Вам также может понравиться

- p1 Midterm 2012Документ8 страницp1 Midterm 2012marygraceomacОценок пока нет

- INVESTMENTSДокумент27 страницINVESTMENTSJao FloresОценок пока нет

- Assement Exam-Dysas 1st Quarter-P1Документ5 страницAssement Exam-Dysas 1st Quarter-P1JohnAllenMarillaОценок пока нет

- Ms 03 - CVP AnalysisДокумент10 страницMs 03 - CVP AnalysisDin Rose GonzalesОценок пока нет

- Aud ProbДокумент9 страницAud ProbKulet AkoОценок пока нет

- Long Quiz Investments Class IJ (5:30-7:30 TWFS)Документ5 страницLong Quiz Investments Class IJ (5:30-7:30 TWFS)Jolina AynganОценок пока нет

- 3 4Документ5 страниц3 4RenОценок пока нет

- NullДокумент22 страницыNullapi-28191758100% (1)

- Quiz 2 - Corp Liqui and Installment SalesДокумент8 страницQuiz 2 - Corp Liqui and Installment SalesKenneth Christian WilburОценок пока нет

- Audit of LiabsДокумент2 страницыAudit of LiabsRommel Royce CadapanОценок пока нет

- CostДокумент33 страницыCostversmajardoОценок пока нет

- 04sol-Investments WB 1stДокумент21 страница04sol-Investments WB 1stNJ SyОценок пока нет

- Module QuizsДокумент24 страницыModule QuizswsviviОценок пока нет

- MAS ReviewerДокумент22 страницыMAS ReviewerBeverly HeliОценок пока нет

- Problem 4Документ6 страницProblem 4jhobsОценок пока нет

- Auditing - Midterms Investment QuizДокумент6 страницAuditing - Midterms Investment QuizmoОценок пока нет

- Quiz Recl FinancingДокумент1 страницаQuiz Recl FinancingLou Brad IgnacioОценок пока нет

- Dahlia DahliaДокумент21 страницаDahlia Dahliaambrosia96Оценок пока нет

- What Is The Correct Amount of Inventory?: SolutionДокумент3 страницыWhat Is The Correct Amount of Inventory?: SolutionSofia LaoОценок пока нет

- Colegio de La Purisima Concepcion: School of The Archdiocese of Capiz Roxas CityДокумент5 страницColegio de La Purisima Concepcion: School of The Archdiocese of Capiz Roxas CityJhomel Domingo GalvezОценок пока нет

- Quizbowl 2Документ10 страницQuizbowl 2lorenceabad07Оценок пока нет

- Integrated Topic 1 (Far-004a)Документ4 страницыIntegrated Topic 1 (Far-004a)lyndon delfinОценок пока нет

- Unit 1 History and New Directions of Accounting Research Exercise 1Документ5 страницUnit 1 History and New Directions of Accounting Research Exercise 1Ivan AnaboОценок пока нет

- Cash and Acrrual Basis QUIZДокумент2 страницыCash and Acrrual Basis QUIZMarii M.100% (1)

- Auditing ProblemsДокумент6 страницAuditing ProblemsMaurice AgbayaniОценок пока нет

- Requirement No. 1: PROBLEM NO. 1 - Heats CorporationДокумент1 страницаRequirement No. 1: PROBLEM NO. 1 - Heats CorporationjhobsОценок пока нет

- AP Solutions 2016Документ13 страницAP Solutions 2016Mary Ann Gumpay Rago100% (1)

- Ix - Completing The Audit and Audit of Financial Statements Presentation PROBLEM NO. 1 - Statement of Financial PositionДокумент12 страницIx - Completing The Audit and Audit of Financial Statements Presentation PROBLEM NO. 1 - Statement of Financial PositionKirstine DelegenciaОценок пока нет

- JPIA CA5101 MerchxManuf Reviewer PDFДокумент7 страницJPIA CA5101 MerchxManuf Reviewer PDFmei angelaОценок пока нет

- StudentДокумент45 страницStudentJoel Christian MascariñaОценок пока нет

- TBCH09Документ6 страницTBCH09Samit TandukarОценок пока нет

- Problem 4Документ2 страницыProblem 4mhikeedelantarОценок пока нет

- Auditor's Cup Questions-2Документ8 страницAuditor's Cup Questions-2VtgОценок пока нет

