Вам также может понравиться

- 10 Rules of CommerceДокумент2 страницы10 Rules of Commercesabiont92% (24)

- Mrs Janada Solomon 500 Laurel Lane, Midland, Texas 79701Документ2 страницыMrs Janada Solomon 500 Laurel Lane, Midland, Texas 79701SolomonОценок пока нет

- Export Credit Agencies - The Unsung Giants of International Trade and FinanceДокумент207 страницExport Credit Agencies - The Unsung Giants of International Trade and Financeace187Оценок пока нет

- Thesis SocialmediaДокумент33 страницыThesis Socialmediagkzuniga44% (9)

- Maritme 1-5Документ28 страницMaritme 1-5gkzuniga100% (1)

- The Successful Strategies from Customer Managment ExcellenceОт EverandThe Successful Strategies from Customer Managment ExcellenceОценок пока нет

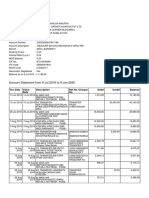

- Account Statement From 9 Jul 2019 To 9 Jan 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент4 страницыAccount Statement From 9 Jul 2019 To 9 Jan 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancemauryapiaeОценок пока нет

- RCBC VS BdoДокумент3 страницыRCBC VS BdoPao InfanteОценок пока нет

- Project On Axis BankДокумент36 страницProject On Axis Bankratandeepjain86% (7)

- Chapter 1 - 2Документ31 страницаChapter 1 - 2gkzuniga13% (8)

- Customer Satisfaction in Banking Sector Research ProposalДокумент9 страницCustomer Satisfaction in Banking Sector Research Proposalmasoom_soorat100% (3)

- The Problem and Its BackgroundДокумент46 страницThe Problem and Its BackgroundgkzunigaОценок пока нет

- The Problem and Its BackgroundДокумент46 страницThe Problem and Its BackgroundgkzunigaОценок пока нет

- Thesis BullyingДокумент35 страницThesis Bullyinggkzuniga74% (19)

- 4t3marikina The Sole of ManilaДокумент15 страниц4t3marikina The Sole of ManilagkzunigaОценок пока нет

- Expo Exhi 2008Документ72 страницыExpo Exhi 2008Engr Umar Iqbal100% (1)

- Dork Carding 2017Документ6 страницDork Carding 2017owen011111Оценок пока нет

- Trade FinanceДокумент65 страницTrade Financeanon_879138113100% (1)

- Measuring Customer Satisfaction: Exploring Customer Satisfaction’s Relationship with Purchase BehaviorОт EverandMeasuring Customer Satisfaction: Exploring Customer Satisfaction’s Relationship with Purchase BehaviorРейтинг: 4.5 из 5 звезд4.5/5 (6)

- Organizational Customers' Retention Strategies On CustomerДокумент10 страницOrganizational Customers' Retention Strategies On CustomerDon CM WanzalaОценок пока нет

- Obsinan Dejene Business Research ProposalДокумент26 страницObsinan Dejene Business Research Proposalobsinan dejene100% (2)

- Coca Cola Brand CateryДокумент15 страницCoca Cola Brand Cateryamith chathurangaОценок пока нет

- Chapter 1Документ6 страницChapter 1Fakir TajulОценок пока нет

- Client Service Quality of The Board of InvestmentsДокумент12 страницClient Service Quality of The Board of InvestmentsIza EstinopoОценок пока нет

- 007 - Review of LiteratureДокумент15 страниц007 - Review of LiteratureNamrata SaxenaОценок пока нет

- Research ProposalДокумент29 страницResearch ProposalNitesh KhatiwadaОценок пока нет

- Research Proposal - BU7756Документ16 страницResearch Proposal - BU7756Yugandhar KumarОценок пока нет

- SSRN Id2493709Документ82 страницыSSRN Id2493709Mohamed MukhtarОценок пока нет

- Customer Satisfaction in Banking Sector: A Case Study On Janata Bank LimitedДокумент11 страницCustomer Satisfaction in Banking Sector: A Case Study On Janata Bank LimitedJannatul FerdousОценок пока нет

- PROJECTДокумент44 страницыPROJECTaagambarawaОценок пока нет

- Synopsis Disst.Документ28 страницSynopsis Disst.Brijesh GandhiОценок пока нет

- ProjectДокумент85 страницProjectPansy ShardaОценок пока нет

- Project Proposal MDP2 FinalДокумент8 страницProject Proposal MDP2 FinaltawandaОценок пока нет

