Вам также может понравиться

- Quickbooks Online CertificatДокумент137 страницQuickbooks Online CertificatRandy Fernandez100% (6)

- CDCS ExamДокумент24 страницыCDCS ExamPangoea Pangoea100% (1)

- Activity Balancing Your Checking AccountДокумент4 страницыActivity Balancing Your Checking AccountMellanie Garcia100% (1)

- QBO Certification Training Guide - v031122Документ308 страницQBO Certification Training Guide - v031122Jonhmark AniñonОценок пока нет

- A Study On South Indain Bank LTDДокумент67 страницA Study On South Indain Bank LTDKarthik Ravi67% (3)

- Industry Analysis AXIS BANKДокумент13 страницIndustry Analysis AXIS BANKEric D'souza0% (1)

- 09875700009652Документ3 страницы09875700009652Glo SmithОценок пока нет

- 004 - NRI - Main Application Form - FillableДокумент6 страниц004 - NRI - Main Application Form - FillableAnkur MishRraОценок пока нет

- Investment Policy of AIBLДокумент70 страницInvestment Policy of AIBLSobuj BernardОценок пока нет

- NPA Management in SBIДокумент118 страницNPA Management in SBIMeenakshiDhirwani83% (12)

- Npl-Southeast BankДокумент33 страницыNpl-Southeast Banksumaiya sumaОценок пока нет

- Final Internship Report On NBLДокумент89 страницFinal Internship Report On NBLMd. Rahat ChowdhuryОценок пока нет

- Internship of NGOДокумент60 страницInternship of NGORao SОценок пока нет

- Loan Processing, Credit Appraisal, Follow-Up &recovery Procedure of IFIC Bank LimitedДокумент93 страницыLoan Processing, Credit Appraisal, Follow-Up &recovery Procedure of IFIC Bank LimitedpriyankaОценок пока нет

- Financial Literacy PaperДокумент50 страницFinancial Literacy PaperRik Chakraborty100% (1)

- Case Study CooperativesДокумент10 страницCase Study Cooperativesnegi_hinata100% (4)

- Full ReportДокумент48 страницFull ReportJahid Hassan0% (1)

- Operating System of ICB Unit FundДокумент58 страницOperating System of ICB Unit FundShahriar Zaman HridoyОценок пока нет

- Relationship Between The Financial Inclusion and DevelopmentДокумент26 страницRelationship Between The Financial Inclusion and DevelopmentMango7187Оценок пока нет

- INTERNSHIP REPORT On HRM of SBLДокумент65 страницINTERNSHIP REPORT On HRM of SBLAsibur RahmanОценок пока нет

- Internship of NGOДокумент63 страницыInternship of NGOMmeraKi100% (2)

- Fianal Project PapaniДокумент43 страницыFianal Project PapaniJyoti Ranjan MishraОценок пока нет

- "Title": Mr. Hitesh Vijay ChavhanДокумент87 страниц"Title": Mr. Hitesh Vijay ChavhanAfreenОценок пока нет

- Financial Performance Analysis of Al Arafa Bank Ltd.Документ78 страницFinancial Performance Analysis of Al Arafa Bank Ltd.Munsi Araf60% (5)

- Internship ReportДокумент62 страницыInternship ReportShariful IslamОценок пока нет

- Internship Report, Dubai Islamic BankДокумент61 страницаInternship Report, Dubai Islamic BankMuhammad DaniYal Rashid75% (4)

- Letter of Transmittal: Auditing of An Ngo: A Case Study On Aware Project Funded by Actionaid BangladeshДокумент58 страницLetter of Transmittal: Auditing of An Ngo: A Case Study On Aware Project Funded by Actionaid BangladeshAbdullah Al NomanОценок пока нет

- Rajkot People's Co-Op - Bank Ltd.Документ72 страницыRajkot People's Co-Op - Bank Ltd.Kishan Gokani100% (1)

- Assignment Point - Solution For Best Assignment Paper: Internal Control Systems in IFIC Bank LimitedДокумент35 страницAssignment Point - Solution For Best Assignment Paper: Internal Control Systems in IFIC Bank LimitedNishatОценок пока нет

- Credit Risk Management-City BankДокумент69 страницCredit Risk Management-City BankGobinda saha100% (1)