- This Study Resource Was: Process Costing - AverageДокумент7 страницThis Study Resource Was: Process Costing - AverageIllion IllionОценок пока нет

- Ap106 Investments and Intangible AssetsДокумент5 страницAp106 Investments and Intangible Assetsbright SpotifyОценок пока нет

- MS03 09 Capital Budgeting Part 2 EncryptedДокумент6 страницMS03 09 Capital Budgeting Part 2 EncryptedKate Crystel reyesОценок пока нет

- Quiz 9 A6Документ20 страницQuiz 9 A6Lara FloresОценок пока нет

- An SME Prepared The Following Post Closing Trial Balance at YearДокумент1 страницаAn SME Prepared The Following Post Closing Trial Balance at YearRaca DesuОценок пока нет

- Acctg 112Документ3 страницыAcctg 112Rathew Cassey PencilОценок пока нет

- RFBT Quiz 1: Forgery. After Giving A Notice of Dishonor, Which of The Following Is Not Correct?Документ7 страницRFBT Quiz 1: Forgery. After Giving A Notice of Dishonor, Which of The Following Is Not Correct?cheni magsaelОценок пока нет

- MAS Midterm Exam PDFДокумент12 страницMAS Midterm Exam PDFZyrelle DelgadoОценок пока нет

- MB2 2013 Ap Set AДокумент6 страницMB2 2013 Ap Set AMary Queen Ramos-UmoquitОценок пока нет

- CA01 VariableCostingFДокумент114 страницCA01 VariableCostingFVenise BaliaОценок пока нет

- 01 Quiz 1Документ2 страницы01 Quiz 1anna mae orcioОценок пока нет

- Auditing 1 Final ExamДокумент8 страницAuditing 1 Final ExamEdemson NavalesОценок пока нет

- Audit of Inventories - Part 2Документ4 страницыAudit of Inventories - Part 2Mark Lawrence YusiОценок пока нет

- Quiz 1 - Balance SheetДокумент3 страницыQuiz 1 - Balance SheetCindy Craus100% (1)

- A Mining Company Is Considering To Open A New Coal MineДокумент4 страницыA Mining Company Is Considering To Open A New Coal MineD Y Patil Institute of MCA and MBAОценок пока нет

- Chapter 3 Quiz KeyДокумент2 страницыChapter 3 Quiz KeyAmna MalikОценок пока нет

- CFAS Reviewer (Unedited)Документ16 страницCFAS Reviewer (Unedited)Kevin OnaroОценок пока нет

- Accounting QuestionДокумент8 страницAccounting QuestionMusa D Acid100% (1)

- Quiz Number 3Документ3 страницыQuiz Number 3Lopez, Azzia M.Оценок пока нет

- Edoc - Pub Problems Solving Masdocx PDFДокумент6 страницEdoc - Pub Problems Solving Masdocx PDFReznakОценок пока нет

- Ia3 IsДокумент3 страницыIa3 IsMary Joy CabilОценок пока нет

- Audit and Assurance Bank and Other Financial InstitutionsДокумент44 страницыAudit and Assurance Bank and Other Financial InstitutionsJohann VillegasОценок пока нет

- Practical Accounting Problems 1Документ4 страницыPractical Accounting Problems 1Eleazer Ego-oganОценок пока нет

- Practical Accounting 1Документ14 страницPractical Accounting 1Anonymous Lih1laaxОценок пока нет

- Financial Accounting Part 3Документ6 страницFinancial Accounting Part 3Christopher Price67% (3)

- Practical Accounting Part 1Документ18 страницPractical Accounting Part 1Jonacress Callo CagatinОценок пока нет

- Finacc AnaДокумент8 страницFinacc AnaKonjiki Ashisogi JizōОценок пока нет

- Chang CДокумент3 страницыChang CmarygraceomacОценок пока нет

- Chapter 22Документ8 страницChapter 22marygraceomacОценок пока нет

- CH 03 Process CostingДокумент19 страницCH 03 Process CostingHadassahFayОценок пока нет

- Intangible and Other AssetsДокумент7 страницIntangible and Other AssetsHope Joy Velasco AprueboОценок пока нет

- Microsoft Word - 02 Quiz Bee - P1 and TOA (Average) PDFДокумент5 страницMicrosoft Word - 02 Quiz Bee - P1 and TOA (Average) PDFNora PasaОценок пока нет

