Вам также может понравиться

- 11 Its A Magical World - Bill WattersonДокумент166 страниц11 Its A Magical World - Bill Wattersonapi-560386898100% (8)

- Practical Problems On PV RatioДокумент7 страницPractical Problems On PV Ratiohrmohan8667% (3)

- Not For Profit Organisation: Basic ConceptsДокумент48 страницNot For Profit Organisation: Basic Conceptsmonudeep aggarwalОценок пока нет

- Activity Base Costing (ABC Costing)Документ12 страницActivity Base Costing (ABC Costing)SantОценок пока нет

- Paper - 2: Strategic Financial Management Questions Security ValuationДокумент21 страницаPaper - 2: Strategic Financial Management Questions Security ValuationRITZ BROWNОценок пока нет

- Biopolitics and The Spectacle in Classic Hollywood CinemaДокумент19 страницBiopolitics and The Spectacle in Classic Hollywood CinemaAnastasiia SoloveiОценок пока нет

- PS2082 VleДокумент82 страницыPS2082 Vlebillymambo0% (1)

- Marginal CostingДокумент10 страницMarginal Costinganon_672065362Оценок пока нет

- Rada Trading 1200#119-07-2019Документ5 страницRada Trading 1200#119-07-2019Ing. Ramon AguileraОценок пока нет

- Financial Management-Capital Budgeting:: Answer The Following QuestionsДокумент2 страницыFinancial Management-Capital Budgeting:: Answer The Following QuestionsMitali JulkaОценок пока нет

- Ca Inter C0 Audit Question Bank NewДокумент14 страницCa Inter C0 Audit Question Bank NewDaanish MittalОценок пока нет

- Conversion of Partnership Firm Into CompanyДокумент8 страницConversion of Partnership Firm Into CompanyAthulya MDОценок пока нет

- Completed Jen and Larry's Mini Case Study Working Papers Fall 2014Документ10 страницCompleted Jen and Larry's Mini Case Study Working Papers Fall 2014ZachLoving100% (1)

- Risk AssessmentДокумент11 страницRisk AssessmentRutha KidaneОценок пока нет

- Supply Chain and Logistics Management: Distribution PoliciesДокумент8 страницSupply Chain and Logistics Management: Distribution PoliciesKailas Sree ChandranОценок пока нет

- The City School: Suspense AccountДокумент10 страницThe City School: Suspense AccountHasan ShoaibОценок пока нет

- Secure - Incometax.gov - BD ViewCertiifcate ViewTaxCertificate TIN INFO NO 3118688Документ1 страницаSecure - Incometax.gov - BD ViewCertiifcate ViewTaxCertificate TIN INFO NO 3118688arman_27727627150% (2)

- Just Design Healthy Prisons and The Architecture of Hope (Y.Jewkes, 2012)Документ20 страницJust Design Healthy Prisons and The Architecture of Hope (Y.Jewkes, 2012)Razi MahriОценок пока нет

- Test Present Simple TenseДокумент2 страницыTest Present Simple TenseSuchadaОценок пока нет

- Ikea ReportДокумент48 страницIkea ReportPulkit Puri100% (3)

- Dec-13 Leasing Vs Borrowing SolutionДокумент1 страницаDec-13 Leasing Vs Borrowing Solutiondon_mahinОценок пока нет

- FM Revision 3rd YearДокумент39 страницFM Revision 3rd YearBharat Satyajit100% (1)

- DAIBB Management ACC-1 PDFДокумент24 страницыDAIBB Management ACC-1 PDFAshik100% (1)

- CA IPCC Costing Nov 14 Guideline Answers PDFДокумент13 страницCA IPCC Costing Nov 14 Guideline Answers PDFmohanraokp2279Оценок пока нет

- Daibb - Management Accounting - Broad Question & AnswerДокумент31 страницаDaibb - Management Accounting - Broad Question & AnswerRumana AfrozОценок пока нет