- Financial Statement Analysis of SbiДокумент61 страницаFinancial Statement Analysis of SbiGayatri Chiliveri100% (1)

- Raihan FarafieeДокумент53 страницыRaihan FarafieeNiaz MorshedОценок пока нет

- Project On Working CapitalДокумент48 страницProject On Working CapitalSandeepKhandelwalОценок пока нет

- Internship Report of NCC Bank Foreign ExchangeДокумент90 страницInternship Report of NCC Bank Foreign ExchangeFariha FerdowsОценок пока нет

- 6th Sem Project 1Документ87 страниц6th Sem Project 1GauravsОценок пока нет

- Internship Report On Financial Performance Analysis of Exim Bank LTDДокумент40 страницInternship Report On Financial Performance Analysis of Exim Bank LTDNure AlamОценок пока нет

- Ratio AnalysisДокумент69 страницRatio AnalysisAniqa AshrafОценок пока нет

- Hailey College of Commerce: University of The PunjabДокумент59 страницHailey College of Commerce: University of The Punjabwahidbc09001Оценок пока нет

- Internship ReportДокумент66 страницInternship Reporturooj fatimaОценок пока нет

- Project Report: Submitted ToДокумент51 страницаProject Report: Submitted ToJannatul FerdousОценок пока нет

- Xin Su - EFT ApplicationДокумент5 страницXin Su - EFT ApplicationSusan SuОценок пока нет

- Final Report SHANKARДокумент105 страницFinal Report SHANKARchinkijsrОценок пока нет

- Final Internship Report On NBLДокумент89 страницFinal Internship Report On NBLMonjurul Alam100% (5)

- Banking System Analysis of IFIC Bank LimitedДокумент28 страницBanking System Analysis of IFIC Bank LimitedMd Omar FaruqОценок пока нет

- Investment Mechanism of Islami Bank BangladeshДокумент67 страницInvestment Mechanism of Islami Bank BangladeshImranAhamedShakhor50% (2)

- Sterling Institute of Management StudiesДокумент12 страницSterling Institute of Management StudieskristokunsОценок пока нет

- Hubee Ali ThesisДокумент8 страницHubee Ali ThesisMayum AkhterОценок пока нет

- The Asean Secretariat Invites Asean Nationals To Apply For The Following VacancyДокумент4 страницыThe Asean Secretariat Invites Asean Nationals To Apply For The Following VacancyEfendi SiahaanОценок пока нет

- Malik Asad Pervez's Internship Report On Askari Commercial Bank LimitedДокумент43 страницыMalik Asad Pervez's Internship Report On Askari Commercial Bank LimitedMalik Asad Pervez100% (1)

- Internship Report On Bank of PunjabДокумент80 страницInternship Report On Bank of Punjabbbaahmad89100% (1)

- Audit ReportДокумент30 страницAudit ReportAsad Khan100% (3)

- Jeska Final Report PSSFДокумент22 страницыJeska Final Report PSSFMalima BM100% (1)

- Ayesha - Body FileДокумент60 страницAyesha - Body FileMd Khaled NoorОценок пока нет

- Sources and Utilization of Funds of OSCBДокумент12 страницSources and Utilization of Funds of OSCBpapa1988Оценок пока нет

- IFIC BankДокумент18 страницIFIC BankNazmus Sakib100% (1)

- Financial Grants Management Manual Version 1 0 54855hДокумент103 страницыFinancial Grants Management Manual Version 1 0 54855hNano SamyurashviliОценок пока нет

- Internship ReportДокумент79 страницInternship ReportAfroza KhanomОценок пока нет

- Internship Report On National Bank of Pakistan: Zeenat Ullah (BBA Finance)Документ61 страницаInternship Report On National Bank of Pakistan: Zeenat Ullah (BBA Finance)Atta Ur RehmanОценок пока нет

- NBP Project 1Документ54 страницыNBP Project 1Common ManОценок пока нет

- A Project Report ON "Customer Preference and Satisfaction Level For Credit Schemes Offered by The Varachha Co-Operative Bank"Документ109 страницA Project Report ON "Customer Preference and Satisfaction Level For Credit Schemes Offered by The Varachha Co-Operative Bank"Ankit Malani100% (1)

- Public Financial Management Systems—Fiji: Key Elements from a Financial Management PerspectiveОт EverandPublic Financial Management Systems—Fiji: Key Elements from a Financial Management PerspectiveОценок пока нет