- Chang AДокумент6 страницChang AmarygraceomacОценок пока нет

- Father Saturnino Urios University Accountancy Program AIR-Cluster 1 (Drill #4)Документ10 страницFather Saturnino Urios University Accountancy Program AIR-Cluster 1 (Drill #4)marygraceomacОценок пока нет

- Ms Air 01Документ9 страницMs Air 01marygraceomacОценок пока нет

- Tax Haven PDFДокумент60 страницTax Haven PDFRemon Agit RimangОценок пока нет

- Aggregate PlanningДокумент10 страницAggregate PlanningmarygraceomacОценок пока нет

- MQ 1 Receivables and InventoryДокумент4 страницыMQ 1 Receivables and Inventorymarygraceomac100% (2)

- Formulas in Computing Economic Order QuantityДокумент13 страницFormulas in Computing Economic Order QuantitymarygraceomacОценок пока нет

- Father Saturnino Urios University Accountancy Program AIR-Cluster 1 (Drill #2)Документ11 страницFather Saturnino Urios University Accountancy Program AIR-Cluster 1 (Drill #2)marygraceomacОценок пока нет

- P2 MaterialsДокумент9 страницP2 MaterialsmarygraceomacОценок пока нет

- Ms Air 01Документ9 страницMs Air 01marygraceomacОценок пока нет

- Total Quality Management in Automotive Supply Chain in The U.S. (6!8!12)Документ9 страницTotal Quality Management in Automotive Supply Chain in The U.S. (6!8!12)marygraceomacОценок пока нет

- BLT Quizzer (Unknown) - Law On Negotiable InstrumentsДокумент7 страницBLT Quizzer (Unknown) - Law On Negotiable InstrumentsJasper Ivan PeraltaОценок пока нет

- FQ 002 Book Value and Earnings Per ShareДокумент3 страницыFQ 002 Book Value and Earnings Per SharemarygraceomacОценок пока нет

- Father Saturnino Urios University Accountancy Program AIR-Cluster 1 (Drill #2)Документ11 страницFather Saturnino Urios University Accountancy Program AIR-Cluster 1 (Drill #2)marygraceomacОценок пока нет

- SPQ 003 Employee Benefits, Leases, and Other LiabilitiesДокумент3 страницыSPQ 003 Employee Benefits, Leases, and Other LiabilitiesmarygraceomacОценок пока нет

- Diagnostic Exam 1.1 AKДокумент15 страницDiagnostic Exam 1.1 AKmarygraceomacОценок пока нет

- MQ 1 Receivables and InventoryДокумент4 страницыMQ 1 Receivables and Inventorymarygraceomac100% (2)

- FQ 002 Book Value and Earnings Per ShareДокумент3 страницыFQ 002 Book Value and Earnings Per SharemarygraceomacОценок пока нет

- FQ 001 Sharehoders - Equity and Retained EarningsДокумент4 страницыFQ 001 Sharehoders - Equity and Retained Earningsmarygraceomac83% (6)

- 16 PDFДокумент7 страниц16 PDFmarygraceomacОценок пока нет

- Lease and Accounting For Income Tax DrillsДокумент3 страницыLease and Accounting For Income Tax DrillsmarygraceomacОценок пока нет

- Diagnostic Exam 1.23 AKДокумент13 страницDiagnostic Exam 1.23 AKmarygraceomacОценок пока нет

- 2007 - The Making of An Icon - LoДокумент16 страниц2007 - The Making of An Icon - LomarygraceomacОценок пока нет

- ENG5 Q1 W1 Lesson 3 Filling Out Forms Accurately (School Forms, Deposit Slip, Withdrawal Slip)Документ29 страницENG5 Q1 W1 Lesson 3 Filling Out Forms Accurately (School Forms, Deposit Slip, Withdrawal Slip)Catherine Rica CanonigoОценок пока нет

- Lecture 12 Equity Analysis and ValuationДокумент31 страницаLecture 12 Equity Analysis and ValuationKhushbooОценок пока нет

- Guidelines and Procedures For Entering Into Joint Venture (JV) Agreements Between Government and Private EntitiesДокумент25 страницGuidelines and Procedures For Entering Into Joint Venture (JV) Agreements Between Government and Private EntitiesPoc Politi-ko ChannelОценок пока нет