- SFM May 2015Документ25 страницSFM May 2015Prasanna SharmaОценок пока нет

- Paper - 5: Advanced Accounting: © The Institute of Chartered Accountants of IndiaДокумент31 страницаPaper - 5: Advanced Accounting: © The Institute of Chartered Accountants of IndiaVarun reddyОценок пока нет

- LEVERAGE Online Problem SheetДокумент6 страницLEVERAGE Online Problem SheetSoumendra RoyОценок пока нет

- CA Ipcc Costing Suggested Answers For Nov 20161Документ12 страницCA Ipcc Costing Suggested Answers For Nov 20161Sai Kumar SandralaОценок пока нет

- From The Following Summary of Cash Account of X LTDДокумент2 страницыFrom The Following Summary of Cash Account of X LTDLysss EpssssОценок пока нет

- CA Inter Cost Important Questions For CA Nov'22Документ93 страницыCA Inter Cost Important Questions For CA Nov'2202 Tapasvee ShahОценок пока нет

- RAROC ExampleДокумент1 страницаRAROC ExampleVenkatsubramanian R IyerОценок пока нет

- Analysis of Variance (ANOVA) One Way and Two WayДокумент24 страницыAnalysis of Variance (ANOVA) One Way and Two WayPanma PatelОценок пока нет

- Valuation of Securities - ASSIGNMENTДокумент63 страницыValuation of Securities - ASSIGNMENTNaga Nagendra0% (2)

- B LawДокумент240 страницB LawShaheer MalikОценок пока нет

- Chapter 4: Redemption of Pref Share & Debentures Topic: Redemption of Debentures. Practice QuestionsДокумент53 страницыChapter 4: Redemption of Pref Share & Debentures Topic: Redemption of Debentures. Practice QuestionsMercy GamingОценок пока нет

- Chapter 21Документ4 страницыChapter 21Rahila RafiqОценок пока нет

- As 16Документ11 страницAs 16Harsh PatelОценок пока нет

- Ar T.C Om: EadingДокумент8 страницAr T.C Om: Eadingarun1974Оценок пока нет

- Chapter 02 Ratio AnalysisДокумент52 страницыChapter 02 Ratio AnalysisSunita YadavОценок пока нет

- FAQs On CA Zambia CertificationДокумент3 страницыFAQs On CA Zambia CertificationHUMPHREY KAYUNYIОценок пока нет

- Purchase ConsiderationДокумент5 страницPurchase ConsiderationAR Ananth Rohith BhatОценок пока нет

- Financial Management Mba Question PaperДокумент4 страницыFinancial Management Mba Question Paperpalak2407Оценок пока нет

- Unit 3: Cost of Capital Cost of DebtДокумент11 страницUnit 3: Cost of Capital Cost of DebtTaransh A100% (1)

- Fa IiiДокумент76 страницFa Iiirishav agarwalОценок пока нет

- CS Executive MCQ and Risk AnalysisДокумент17 страницCS Executive MCQ and Risk Analysis19101977Оценок пока нет

- Management & Organization (Jamuna Group)Документ14 страницManagement & Organization (Jamuna Group)elenaОценок пока нет

- EbitДокумент3 страницыEbitJann KerkyОценок пока нет

- Techniques of Capital Budgeting SumsДокумент15 страницTechniques of Capital Budgeting Sumshardika jadavОценок пока нет

- Chapter # 6 Departmental AccountДокумент36 страницChapter # 6 Departmental AccountRooh Ullah KhanОценок пока нет

- 7 Finalnew Sugg June09Документ17 страниц7 Finalnew Sugg June09mknatoo1963Оценок пока нет

- Key Factors: Q-1 Key-Factor Product Mix Decision - Minimum Production Condition - Additional CostДокумент11 страницKey Factors: Q-1 Key-Factor Product Mix Decision - Minimum Production Condition - Additional CostPRABESH GAJURELОценок пока нет

- Suggested Answer Paper CAP III Dec 2019Документ142 страницыSuggested Answer Paper CAP III Dec 2019Roshan PanditОценок пока нет