- Determinants of Customer Satisfaction of Banking Industry in BangladeshДокумент15 страницDeterminants of Customer Satisfaction of Banking Industry in BangladeshFauzi DjibranОценок пока нет

- The Effect of Conscientious On Customer SatisfactionДокумент22 страницыThe Effect of Conscientious On Customer SatisfactionHaryour Bar MieyОценок пока нет

- Marketing Term Paper On HorlicksДокумент16 страницMarketing Term Paper On HorlicksArijit Podder PulakОценок пока нет

- Kahsay Edited 2 ProposalДокумент29 страницKahsay Edited 2 Proposalkahissay berihunОценок пока нет

- Final Thesis File Uplode by View GlobalДокумент67 страницFinal Thesis File Uplode by View GlobalBishnu Prasad Bhattarai - BhimОценок пока нет

- A Comperative Study of Customer Perception in Icici Bank and HDFC BankДокумент11 страницA Comperative Study of Customer Perception in Icici Bank and HDFC BankSourabh Mishra100% (1)

- Chapter 2Документ22 страницыChapter 2Okorie Chinedu PОценок пока нет

- Service Marketing 2018 & 2019Документ4 страницыService Marketing 2018 & 2019Satyam singhОценок пока нет

- Customer Service Department and Clients Satisfaction: An Empirical Study of Commercial Bank of Surkhet, ValleyДокумент7 страницCustomer Service Department and Clients Satisfaction: An Empirical Study of Commercial Bank of Surkhet, ValleyThe IjbmtОценок пока нет

- F016214451 PDFДокумент8 страницF016214451 PDFramyaОценок пока нет

- Introduction and Design of The Study: Chapter - 1Документ33 страницыIntroduction and Design of The Study: Chapter - 1Rohan SharmaОценок пока нет

- RESEARCH 123 RevisedДокумент13 страницRESEARCH 123 RevisedWilma Sayam BarucОценок пока нет

- New Microsoft Word Document - OdtДокумент5 страницNew Microsoft Word Document - OdtObsetan HurisaОценок пока нет

- Chapter One: 1.1 Background of The StudyДокумент65 страницChapter One: 1.1 Background of The Studysami samiОценок пока нет

- Presentation1 ZenawДокумент21 страницаPresentation1 ZenawTesema GenetuОценок пока нет

- Impact of Customer Relationship Management On Customers LoyaltyДокумент26 страницImpact of Customer Relationship Management On Customers LoyaltyAjewole Eben TopeОценок пока нет

- Customer Service of Banking. DUДокумент19 страницCustomer Service of Banking. DUkaiumОценок пока нет

- Relationship Between Customer Satisfaction and ProfitabilityДокумент51 страницаRelationship Between Customer Satisfaction and ProfitabilityNajie LawiОценок пока нет

- 03-06-2021-1622721579-7-Ijbgm-11. Ijbgm - Service Quality Indexing - Sqi - For Financial InstitutionsДокумент6 страниц03-06-2021-1622721579-7-Ijbgm-11. Ijbgm - Service Quality Indexing - Sqi - For Financial Institutionsiaset123Оценок пока нет

- International Journal of Business and Management Invention (IJBMI)Документ9 страницInternational Journal of Business and Management Invention (IJBMI)inventionjournalsОценок пока нет

- Customer LoyaltyДокумент38 страницCustomer LoyaltyAnand sharmaОценок пока нет

- Related Papers: IOSR JournalsДокумент9 страницRelated Papers: IOSR JournalsMavani snehaОценок пока нет

- TQM Chapter 6Документ5 страницTQM Chapter 6Khel PinedaОценок пока нет

- 10customer SatisfactionДокумент7 страниц10customer SatisfactionReynhard DaleОценок пока нет

- A Study On Impact of Service Quality On Customer Satisfaction in The Indian Insurance IndustryДокумент8 страницA Study On Impact of Service Quality On Customer Satisfaction in The Indian Insurance IndustrySwathy SanthoshОценок пока нет