- JSW Steel LTD PDFДокумент4 страницыJSW Steel LTD PDFTanveer NОценок пока нет

- ArundelДокумент6 страницArundelArnab Pramanik100% (1)

- Chapter 13 SolutionsДокумент26 страницChapter 13 SolutionsMathew Idanan0% (1)

- Salon Business Plan For Starting Your Own Beauty Salon ServiceДокумент97 страницSalon Business Plan For Starting Your Own Beauty Salon ServiceAlhaji Daramy100% (5)

- What Is Stablecoin?: A Survey On Its Mechanism and Potential As Decentralized Payment SystemsДокумент18 страницWhat Is Stablecoin?: A Survey On Its Mechanism and Potential As Decentralized Payment SystemsSAECTARОценок пока нет

- 44th Annual Report 2005-2006: National Organic Chemical Industries LimitedДокумент73 страницы44th Annual Report 2005-2006: National Organic Chemical Industries Limitedsandesh1506Оценок пока нет

- Powers of Corporation TableДокумент2 страницыPowers of Corporation TableAna MendezОценок пока нет

- Inner Circle Trader Ict Forex Ict NotesДокумент110 страницInner Circle Trader Ict Forex Ict NotesjcferreiraОценок пока нет

- Cash QuizДокумент6 страницCash QuizGwen Cabarse PansoyОценок пока нет

- 6 Igcse - Accounting - Errors - Past - Papers - UnlockedДокумент58 страниц6 Igcse - Accounting - Errors - Past - Papers - Unlockedshivom talrejaОценок пока нет

- Thank You For Paying On-Time: Basic Housing Solutions, IncДокумент1 страницаThank You For Paying On-Time: Basic Housing Solutions, IncMarcelo AnfoneОценок пока нет

- Management Accounting Module - VДокумент11 страницManagement Accounting Module - Vdivya kalyaniОценок пока нет

- Financial Statements Ratio Analysis of InfosysДокумент15 страницFinancial Statements Ratio Analysis of InfosysVishal KushwahaОценок пока нет

- Extra 3Документ2 страницыExtra 3Ahmed GemyОценок пока нет

- 14 - Simple Interest MODULE 6Документ16 страниц14 - Simple Interest MODULE 6Mabel LynОценок пока нет

- Housing ReportДокумент6 страницHousing ReportJasmin QuebidoОценок пока нет

- Digital Lending: KenyaДокумент31 страницаDigital Lending: KenyaRick OdomОценок пока нет

- Michael Rubel ResumeДокумент1 страницаMichael Rubel Resumeapi-207919284Оценок пока нет

- Memo For Brokers: Philippine Stock Exchange, IncДокумент31 страницаMemo For Brokers: Philippine Stock Exchange, IncBrian AlmeriaОценок пока нет

- Yadadri Bhuvanagiri - Pochampally - Mpups Bheemanpally - 36200901801 - P200901801 - 20231109 - 000008 - Green Chalk BoardsДокумент2 страницыYadadri Bhuvanagiri - Pochampally - Mpups Bheemanpally - 36200901801 - P200901801 - 20231109 - 000008 - Green Chalk BoardsdurgaprasadОценок пока нет

- CA Inter Paper 2 All Question PapersДокумент175 страницCA Inter Paper 2 All Question PapersNivedita SharmaОценок пока нет

- The Franchisor Feasibility StudyДокумент12 страницThe Franchisor Feasibility StudyLeighgendary CruzОценок пока нет

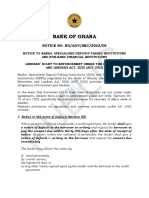

- BOG Notice BG GOV SEC 2022 05 Lenders Right To Enforcement Under The Borrowers and Lenders Act 2020 Act 1052 1Документ3 страницыBOG Notice BG GOV SEC 2022 05 Lenders Right To Enforcement Under The Borrowers and Lenders Act 2020 Act 1052 1Fuaad DodooОценок пока нет

- Business and Corporate LawДокумент3 страницыBusiness and Corporate LawRuhaan TanvirОценок пока нет

- 06 - Class 06 - Trade SetupsДокумент12 страниц06 - Class 06 - Trade SetupsChandler BingОценок пока нет

- Economics 12, 2 SolutionsДокумент48 страницEconomics 12, 2 Solutionssantpreetkaur659Оценок пока нет

- For ClosureДокумент18 страницFor Closuremau_cajipeОценок пока нет