- Problem 5: XY LTDДокумент4 страницыProblem 5: XY LTDAF 1 Tejasri PamujulaОценок пока нет

- 46793bosinter p8 Seca cp5 PDFДокумент42 страницы46793bosinter p8 Seca cp5 PDFIsavic AlsinaОценок пока нет

- Accounting 1 FinalДокумент2 страницыAccounting 1 FinalchiknaaaОценок пока нет

- Class Questions SolutionsДокумент15 страницClass Questions Solutionsmoneshivangi29Оценок пока нет

- Consignment and Joint Venture - Accounting AspectsДокумент49 страницConsignment and Joint Venture - Accounting AspectsKNOWLEDGE CREATORS0% (2)

- Jaibb Accounting Solution Final Acc and Journal EntriesДокумент17 страницJaibb Accounting Solution Final Acc and Journal EntriesAriful Haque Sajib0% (1)

- CS Exec - Prog - Paper-2 Company AC Cost & Management AccountingДокумент25 страницCS Exec - Prog - Paper-2 Company AC Cost & Management AccountingGautam SinghОценок пока нет

- CPA 1 Financial Accounting-1Документ8 страницCPA 1 Financial Accounting-1LYNETTE NYAKAISIKIОценок пока нет

- P2 November 2014 Question Paper PDFДокумент20 страницP2 November 2014 Question Paper PDFAnu MauryaОценок пока нет

- 3 Pre - PostДокумент7 страниц3 Pre - PostParul Bhardwaj VaidyaОценок пока нет

- Corporate Finance Ppt. SlideДокумент24 страницыCorporate Finance Ppt. SlideMd. Jahangir Alam100% (1)

- FINANCIAL MANAGEMENT Assignment 2Документ14 страницFINANCIAL MANAGEMENT Assignment 2dangerous saifОценок пока нет

- DAIBB MA Math Solutions 290315Документ11 страницDAIBB MA Math Solutions 290315joyОценок пока нет

- CVP AnalysisДокумент41 страницаCVP AnalysisMasud Khan ShakilОценок пока нет

- Cost II AssignmentДокумент18 страницCost II AssignmentAddisОценок пока нет

- Final Exam Review2aStudentДокумент9 страницFinal Exam Review2aStudentFatima SОценок пока нет

- FMA Assg 1Документ8 страницFMA Assg 1Dagmawit NegussieОценок пока нет

- ACCT 3210 Hw2Документ3 страницыACCT 3210 Hw2Sin Tung KoОценок пока нет

- Jamuna Bank Limited: Report Name: Income Expenditure Comparison ReportДокумент35 страницJamuna Bank Limited: Report Name: Income Expenditure Comparison Reportarman_277276271Оценок пока нет

- Jamuna Bank Limited: Report Name: Statement of Affairs ConsolidatedДокумент5 страницJamuna Bank Limited: Report Name: Statement of Affairs Consolidatedarman_277276271Оценок пока нет

- Absorption CostingДокумент23 страницыAbsorption Costingarman_277276271Оценок пока нет

- Stamp Duty On Insterument-08.09.2019Документ2 страницыStamp Duty On Insterument-08.09.2019arman_277276271Оценок пока нет

- 3.0 Product MixДокумент8 страниц3.0 Product Mixarman_277276271Оценок пока нет

- PassДокумент1 страницаPassarman_277276271Оценок пока нет

- Return & Risk: Welcome To The Lecture Session OnДокумент13 страницReturn & Risk: Welcome To The Lecture Session Onarman_277276271Оценок пока нет

- Wbffiwb DW: Membershi FromДокумент1 страницаWbffiwb DW: Membershi Fromarman_277276271Оценок пока нет

- Law &prac.Документ16 страницLaw &prac.arman_277276271Оценок пока нет

- Summary of Loan ClassificationДокумент27 страницSummary of Loan Classificationarman_277276271Оценок пока нет