- Critical Financial Review: Understanding Corporate Financial InformationОт EverandCritical Financial Review: Understanding Corporate Financial InformationОценок пока нет

- The Budget-Building Book for Nonprofits: A Step-by-Step Guide for Managers and BoardsОт EverandThe Budget-Building Book for Nonprofits: A Step-by-Step Guide for Managers and BoardsОценок пока нет

- Fiscal Decentralization Reform in Cambodia: Progress over the Past Decade and OpportunitiesОт EverandFiscal Decentralization Reform in Cambodia: Progress over the Past Decade and OpportunitiesОценок пока нет

- Strengthening Partnerships: Accountability Mechanism Annual Report 2014От EverandStrengthening Partnerships: Accountability Mechanism Annual Report 2014Оценок пока нет

- Book 2: Futuristic Rugby League: Academy of Excellence for Coaching Rugby Skills and Fitness DrillsОт EverandBook 2: Futuristic Rugby League: Academy of Excellence for Coaching Rugby Skills and Fitness DrillsОценок пока нет

- Term Paper TopicДокумент1 страницаTerm Paper TopicHabibullah SarkerОценок пока нет

- Robbins Ob16 PPT 14Документ29 страницRobbins Ob16 PPT 14Habibullah SarkerОценок пока нет

- Financial Markets: An Engine For Economic GrowthДокумент3 страницыFinancial Markets: An Engine For Economic GrowthHabibullah SarkerОценок пока нет

- Operations Management Lecture 5 Statistical Process ControlДокумент55 страницOperations Management Lecture 5 Statistical Process ControlHabibullah SarkerОценок пока нет

- Foreign Exchange Market in BangladeshДокумент28 страницForeign Exchange Market in BangladeshYeasir Malik85% (20)

- Iba MathsДокумент1 страницаIba MathsHabibullah SarkerОценок пока нет

- Operations Management Lecture 6 Inventory ManagementДокумент60 страницOperations Management Lecture 6 Inventory ManagementHabibullah SarkerОценок пока нет

- 111 Bangladesh PDFДокумент84 страницы111 Bangladesh PDFHabibullah SarkerОценок пока нет

- Principles of Economics - UpdatedДокумент72 страницыPrinciples of Economics - UpdatedHabibullah Sarker0% (1)

- Present Value TablesДокумент4 страницыPresent Value TablesstcreamОценок пока нет

- 9 - Financial Market Developments and Challenges in Bangladesh PDFДокумент84 страницы9 - Financial Market Developments and Challenges in Bangladesh PDFHabibullah Sarker100% (1)

- Present Value TablesДокумент2 страницыPresent Value TablesFreelansir100% (1)

- Lecture-8-Principles of FinaДокумент16 страницLecture-8-Principles of FinaHabibullah SarkerОценок пока нет

- Course ListДокумент2 страницыCourse ListHabibullah SarkerОценок пока нет

- Bangladesh's Experience - Public Financial Management and ProcurementДокумент15 страницBangladesh's Experience - Public Financial Management and ProcurementHabibullah SarkerОценок пока нет

- Table FV A 01Документ1 страницаTable FV A 01Miguel Vásquez TorresОценок пока нет

- Lecture-4 Topic: The Cost of CapitalДокумент23 страницыLecture-4 Topic: The Cost of CapitalHabibullah SarkerОценок пока нет

- Lecture 6: Valuation of Bonds and SharesДокумент12 страницLecture 6: Valuation of Bonds and SharesHabibullah SarkerОценок пока нет

- Group Project MKT-417 Sec. 1 Instructor: Samy Ahmed: Submitted BY Name IDДокумент29 страницGroup Project MKT-417 Sec. 1 Instructor: Samy Ahmed: Submitted BY Name IDHabibullah SarkerОценок пока нет

- Assignment On WTO and Garment Industry of BDДокумент20 страницAssignment On WTO and Garment Industry of BDShantanu Das100% (4)

- FinanceДокумент19 страницFinanceHabibullah SarkerОценок пока нет

- Bangladesh Financial Systems Stability Assessment - IMFДокумент46 страницBangladesh Financial Systems Stability Assessment - IMFSmart IftyОценок пока нет

- Facts, Concepts and ProblemsДокумент1 страницаFacts, Concepts and ProblemsHabibullah SarkerОценок пока нет

