statementaju3167Оценок пока нет

- United India Insurance Company LimitedДокумент2 страницыUnited India Insurance Company LimitedThoufeeq IbrahimОценок пока нет

- PremiumRept MDS - RameshДокумент2 страницыPremiumRept MDS - Rameshnavengg521Оценок пока нет

- Manpower Agreement SampleДокумент3 страницыManpower Agreement Sampleashoka187Оценок пока нет

- Policy Doc PDFДокумент4 страницыPolicy Doc PDFGajen SinghОценок пока нет

- SBI General's Health Insurance Policy - Retail: Take Control of Your Family's Health. and Happiness TooДокумент2 страницыSBI General's Health Insurance Policy - Retail: Take Control of Your Family's Health. and Happiness ToobpshuОценок пока нет

- Reliance Group Credit Shield Plan Secures LoansДокумент6 страницReliance Group Credit Shield Plan Secures LoansMahipal YadavОценок пока нет

- 善因緣Документ8 страниц善因緣api-3758017Оценок пока нет

- Writing Programs Textbook List - 1Документ5 страницWriting Programs Textbook List - 1aharish_iitkОценок пока нет

- China China China China China China China China China China China China China China China China China China China China China ChinaДокумент55 страницChina China China China China China China China China China China China China China China China China China China China China Chinaaharish_iitk0% (1)

- Essay Guidelines: Moral Rights Paper: ESSAY. I'll Need To See It To Understand What You've Written About ItДокумент2 страницыEssay Guidelines: Moral Rights Paper: ESSAY. I'll Need To See It To Understand What You've Written About Itaharish_iitkОценок пока нет

- Docs Voith CouplingsДокумент39 страницDocs Voith CouplingsJuan Andres Coello CassinelliОценок пока нет

- HitachiДокумент1 страницаHitachiaharish_iitkОценок пока нет

- Indian Rock-Cut ArchitectureДокумент7 страницIndian Rock-Cut Architectureaharish_iitk100% (1)

- Requirement of StructureДокумент1 страницаRequirement of Structureaharish_iitkОценок пока нет

- Tender Electrical Mar 10Документ19 страницTender Electrical Mar 10aharish_iitkОценок пока нет

- Technical & Financial Bid ProformaДокумент2 страницыTechnical & Financial Bid Proformaaharish_iitkОценок пока нет

- Tender FormДокумент7 страницTender Formaharish_iitkОценок пока нет

- Product CatalogueДокумент95 страницProduct Catalogueaharish_iitkОценок пока нет

- Tender Form IFA Equipment (R& D Lab) - 3Документ5 страницTender Form IFA Equipment (R& D Lab) - 3aharish_iitkОценок пока нет

- Adhunik Systems Kanpur 29.06.10Документ2 страницыAdhunik Systems Kanpur 29.06.10aharish_iitkОценок пока нет

- Tender Form IFA Equipmnt (Comercial Scale) - 1Документ3 страницыTender Form IFA Equipmnt (Comercial Scale) - 1aharish_iitkОценок пока нет

- Letter HeadДокумент1 страницаLetter Headaharish_iitkОценок пока нет

- Schedule of Premium (Amount in RS.)Документ4 страницыSchedule of Premium (Amount in RS.)Yogesh ChhaprooОценок пока нет

- Cover SRCC loss damageДокумент2 страницыCover SRCC loss damageKhawar RiazОценок пока нет

- My Insurance Plan Doesnt Cover Mental Health and I Need A Psychologist What Do I Doradjj PDFДокумент8 страницMy Insurance Plan Doesnt Cover Mental Health and I Need A Psychologist What Do I Doradjj PDFBanksHerbert0Оценок пока нет

- Manoj Maheshrao Khandare Project ReportДокумент39 страницManoj Maheshrao Khandare Project Reportshubham moonОценок пока нет

- CJL 5000 Hsa Plan 2024 SBC Final 10182023Документ8 страницCJL 5000 Hsa Plan 2024 SBC Final 10182023dominicvjohnson03Оценок пока нет

- Policy - TruДокумент87 страницPolicy - Truapi-523902606Оценок пока нет

- Institute of London Underwriters Standard Dutch Hull FormДокумент7 страницInstitute of London Underwriters Standard Dutch Hull FormSuryadilaga JajangОценок пока нет

- Student Health Insurance: San José State UniversityДокумент20 страницStudent Health Insurance: San José State UniversityDeni ZenОценок пока нет

- HDFC ERGO General Insurance Certificate of InsuranceДокумент2 страницыHDFC ERGO General Insurance Certificate of InsuranceAlfred FernandesОценок пока нет

- ProHealth V7 Accordian April'23 02Документ8 страницProHealth V7 Accordian April'23 02Sreeraj P SОценок пока нет

- STANDARD CERTIFICATEДокумент1 страницаSTANDARD CERTIFICATEavi coolОценок пока нет

- Labor law issues in employee compensation and benefitsДокумент6 страницLabor law issues in employee compensation and benefitsBen D. ProtacioОценок пока нет

- EB MediShield Plus BrochureДокумент6 страницEB MediShield Plus Brochurediefenbaker13Оценок пока нет

- 1#@1Документ47 страниц1#@1Ng Chia ShenОценок пока нет

- Commercial Vehicle InsuranceДокумент124 страницыCommercial Vehicle InsurancePratik SapkotaОценок пока нет

- Table of BenefitsДокумент41 страницаTable of BenefitsTaurai ChiwanzaОценок пока нет

- Critical Reasoning: "Trap Answers Lure You To Weaken Flawed Arguments With Similarly Flawed Answer Options."Документ17 страницCritical Reasoning: "Trap Answers Lure You To Weaken Flawed Arguments With Similarly Flawed Answer Options."devilsharmaОценок пока нет

- Policy Schedule Cum Certificate of InsuranceДокумент2 страницыPolicy Schedule Cum Certificate of InsuranceROhit MalikОценок пока нет

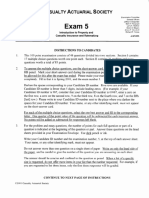

- Exam 5: Casualty Actuarial SocietyДокумент25 страницExam 5: Casualty Actuarial SocietyPETERОценок пока нет

- Sample PPLДокумент3 страницыSample PPLDrew PachecoОценок пока нет

- Two Wheeler Policy PDFДокумент2 страницыTwo Wheeler Policy PDFVijaya SimhaОценок пока нет

- InsuranceДокумент6 страницInsurancesourabhОценок пока нет

- Loblaws GF Benefits ComparisonДокумент14 страницLoblaws GF Benefits ComparisonOpenFileОценок пока нет

- 450 499 PDFДокумент44 страницы450 499 PDFSamuelОценок пока нет

- Chapter-Ii Review of LiteratureДокумент79 страницChapter-Ii Review of LiteratureMubeenОценок пока нет

- Sana Gul 1Документ2 страницыSana Gul 1raoshahzad9000Оценок пока нет