- TIN CertificateДокумент1 страницаTIN Certificatearman_277276271Оценок пока нет

- AshugonjДокумент1 страницаAshugonjarman_277276271Оценок пока нет

- Financial Highlight 2016Документ1 страницаFinancial Highlight 2016arman_277276271Оценок пока нет

- Fund Transfer PDFДокумент1 страницаFund Transfer PDFarman_277276271Оценок пока нет

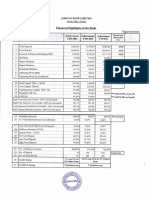

- Financial HighlightsДокумент1 страницаFinancial Highlightsarman_277276271Оценок пока нет

- Harun VaiДокумент1 страницаHarun Vaiarman_277276271Оценок пока нет

- Notification: Professional Examination Result: November-December 2020Документ2 страницыNotification: Professional Examination Result: November-December 2020Zahidul Amin FarhadОценок пока нет

- Berkshire Hathaway Inc.: United States Securities and Exchange CommissionДокумент48 страницBerkshire Hathaway Inc.: United States Securities and Exchange CommissionTu Zhan LuoОценок пока нет

- A2 UNIT 2 Extra Grammar Practice RevisionДокумент1 страницаA2 UNIT 2 Extra Grammar Practice RevisionCarolinaОценок пока нет

- Q2 Emptech W1 4Документ32 страницыQ2 Emptech W1 4Adeleine YapОценок пока нет

- Sir Gawain and The Green Knight: A TranslationДокумент39 страницSir Gawain and The Green Knight: A TranslationJohn AshtonОценок пока нет

- Kishore M. Daswani - ResumeДокумент3 страницыKishore M. Daswani - ResumeKishore DaswaniОценок пока нет

- Individual Paper Proposal For Biochar Literature ReviewДокумент2 страницыIndividual Paper Proposal For Biochar Literature ReviewraiiinydaysОценок пока нет

- Conduct Disorder ChecklistДокумент1 страницаConduct Disorder Checklistiswarya vellaisamyОценок пока нет

- ARTA Art of Emerging Europe2Документ2 страницыARTA Art of Emerging Europe2DanSanity TVОценок пока нет

- OD2e L4 Reading Comprehension WS Unit 3Документ2 страницыOD2e L4 Reading Comprehension WS Unit 3Nadeen NabilОценок пока нет

- 7 Principles or 7 CДокумент5 страниц7 Principles or 7 Cnimra mehboobОценок пока нет

- EDUC - 115 D - Fall2018 - Kathryn GauthierДокумент7 страницEDUC - 115 D - Fall2018 - Kathryn Gauthierdocs4me_nowОценок пока нет

- Suggested Answer: Business Strategy May-June 2018Документ10 страницSuggested Answer: Business Strategy May-June 2018Towhidul IslamОценок пока нет

- 2010 Final Graduation ScriptДокумент8 страниц2010 Final Graduation ScriptUmmu Assihdi100% (1)

- Albert EinsteinДокумент3 страницыAlbert EinsteinAgus GLОценок пока нет

- Final Project Report - Keiretsu: Topic Page NoДокумент10 страницFinal Project Report - Keiretsu: Topic Page NoRevatiОценок пока нет

- Nurlilis (Tgs. Bhs - Inggris. Chapter 4)Документ5 страницNurlilis (Tgs. Bhs - Inggris. Chapter 4)Latifa Hanafi100% (1)

- Mercado v. Nambi FLORESДокумент2 страницыMercado v. Nambi FLORESCarlos JamesОценок пока нет

- P.S. Deodhar - Cinasthana Today - Viewing China From India-Tata McGraw Hill Education (2014)Документ372 страницыP.S. Deodhar - Cinasthana Today - Viewing China From India-Tata McGraw Hill Education (2014)MANEESH JADHAVОценок пока нет

- Pankaj YadavSEPT - 2022Документ1 страницаPankaj YadavSEPT - 2022dhirajutekar990Оценок пока нет