- Schaltegger Burrit Zvezdov Carbon Management AccountingДокумент36 страницSchaltegger Burrit Zvezdov Carbon Management AccountingHabibullah SarkerОценок пока нет

- Noc 6Документ2 страницыNoc 6Md.Rashed UzzamanОценок пока нет

- Trade Finance: GuideДокумент36 страницTrade Finance: Guidesujitranair100% (1)

- INTRO - CHAPT2-Economics The Creation and Distribution of WealthДокумент38 страницINTRO - CHAPT2-Economics The Creation and Distribution of WealthHabibullah SarkerОценок пока нет

- May AppДокумент1 страницаMay AppHabibullah SarkerОценок пока нет

- Auditing Problems: Let'S Go!Документ8 страницAuditing Problems: Let'S Go!AiahОценок пока нет

- Equitable PCI Bank V Tan - Santos - 8Документ2 страницыEquitable PCI Bank V Tan - Santos - 8Jasmine Rose Maquiling100% (2)

- NYC Place of Assembly - GuideДокумент21 страницаNYC Place of Assembly - GuideanynomisОценок пока нет

- Guide To Payment Services in SLДокумент86 страницGuide To Payment Services in SLTharuka WijesingheОценок пока нет

- Aakanksha Gurukul Noida Bank StatementДокумент1 страницаAakanksha Gurukul Noida Bank StatementAneeta DeviОценок пока нет

- Congratulations! You Are On One Airtel 1349 PlanДокумент11 страницCongratulations! You Are On One Airtel 1349 Plansandeep salavarОценок пока нет

- SMKSH Alumni Association Draft ConstitutionДокумент9 страницSMKSH Alumni Association Draft Constitutionhizamiiskandar100% (1)

- Sanchayapatra Rules-1977 Up To DateДокумент21 страницаSanchayapatra Rules-1977 Up To Datejoyasree nathОценок пока нет

- 0 0 0 0 94791 SGST (0006)Документ2 страницы0 0 0 0 94791 SGST (0006)dhavalОценок пока нет

- Set IДокумент2 страницыSet IAdoree RamosОценок пока нет

- Iced Cake CollectionДокумент20 страницIced Cake CollectionSlim Kanoun100% (1)

- La Consolacion College-Manila: School of Business and AccountancyДокумент20 страницLa Consolacion College-Manila: School of Business and AccountancyKasey PastorОценок пока нет

- G.R. No. 74917 - Banco de Oro v. Equitable Banking CorpДокумент13 страницG.R. No. 74917 - Banco de Oro v. Equitable Banking CorpAj SobrevegaОценок пока нет

- Internship Report Sindh BankДокумент34 страницыInternship Report Sindh BankAl RafioОценок пока нет

- SAP FICO Certification Test 6Документ18 страницSAP FICO Certification Test 6arfaaОценок пока нет

- Financial Accounting: Sixth EditionДокумент40 страницFinancial Accounting: Sixth EditionA BCОценок пока нет

- PFMS Generated Print Payment Advice: To, The Branch HeadДокумент2 страницыPFMS Generated Print Payment Advice: To, The Branch HeadRAKESH KUMAR CHOUDHARYОценок пока нет

- MYOB Cash Exercise PDFДокумент9 страницMYOB Cash Exercise PDFReese StylesОценок пока нет

- Landbank AccountsДокумент17 страницLandbank AccountscammiecazzieОценок пока нет

- In The Metropolitan Magistrate - Court at Andheri, Mumbai C.C.No. of 2019Документ3 страницыIn The Metropolitan Magistrate - Court at Andheri, Mumbai C.C.No. of 2019VivekОценок пока нет

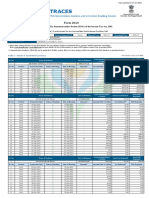

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Документ5 страницForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961kalki17Оценок пока нет

- Philadelphia District Attorney's State Forfeiture Account - RedactedДокумент119 страницPhiladelphia District Attorney's State Forfeiture Account - Redactedmax_marin_paОценок пока нет

- DPB 3023 - Negotiable InstrumentsДокумент28 страницDPB 3023 - Negotiable InstrumentsNur Afiza0% (1)

- Bank Statement KotakДокумент4 страницыBank Statement KotakRamPrasadОценок пока нет