- SefviceQualityImpactOnCustomerSatisfaction (1 4) 0ef582b6 Ab61 4c2d 9214 4f2dfa2d5757Документ4 страницыSefviceQualityImpactOnCustomerSatisfaction (1 4) 0ef582b6 Ab61 4c2d 9214 4f2dfa2d5757esmani84Оценок пока нет

- Chapter 1-3 With QuestionnaireДокумент29 страницChapter 1-3 With QuestionnaireMichelle Bautista100% (2)

- Paper+1+Information+Sharing+Quality+Assurance+6 OctДокумент18 страницPaper+1+Information+Sharing+Quality+Assurance+6 OctRabia ArooshОценок пока нет

- A Research ProposalДокумент14 страницA Research ProposalMIAN USMANОценок пока нет

- Saurav 123Документ15 страницSaurav 123aslam khanОценок пока нет

- SSRN Id3703405Документ8 страницSSRN Id3703405Kaushik SutradharОценок пока нет

- Delivering Effective Customer Service Final ReportДокумент51 страницаDelivering Effective Customer Service Final ReportAmit SinghОценок пока нет

- Chapter IДокумент81 страницаChapter ILhyn RicafrenteОценок пока нет

- An SariДокумент8 страницAn SariAnkit SinghalОценок пока нет

- Service ManagementДокумент6 страницService ManagementkkОценок пока нет

- SFINAL Literature ReviewДокумент10 страницSFINAL Literature Reviewpurva02Оценок пока нет

- ServloyalДокумент5 страницServloyalNishant JoshiОценок пока нет

- Seevice Recovery (Research Methodology)Документ86 страницSeevice Recovery (Research Methodology)Leroy SaneОценок пока нет

- 184 Sayendra SharmaДокумент6 страниц184 Sayendra Sharmagowtham rajaОценок пока нет

- The Influence of Quality of Complaints Handling Services and Customer Choices On Hotel Customer LoyaltyДокумент6 страницThe Influence of Quality of Complaints Handling Services and Customer Choices On Hotel Customer LoyaltyThe IjbmtОценок пока нет

- Review of Related LiteratureДокумент11 страницReview of Related LiteratureRo BinОценок пока нет

- Marketing of Consumer Financial Products: Insights From Service MarketingОт EverandMarketing of Consumer Financial Products: Insights From Service MarketingОценок пока нет

- The Changing Global Marketplace Landscape: Understanding Customer Intentions, Attitudes, Beliefs, and FeelingsОт EverandThe Changing Global Marketplace Landscape: Understanding Customer Intentions, Attitudes, Beliefs, and FeelingsОценок пока нет

- Chapter 1 BpoДокумент12 страницChapter 1 BpogkzunigaОценок пока нет

- I. Executive SummaryДокумент15 страницI. Executive SummarygkzunigaОценок пока нет

- ResearchДокумент47 страницResearchgkzunigaОценок пока нет

- Thesis ProposalДокумент15 страницThesis ProposalgkzunigaОценок пока нет

- Chapter 1 UpdatedДокумент26 страницChapter 1 Updatedgkzuniga50% (2)

- CHAPTER V - ConclusionДокумент17 страницCHAPTER V - ConclusiongkzunigaОценок пока нет

- De Elderly Retirement Homes InPH Ver2 With CommentsДокумент20 страницDe Elderly Retirement Homes InPH Ver2 With CommentsgkzunigaОценок пока нет

- Conceptpaper BDOДокумент3 страницыConceptpaper BDOgkzunigaОценок пока нет

- Kookie Krumble Bowl Factory: Solo or SharingДокумент2 страницыKookie Krumble Bowl Factory: Solo or SharinggkzunigaОценок пока нет

- Alyannah RevisedДокумент119 страницAlyannah RevisedgkzunigaОценок пока нет

- Tourism Development at Monas Tower, Central Jakarta: Feasibility Study OnДокумент6 страницTourism Development at Monas Tower, Central Jakarta: Feasibility Study OngkzunigaОценок пока нет

- FB Ep CompleteДокумент32 страницыFB Ep CompletegkzunigaОценок пока нет

- Jose Rizal UniversityДокумент24 страницыJose Rizal Universitygkzuniga100% (1)

- Chapter 1 - 5 ThesisДокумент54 страницыChapter 1 - 5 ThesisgkzunigaОценок пока нет

- Proposed Curriculum For Grade 6 S.Y. 2015-2016: Lessons CoverageДокумент10 страницProposed Curriculum For Grade 6 S.Y. 2015-2016: Lessons CoveragegkzunigaОценок пока нет

- The Problem and Its Setting: What Do Children Need To Learn?Документ4 страницыThe Problem and Its Setting: What Do Children Need To Learn?gkzunigaОценок пока нет

- Please See Comment On U1: One in Christ, Love, Serve and Celebrate!Документ2 страницыPlease See Comment On U1: One in Christ, Love, Serve and Celebrate!gkzunigaОценок пока нет

- Formative Assess StrategiesДокумент20 страницFormative Assess StrategiesAnaly BacalucosОценок пока нет

- Islamic Finance What Is It ?Документ15 страницIslamic Finance What Is It ?Arief Cracker CeeОценок пока нет

- Petitioner Vs Vs Respondents: First DivisionДокумент8 страницPetitioner Vs Vs Respondents: First DivisionMichaella Claire LayugОценок пока нет

- Chapter 6 ZicaДокумент45 страницChapter 6 ZicaVainess S Zulu100% (4)

- Partial Withdrawal FormДокумент1 страницаPartial Withdrawal Formmohd uzaini mat jusohОценок пока нет

- P 1 Aug 29Документ1 страницаP 1 Aug 29hlaldinmawiaОценок пока нет

- Portfolio Management and Mutual Fund Analysis PDFДокумент53 страницыPortfolio Management and Mutual Fund Analysis PDFRenuprakash Kp75% (4)

- Tepper v. Temple-InlandДокумент114 страницTepper v. Temple-InlandDealBookОценок пока нет

- SHOCKER: Internal Emails Reveal Florida Legislative Staff Asked Payday Industry For Approval of Changes To New Lending BillДокумент9 страницSHOCKER: Internal Emails Reveal Florida Legislative Staff Asked Payday Industry For Approval of Changes To New Lending BillAllied ProgressОценок пока нет

- Internal Factor Evaluation (Ife) of Kotak Mahindra: Key Success Factors Weight Rate ScoreДокумент9 страницInternal Factor Evaluation (Ife) of Kotak Mahindra: Key Success Factors Weight Rate Scoresimran punjabiОценок пока нет

- Cipla-I 4/4/2018 13:45 565.55 NEUTRAL 567.34 Cnxit-I 4/4/2018 12:30 12620 SELL MODE 12634.93Документ8 страницCipla-I 4/4/2018 13:45 565.55 NEUTRAL 567.34 Cnxit-I 4/4/2018 12:30 12620 SELL MODE 12634.93dewanibipinОценок пока нет

- Bangladesh University of Business & Technology (BUBT)Документ3 страницыBangladesh University of Business & Technology (BUBT)sagarsbhОценок пока нет

- Principales Organismos ReguladoresДокумент5 страницPrincipales Organismos Reguladoresholger azael murillo gomezОценок пока нет

- A Case Study On FINOДокумент9 страницA Case Study On FINOPiyush Singh PrasannaОценок пока нет

- How To Save Money - 8 Simple Ways To Start Saving Money PDFДокумент6 страницHow To Save Money - 8 Simple Ways To Start Saving Money PDFMark AОценок пока нет

- Shipping EconomistДокумент52 страницыShipping EconomistJames RobbinsОценок пока нет

- MFM Project Guidelines From Christ University FFFFFДокумент6 страницMFM Project Guidelines From Christ University FFFFFakash08agarwal_18589Оценок пока нет

- EHS - Bob LittermanДокумент27 страницEHS - Bob LittermanjjkkkkjkОценок пока нет

- Trends and Challenges in Islamic FinanceДокумент20 страницTrends and Challenges in Islamic FinanceManfadawi FadawiОценок пока нет

- GSAA Home Equity Trust 2005-15 - Purchased Property 3 Years After Closing Date From US BankДокумент7 страницGSAA Home Equity Trust 2005-15 - Purchased Property 3 Years After Closing Date From US BankTim BryantОценок пока нет

- RBA APU PPT - OJK 16 April 2018Документ46 страницRBA APU PPT - OJK 16 April 2018BunnyОценок пока нет

- Real Estate Guide - April / May 2012Документ88 страницReal Estate Guide - April / May 2012Echo PressОценок пока нет